Over a two-day period, beginning February 15, 2020, XYZ Oil Corporation would sign a contract for the

Question:

Over a two-day period, beginning February 15, 2020, XYZ Oil Corporation would sign a contract for the purchase of a ship. At that time, the company had to commit to making a single payment or to spread the payment over approximately 34 months. A complicating factor was that the payment(s) would be in yen. The purchase decision had been made only that morning, and Mark Floyd, who only three weeks previously had transferred to corporate headquarters from a regional office, had been asked to make the recommendation on means of payment.

XYZ operated through separate divisions devoted to exploring and producing chemicals, marketing, refining and transporting and shipping. The company had recently decided that the Mediterranean would be increasingly important source of crude oil. Domestic production in The United States was falling, and demand for low-sulfur fuels, of which the Mediterranean was one of the prime suppliers, were increasing. XYZ had thus made a commitment to purchase several very large crude carriers (VLCC) over the next five years. The construction of the first for a total cost of 15 billion yen had recently been negotiated with a large Japanese shipyard. At the actual contract signing on February 15, XYZ could choose a single payment covering the full cost of the vessel or the 4x4-payment plan usually associated with projects of this type.

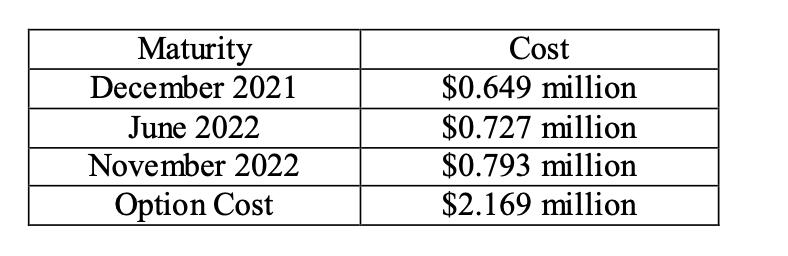

Under a 4x4 payment plan, XYZ would pay 25 percent of the purchase price at the time of the signing. The next payment of 25 percent would be due at the time of the keel laying, which was expected to take place by the end of December 2021. An additional 25 percent would be payable when the ship was launched in June of 2022, and the final 25 percent would be due at delivery. The final delivery date specified in the contract was the end of November 2022.

The alternative offered by the Japanese firm was a single payment of 13.17 billion yen to be paid on February 15.

A major complication in the decision was that the payment(s) would have to be in Japanese yen. If XYZ decided to take the single-payment alternative, no exchange rate problem existed since the company could exchange the 13.17 billion yen at 110.07 yen to the U.S. dollar, the rate on February 13, 2020, which would fix the cost at $119.65 million. If on the other hand, 4x4 plan was chosen, the exchange rates for the various due dates were uncertain. Yet, XYZ Oil's forecast of exchange rates were for the yen to be in the 100-120 range by the end of 2021, the 95-115 range by the middle of 2022, and the 90-110 range by the end of 2022.

XYZ had recently been using a hurdle rate of 10 percent for evaluating projects in excess of $10 million, and taxes played no role in the decision because of special tax credits.

The exchange rate risk inherent in the 4x4 plan could be hedged in various ways. One way was a forward contract. After calling several banks XYZ estimated that he could get forward rates of 107.5 yen to the US dollar for the end of 2021, 105.5 yen to the U.S. dollar for the middle of 2022 and 104 yen to the dollar for the end of 2022.

An alternative for dealing with the exchange rate risk was to use yen call options. A dealer had offered the following yen call options with exercise prices of 110.07 yen to the US dollar:

XYZ has three alternatives to decide: do nothing, use forward and use the call option. What choice should he make?

Expert Answer:

If the company makes a single payment the cost in dollars 11965 million Alternative 1 Doing nothing ... View the full answer

Dynamic Business Law The Essentials

ISBN: 978-0073524979

2nd edition

Authors: Nancy Kubasek, Neil Browne, Daniel Herron