The following situations relate to different companies that are required to implement relevant IFRSS to deal...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

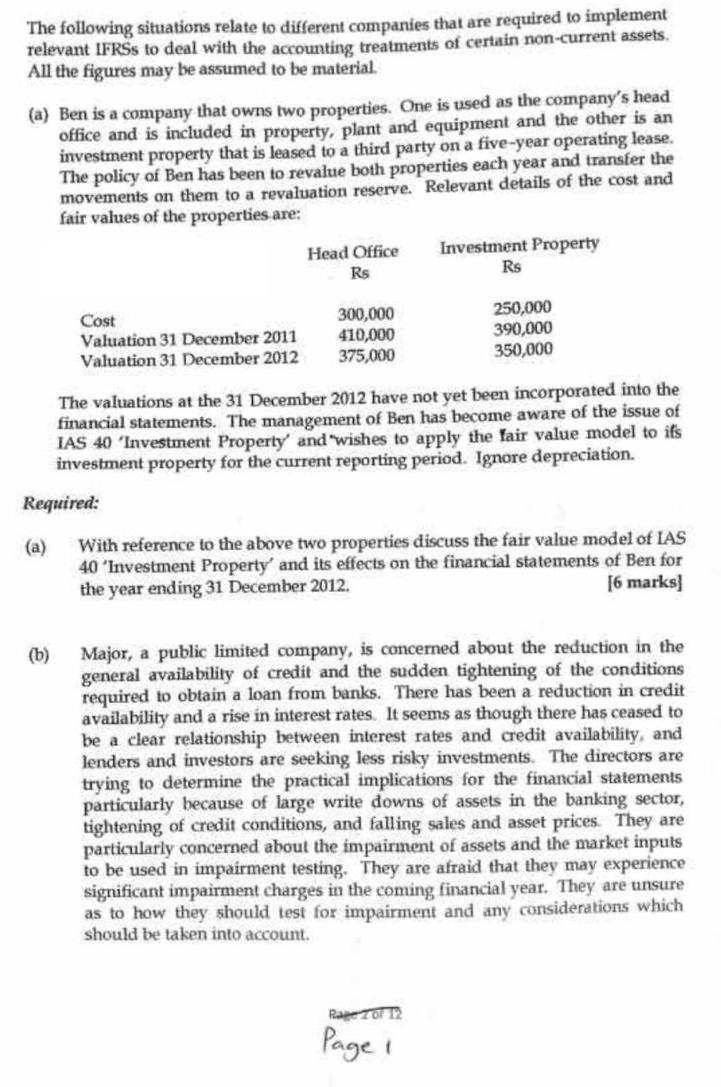

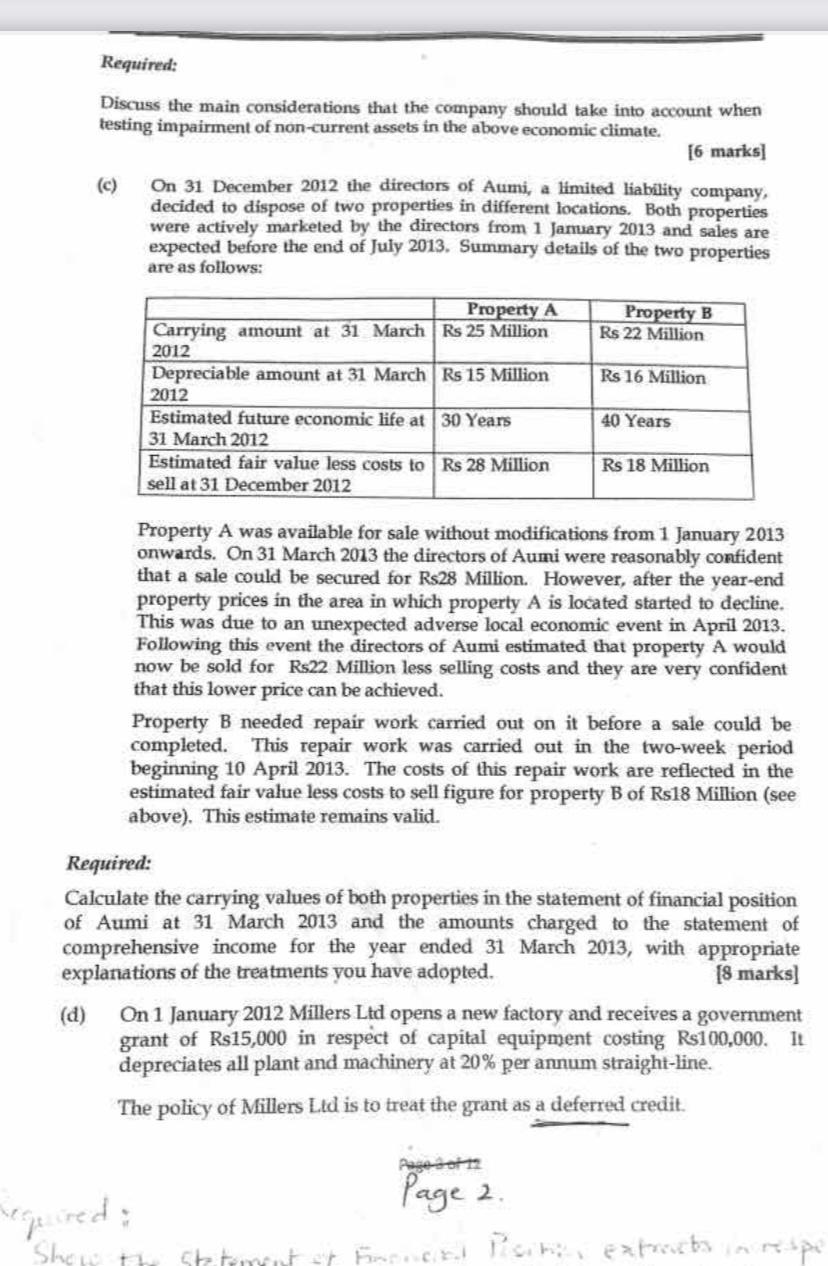

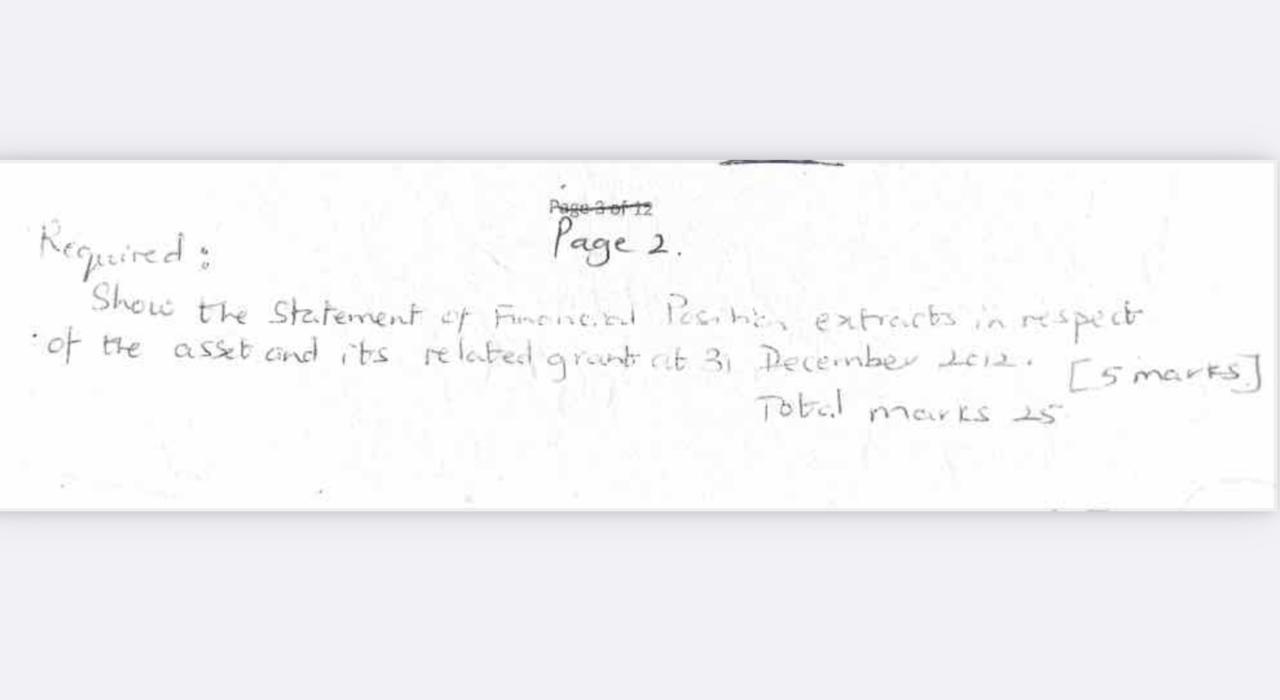

The following situations relate to different companies that are required to implement relevant IFRSS to deal with the accounting treatments of certain non-current assets. All the figures may be assumed to be material. (a) Ben is a company that owns two properties. One is used as the company's head office and is included in property, plant and equipment and the other is an investment property that is leased to a third party on a five-year operating lease. The policy of Ben has been to revalue both properties each year and transfer the movements on them to a revaluation reserve. Relevant details of the cost and fair values of the properties are: Investment Property Rs Head Office Rs Cost Valuation 31 December 2011 Valuation 31 December 2012 300,000 410,000 375,000 250,000 390,000 350,000 The valuations at the 31 December 2012 have not yet been incorporated into the financial statements. The mnanagement of Ben has become aware of the issue of IAS 40 'Investment Property' and wishes to apply the fair value model to ifs investment property for the current reporting period. Ignore depreciation. Required: (a) With reference to the above two properties discuss the fair value model of IAS 40 'Investment Property' and its effects on the financial statements of Ben for the year ending 31 December 2012. [6 marks] Major, a public limited company, is concerned about the reduction in the (b) general availability of credit and the sudden tightening of the conditions required to obtain a loan from banks. There has been a reduction in credit availability and a rise in interest rates. It seems as though there has ceased to be a clear relationship between interest rates and credit availability, and lenders and investors are seeking less risky investments. The directors are trying to determine the practical implications for the financial statements particularly because of large write downs of assets in the banking sector, tightening of credit conditions, and falling sales and asset prices. They are particularly concerned about the impairment of assets and the market inputs to be used in impairment testing. They are afraid that they may experience significant impairment charges in the coming financial year. They are unsure as to how they should test for impairment and any considerations which should be taken into account. RageTo 12 Page i Required: Discuss the main considerations that the company should take into account when testing impairment of non-current assets in the above economic climate. [6 marks] On 31 December 2012 the directors of Aumi, a limited liability company, (c) decided to dispose of two properties in different locations. Both properties were actively marketed by the directors from 1 Jamuary 2013 and sales are expected before the end of July 2013. Summary details of the two properties are as follows: Property A Property B Rs 22 Million Carrying amount at 31 March Rs 25 Million 2012 Depreciable amount at 31 March Rs 15 Million 2012 Estimated future economic life at 30 Years 31 March 2012 Estimated fair value less costs to Rs 28 Million sell at 31 December 2012 Rs 16 Million 40 Years Rs 18 Million Property A was available for sale without modifications from 1 January 2013 onwards. On 31 March 2013 the directors of Aumi were reasonably confident that a sale could be secured for Rs28 Milion. However, after the year-end property prices in the area in which property A is located started to decline. This was due to an unexpected adverse local economic event in April 2013. Following this event the directors of Aumi estimated that property A would now be sold for Rs22 Million less selling costs and they are very confident that this lower price can be achieved. Property B needed repair work carried out on it before a sale could be completed. This repair work was carried out in the two-week period beginning 10 April 2013. The costs of this repair work are reflected in the estimated fair value less costs to sell figure for property B of Rs18 Million (see above). This estimate remains valid. Required: Calculate the carrying values of both properties in the statement of financial position of Aumi at 31 March 2013 and the amounts charged to the statement of comprehensive income for the year ended 31 March 2013, with appropriate explanations of the treatments you have adopted. [8 marks] On 1 January 2012 Millers Ltd opens a new factory and receives a government (d) grant of Rs15,000 in respect of capital equipment costing Rs100,000. It depreciates all plant and machinery at 20 % per annum straight-line. The policy of Millers Ltd is to treat the grant as a deferred credit. Page 2. Shew th Statuyut st Ancc ici exteba Page 3 of 12 Page 2. Required; Show the Steterment cf Fimene.bud Pesiti, extraurts in respect of the asset cind its related grant at 31 December Le12. [s marks] Tobal marks 25 The following situations relate to different companies that are required to implement relevant IFRSS to deal with the accounting treatments of certain non-current assets. All the figures may be assumed to be material. (a) Ben is a company that owns two properties. One is used as the company's head office and is included in property, plant and equipment and the other is an investment property that is leased to a third party on a five-year operating lease. The policy of Ben has been to revalue both properties each year and transfer the movements on them to a revaluation reserve. Relevant details of the cost and fair values of the properties are: Investment Property Rs Head Office Rs Cost Valuation 31 December 2011 Valuation 31 December 2012 300,000 410,000 375,000 250,000 390,000 350,000 The valuations at the 31 December 2012 have not yet been incorporated into the financial statements. The mnanagement of Ben has become aware of the issue of IAS 40 'Investment Property' and wishes to apply the fair value model to ifs investment property for the current reporting period. Ignore depreciation. Required: (a) With reference to the above two properties discuss the fair value model of IAS 40 'Investment Property' and its effects on the financial statements of Ben for the year ending 31 December 2012. [6 marks] Major, a public limited company, is concerned about the reduction in the (b) general availability of credit and the sudden tightening of the conditions required to obtain a loan from banks. There has been a reduction in credit availability and a rise in interest rates. It seems as though there has ceased to be a clear relationship between interest rates and credit availability, and lenders and investors are seeking less risky investments. The directors are trying to determine the practical implications for the financial statements particularly because of large write downs of assets in the banking sector, tightening of credit conditions, and falling sales and asset prices. They are particularly concerned about the impairment of assets and the market inputs to be used in impairment testing. They are afraid that they may experience significant impairment charges in the coming financial year. They are unsure as to how they should test for impairment and any considerations which should be taken into account. RageTo 12 Page i Required: Discuss the main considerations that the company should take into account when testing impairment of non-current assets in the above economic climate. [6 marks] On 31 December 2012 the directors of Aumi, a limited liability company, (c) decided to dispose of two properties in different locations. Both properties were actively marketed by the directors from 1 Jamuary 2013 and sales are expected before the end of July 2013. Summary details of the two properties are as follows: Property A Property B Rs 22 Million Carrying amount at 31 March Rs 25 Million 2012 Depreciable amount at 31 March Rs 15 Million 2012 Estimated future economic life at 30 Years 31 March 2012 Estimated fair value less costs to Rs 28 Million sell at 31 December 2012 Rs 16 Million 40 Years Rs 18 Million Property A was available for sale without modifications from 1 January 2013 onwards. On 31 March 2013 the directors of Aumi were reasonably confident that a sale could be secured for Rs28 Milion. However, after the year-end property prices in the area in which property A is located started to decline. This was due to an unexpected adverse local economic event in April 2013. Following this event the directors of Aumi estimated that property A would now be sold for Rs22 Million less selling costs and they are very confident that this lower price can be achieved. Property B needed repair work carried out on it before a sale could be completed. This repair work was carried out in the two-week period beginning 10 April 2013. The costs of this repair work are reflected in the estimated fair value less costs to sell figure for property B of Rs18 Million (see above). This estimate remains valid. Required: Calculate the carrying values of both properties in the statement of financial position of Aumi at 31 March 2013 and the amounts charged to the statement of comprehensive income for the year ended 31 March 2013, with appropriate explanations of the treatments you have adopted. [8 marks] On 1 January 2012 Millers Ltd opens a new factory and receives a government (d) grant of Rs15,000 in respect of capital equipment costing Rs100,000. It depreciates all plant and machinery at 20 % per annum straight-line. The policy of Millers Ltd is to treat the grant as a deferred credit. Page 2. Shew th Statuyut st Ancc ici exteba Page 3 of 12 Page 2. Required; Show the Steterment cf Fimene.bud Pesiti, extraurts in respect of the asset cind its related grant at 31 December Le12. [s marks] Tobal marks 25

Expert Answer:

Answer rating: 100% (QA)

Sol aUnder Fair Value Model Plant and Property should be consider on fair value aftr considering dep... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

The following situations relate to Bolivia Company. 1. Bolivia provides a warranty with all its products it sells. It estimates that it will sell 1,000,000 units of its product for the year ended...

-

The following situations relate to Bolivia Company. 1. Bolivia provides a warranty with all products sold. It estimates that it will sell 1,000,000 units of its product for the year ended December...

-

The following situations relate to Bolivia Company. 1. Bolivia provides a warranty with all its products it sells. It estimates that it will sell 1,000,000 units of its product for the year ended...

-

Problem 10 The Solow Growth Model is an exogenous model of economic growth that analyzes changes in the level of output in an economy over time as a result of changes in the population growth rate,...

-

Why would a company want a distributed database?

-

Using your estimates from Problem 8 and the fact that the correlation of A and B is 0.48, calculate the volatility (standard deviation) of a portfolio that is 70% invested in stock A and 30% invested...

-

What would happen to the SML graph in Figure 8.8 if expected inflation increased or decreased? Figure 8.8 268 269 270 271 272 273 274 275 A Required Rate of Return TH-13.0% SML: r, RF+RPM * b D E F H...

-

Macs Motel opened for business on May 1, 2017. Its trial balance before adjustment on May 31 is as follows. In addition to those accounts listed on the trial balance, the chart of accounts for Macs...

-

2. The armadillo is known as one of the world's fastest land animals. On one particular occasion, a biologist observed an armadillo named [N57E] for 6.00 s. The armadillo then ran 19.0 m [N23W]. What...

-

Reconsider the Lockhead Aircraft Co. problem presented in Problem 16.15 regarding a project to develop a new fighter airplane for the U.S. Air Force. Management is extremely concerned that current...

-

n = 3.72 mol of Hydrogen gas is initially at T = 306.0 K temperature and p = 2.56x105 Pa pressure. The gas is then reversibly and isothermally compressed until its pressure reaches pf = 9.92x105 Pa....

-

The following financial statement information is from five separate companies. Company A Company B Company C Company D Company E December 31, 2018 Assets $ 44,000 $ 34,320 $ 28,160 $ 78,320 $ 120,120...

-

2. Please respond to the following questions in a minimum of 250 words: a. Illustrate the transactional model. You may note that meanings exist among people (e.g., difference between "quitting" and...

-

Higher Order Thinking At the state fair, a person must be at least 138 centimeters tall to ride the roller coaster. Chiko wants to ride the coaster. He is 4 feet 7 inches tall. Is Chiko tall enough...

-

I. Determine the par yield rates (yields to maturity on par bonds) and forward rates (the ones with ? below) based on the spot curve given below. Make sure that you show your work, not just the...

-

Homeland Security Threat Analysis Free societies are at risk for terrorist acts for several reasons: a) loose control of public information; b) weapons, communications equipment, and explosives are...

-

4. Restructuring Moves Based on the assessment of JB Hi-Fi Australia brand portfolio, identify areas for downsizing and down scoping, and justify how would such a strategy result in improved...

-

What are some of the various ways to implement an awareness program?

-

Explain the difference between service cost and prior service cost.

-

James Kirk is a financial executive with McDowell Enterprises. Although James Kirk has not had any formal training in finance or accounting, he has a good sense for numbers and has helped the company...

-

Magilke Industries acquired equipment this year to be used in its operations. The equipment was delivered by the suppliers, installed by Magilke, and placed into operation. Some of it was purchased...

-

The book basis of depreciable assets for Erwin Co. is 900,000 and the tax basis is 700,000 at the end of 2015. The enacted tax rate is 34% for all periods. Determine the amount of deferred taxes to...

-

How does an asset gain or loss develop in pension accounting?

-

In January 2014, installation costs of 6,000 on new equipment were charged to Maintenance and Repairs Expense. Other costs of this equipment of 30,000 were correctly recorded and have been...

Study smarter with the SolutionInn App