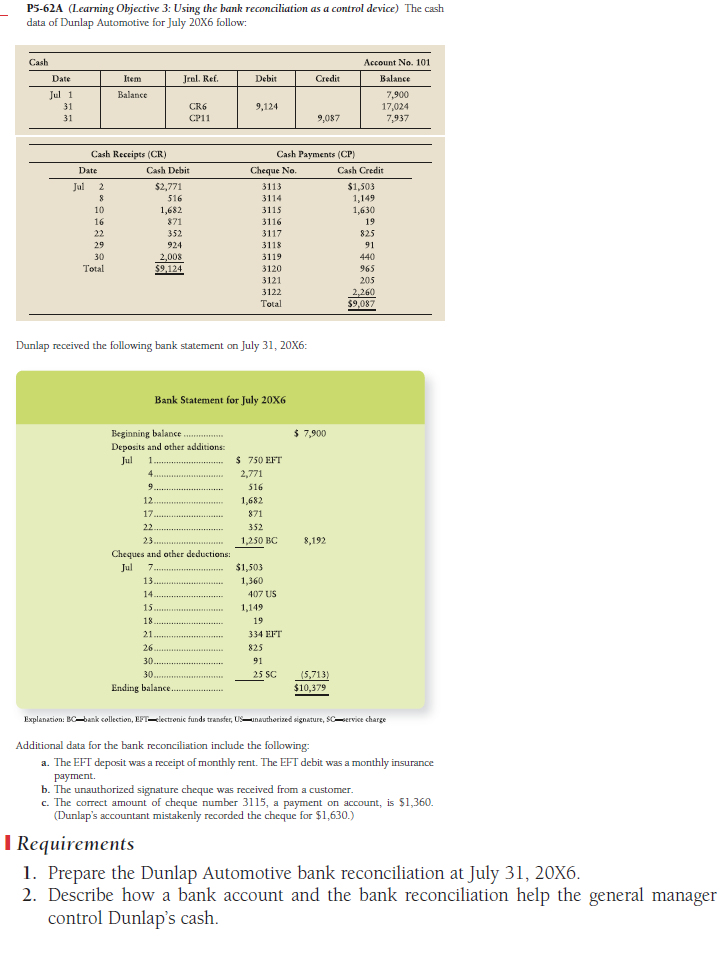

Question: P5-62A (Learning Objective 3: Using the bank reconciliation as a control device) The cash data of Dunlap Automotive for July 20X6 follow: Cash Account No.

P5-62A (Learning Objective 3: Using the bank reconciliation as a control device) The cash data of Dunlap Automotive for July 20X6 follow: Cash Account No. 101 Jral. Ref. Debit Jul 1 31 31 7,900 17,024 7,937 9,124 CR6 CP11 9,087 Cash Receipts (CR) Cash Payments (CP) Cheque No. 3113 3114 3115 116 3117 3118 3119 3120 3121 3122 Total Cash Debit Cash Credit $1,503 1,149 1,630 19 825 Jul 2 $2,771 516 1,682 871 352 924 008 10 16 Total 965 $9,087 Dunlap received the following bank statement on July 31, 20X6 Bank Statement for July 20X6 Beginning balance Deposits and other additions: $ 7,900 $ 750 EFT 2,771 516 1,682 871 352 12 17 3 1,250 BC 8,192 Cheques and other deductions: $1,503 1,360 13 407 US 5s 1,149 19 21 26 30 334 EFT 825 91 25 SC15,713 $10,379 Ending balanc Additional data for the bank reconciliation include the following a. The EFT depasit was a receipt of monthly rent. The EFT debit was a monthly insurance b. The unauthorized signature chequ c. The cormect amount of cheque number 3115, a payment on account, is $1,360. e was received from a customer Dunlap's accountant mistakenly recorded the cheque for $1,630.) l Requirements 1. Prepare the Dunlap Automotive bank reconciliation at July 31, 20X6 2. Describe how a bank account and the bank reconciliation help the general manager control Dunlap's cash

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts