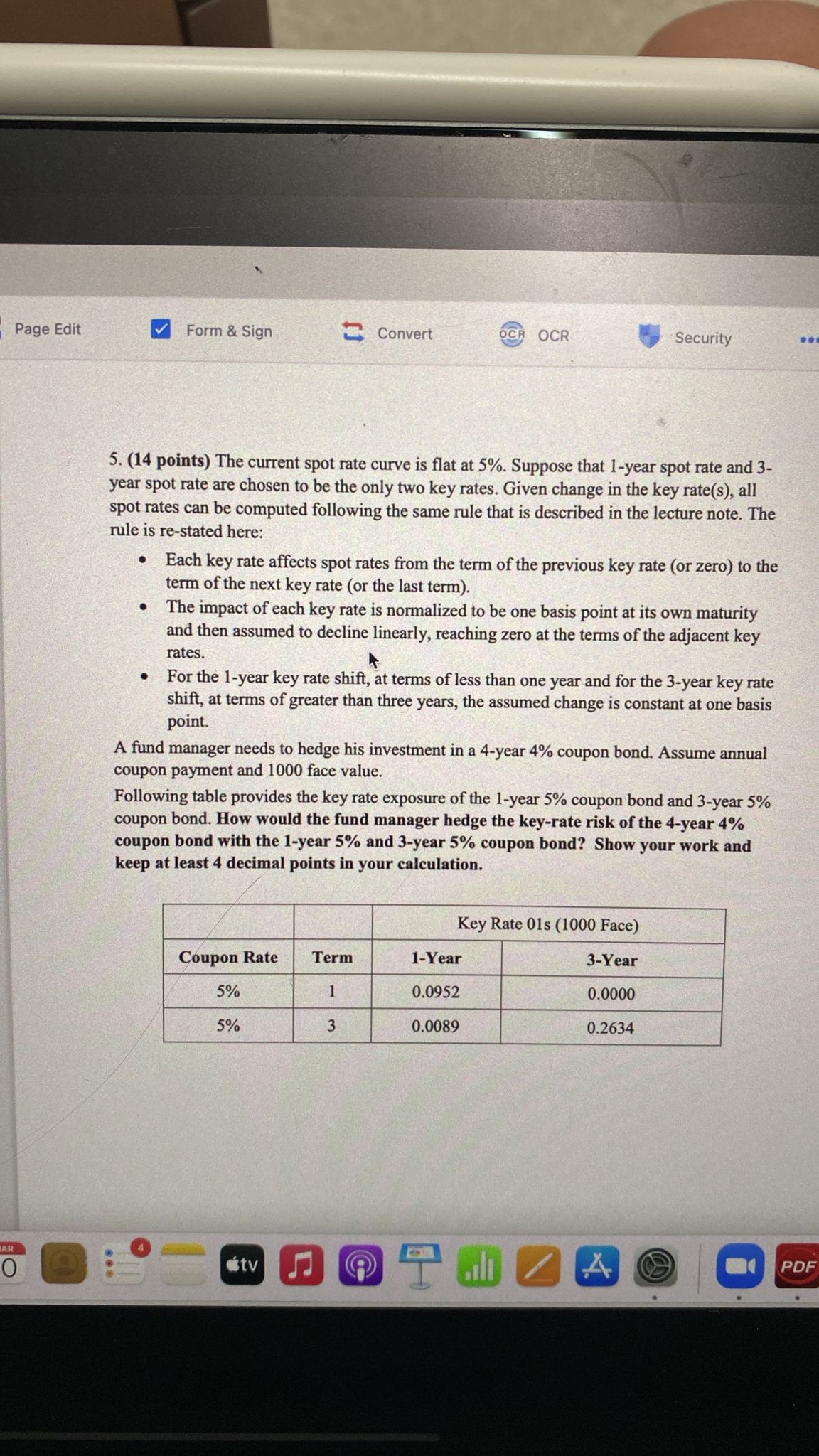

Question: Page Edit Form & Sign Convert OCR OCR Security 5. (14 points) The current spot rate curve is flat at 5%. Suppose that 1-year spot

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts