Question: PART 1 Fixed and Variable Cost Determinations Unit Cost Calculations The projected cost of a lamp is calculated based upon the projected increases or

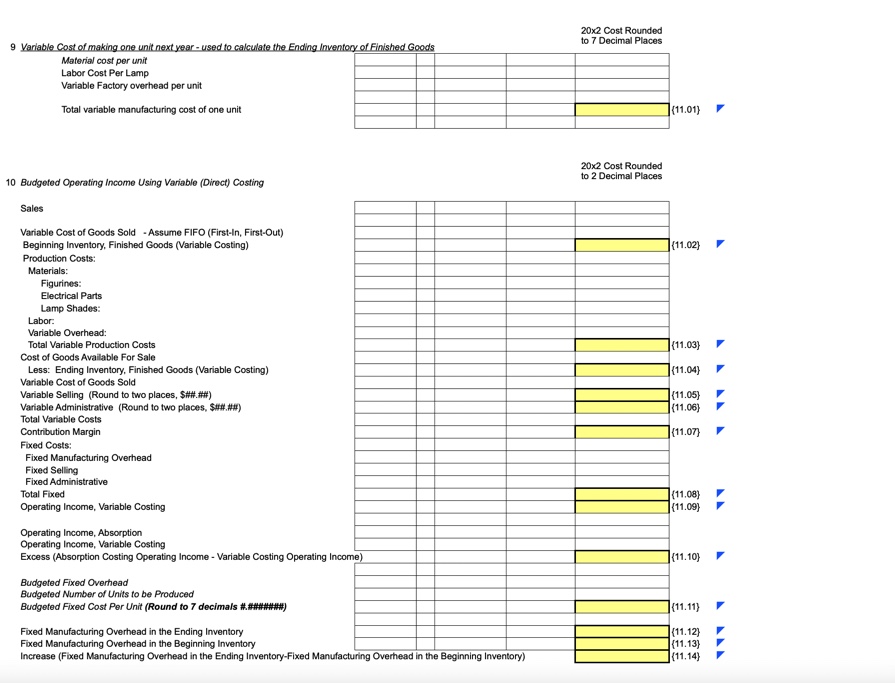

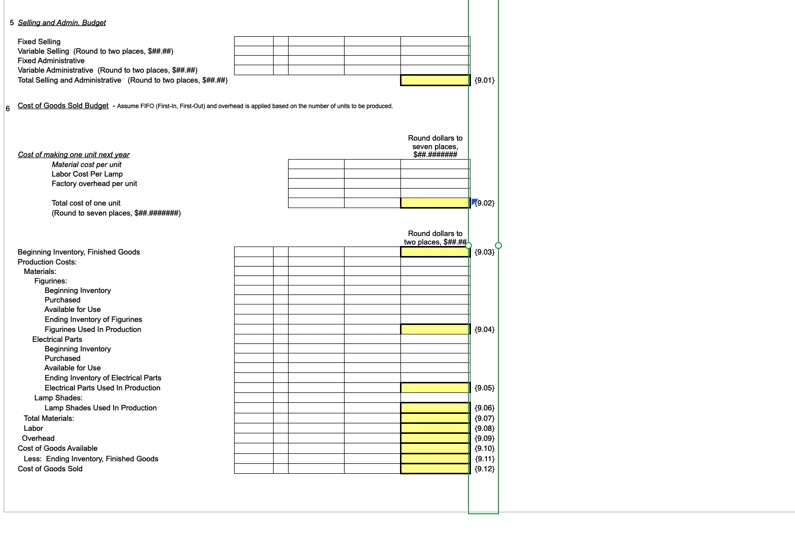

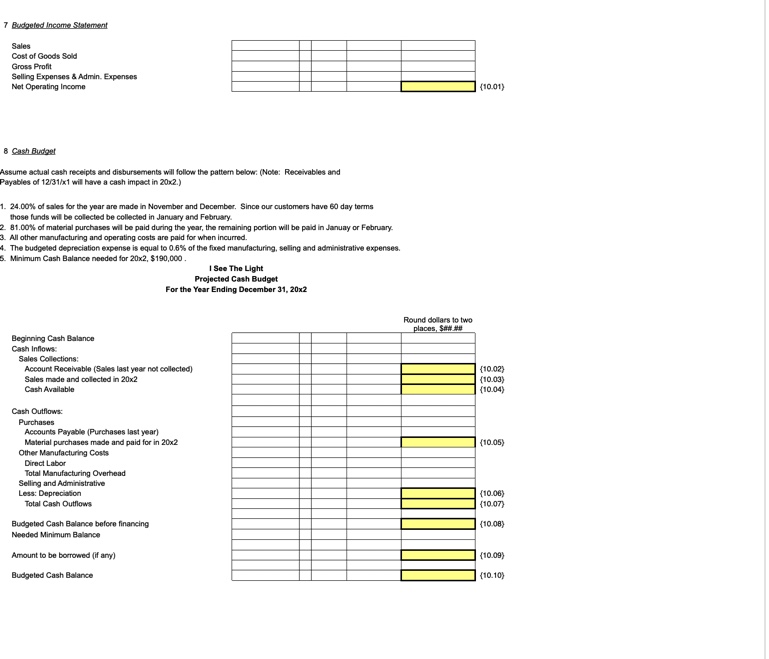

PART 1 Fixed and Variable Cost Determinations Unit Cost Calculations The projected cost of a lamp is calculated based upon the projected increases or decreases to current costs. The present costs to manufacture one lamp are: Figurines Electrical Sets Lamp Shade Direct Labor: Variable Overhead: Fixed Overhead: Cost per lamp: Expected increases for 20x2 $9.2000000 per lamp 1.2500000 per lamp 6.0000000 per lamp 2.2500000 per lamp (4 lamps/hr.) 0.2250000 per lamp 10.0000000 per lamp (based on normal capacity of 25,000 lamps) $28.9250000 per lamp When calculating projected increases round to SEVEN decimal places, $0.0000000. 1. Material Costs are expected to increase by 2.50%. 2. Labor Costs are expected to increase by 2.50%. 3. Variable Overhead is expected to increase by 6.00%. 4. Fixed Overhead is expected to increase to $265,000. 5. Fixed selling expenses are expected to be $29,000 in 20x2. 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 6.00% 7. Fixed Administrative expenses are expected to increase by $2,000. The total administrative expenses for 20x0 were $41,205.00, when 23,500 units were sold. Use the High-Low method to calculate the total fixed administrative expense. 8. Variable administrative expenses (measured on a per lamp basis) are expected to increase by 3.00%. The total administrative expenses for 20x0 were $41,205.00, when 23,500 units were sold. Use the High-Low method to calculate the variable administrative expense per lamp. On the following schedule develop the following figures: 1- 20x2 Projected Variable Manufacturing Unit Cost of a lamp. 2- 20x2 Projected Variable Unit Cost per lamp. 3- 20x2 Projected Fixed Costs. PART 3 Budgets Keep in mind that the budget section builds on work from the previous parts, including Part I as well as the Background Information (tabs 1-4). You should continue to use the same file with your previously submitted answers. Division N has decided to develop its budget based upon projected sales of 25,000 lamps at $54.00 per lamp. The company has requested that you prepare a master budget for the year. This budget is to be used for planning and control of operations and should be composed of: 1. Production Budget 2. Materials Budget 3. Direct Labor Budget 4. Factory Overhead Budget 5. Selling and Administrative Budget 6. Cost of Goods Sold Budget 7. Budgeted Income Statement 8. Cash Budget Notes for Budgeting: The company wants to maintain the same number of units in the beginning and ending inventories of work-in-process, and electrical parts while increasing the figurines inventory to 600 pieces and increasing the finished goods by 23.00%. Complete the following budgets 1 Production Budget Planned Sales Desired Ending Inventory of Finished Goods (roundup to the next unit) Total Needed Less: Beginning Inventory Total Production (7.01) Variable Manufacturing Unit Cost Figurines Electrical Sets Lamp Shade Labor I See The Light, Inc Schedule of Projected Costs 20x1 Cost Projected Percent Increase 20x2 Cost Rounded to 7 Decimal Places 9.2000000 2.50% $9.4300000 {4.01} 1.2500000 2.50% $1.2812500 (4.02) 6.0000000 2.50% $6.1500000 (4.03) 2.2500000 2.50% $2.3062500 {4.04) 0.2250000 6.00% $0.2385000 (4.05} $19.4060000 (4.06) Variable Overhead Projected Variable Manufacturing Cost Per Unit 18.9250000 Total Variable Cost Per Unit Variable Selling Variable Administrative 20x1 Variable Administrative 20x2 Projected Variable Manufacturing Unit Cost Projected Total Variable Cost Per Unit Schedule of Fixed Costs 20x1 Cost Projected Percent Increase 20x2 Cost Rounded to 7 Decimal Places 6.00% 3.1500000 3.3390000 (4.07) (4.08) 0.0309000 {4.09) 19.4060000 (4.06) 19.4369000 (4.10) 20x1 Cost Projected Increase 20x2 Cost Rounded to 2 Decimal Places Fixed Overhead $ 265,000.00 (4.11) (normal capacity of lamps @ Fixed Selling $ 29,000.00 (4.12} Fixed Administrative 20x1 Fixed Administrative 20x2 40,500.00 (4.13) $ 42,500.00 {4.14} Projected Total Fixed Costs $ 336,500.00 (4.15) I See The Light Projected Income Statement For the Period Ending December 31, 20x1 Sales Cost of Goods Sold Gross Profit Selling Expenses: Fixed Variable 25,000 lamps @$45.00 @ $28.93 Administrative Expenses $ 1,125,000.00 723,250.00 $ 401,750.00 mission per unit) @$3.15 $ 23,000.00 78,750.00 $101,750.00 41,250.00 $ Total Selling and Administrative Expenses: Net Profit I See The Light Projected Balance Sheet As of December 31, 20x1 Current Assets Cash Accounts Receivable Inventory Raw Material Figurines Electrical Sets Work in Process Finished Goods Total Current Assets Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets 500 @ $9.20 500 @$1.25 0 3000 @ $28.9250 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity 143,000.00 258,750.00 $ 34,710.00 67,500.00 4,600.00 625.00 86,775.00 194,210.00 $ 20,000.00 6,800.00 13,200.00 $ 207,410.00 $ 12,000.00 141,410.00 54,000.00 54,000.00 153,410.00 207.410.00 9 Variable Cost of making one unit next year - used to calculate the Ending Inventory of Finished Goods Material cost per unit Labor Cost Per Lamp Variable Factory overhead per unit Total variable manufacturing cost of one unit 20x2 Cost Rounded to 7 Decimal Places 10 Budgeted Operating Income Using Variable (Direct) Costing Sales Variable Cost of Goods Sold Assume FIFO (First-In, First-Out) Beginning Inventory, Finished Goods (Variable Costing) Production Costs: Materials: Figurines: Electrical Parts 20x2 Cost Rounded to 2 Decimal Places (11.01) {11.02} Lamp Shades: Labor: Variable Overhead: Total Variable Production Costs Cost of Goods Available For Sale Less: Ending Inventory, Finished Goods (Variable Costing) Variable Cost of Goods Sold Variable Selling (Round to two places, $##.###) Variable Administrative (Round to two places, $##.##) Total Variable Costs Contribution Margin Fixed Costs: Fixed Manufacturing Overhead Fixed Selling Fixed Administrative Total Fixed Operating Income, Variable Costing Operating Income, Absorption Operating Income, Variable Costing Excess (Absorption Costing Operating Income - Variable Costing Operating Income) Budgeted Fixed Overhead Budgeted Number of Units to be Produced Budgeted Fixed Cost Per Unit (Round to 7 decimals ########) Fixed Manufacturing Overhead in the Ending Inventory (11.03) {11.04) (11.05) {11.06} {11.07} (11.08) (11.09) (11.10) (11.11) (11.12) (11.13) Increase (Fixed Manufacturing Overhead in the Ending Inventory-Fixed Manufacturing Overhead in the Beginning Inventory) (11.14) Fixed Manufacturing Overhead in the Beginning Inventory 5 Selling and Admin. Budget Fixed Selling Variable Selling (Round to two places, $0.00) Fixed Administrative Variable Administrative (Round to two places, $##.#) Total Selling and Administrative (Round to two places, $##.NW) 6 Cost of Goods Sold Budget - Assume FIFO (First-In, First-Out) and overhead is applied based on the number of units to be produced. Cost of making one unit next year Material cost per unit Labor Cost Per Lamp Factory overhead per unit Total cost of one unit (Round to seven places, $##.##) Beginning Inventory, Finished Goods Production Costs: Materials: Figurines: Beginning Inventory Purchased Available for Use Ending Inventory of Figurines Figurines Used In Production Electrical Parts Beginning Inventory Purchased Available for Use Ending Inventory of Electrical Parts Electrical Parts Used In Production Lamp Shades: Lamp Shades Used In Production Total Materials: Round dollars to seven places, (9.01) 9.02) Round dollars to two places, SNN (9.03) (9.04) (9.05) (9.06) (9.07) Labor (9.08) Overhead (9.09) Cost of Goods Available (9.10) Less: Ending Inventory, Finished Goods (9.11) Cost of Goods Sold (9.12) 7 Budgeted Income Statement Sales Cost of Goods Sold Gross Profit Selling Expenses & Admin. Expenses Net Operating Income 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattern below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 24.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February. 2 81.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February. 3. All other manufacturing and operating costs are paid for when incurred. 4. The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. 5. Minimum Cash Balance needed for 20x2, $190,000. I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) Sales made and collected in 20x2 Cash Available Cash Outflows: Purchases Accounts Payable (Purchases last year) Material purchases made and paid for in 20x2 Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative Less: Depreciation Total Cash Outflows Budgeted Cash Balance before financing Needed Minimum Balance Amount to be borrowed (if any) Budgeted Cash Balance Round dollars to two places, $##.## (10.01) (10.02) (10.03) (10.04) (10.05) (10.06) {10.07) (10.08) (10.09) (10.10)

Step by Step Solution

There are 3 Steps involved in it

Lets work through the problem step by step Physical Flow of Units January WorkinProcessBeginning Units Started this Period Units to Account for Total units transferred out 10000 units WorkinProcessEnd... View full answer

Get step-by-step solutions from verified subject matter experts