Question: Options and mathematics: Do not skip calculations in the exercises and write as clear as possible. If some portion of the solution is not clearly

Options and mathematics:

Do not skip calculations in the exercises and write as clear as possible. If some portion of the solution is not clearly readable, it will be assumed to be wrong.

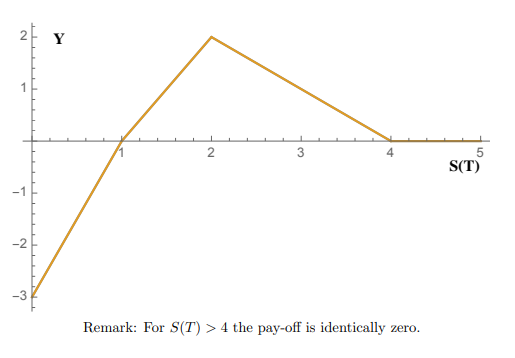

1. Find a constant portfolio consisting of European puts that replicates the European derivative with maturity T and pay-off Y depicted down here:

25 Y 2 3 3 5 S(T) - 1 -2 -3 Remark: For S(T) > 4 the pay-off is identically zero

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock