Question: Part 1 Part 2 Part 3 Required Su Chan resides in Vancouver, BC, and has been employed by YYZ Ltd. for a number of years

Part 1

Part 2

Part 3

Required

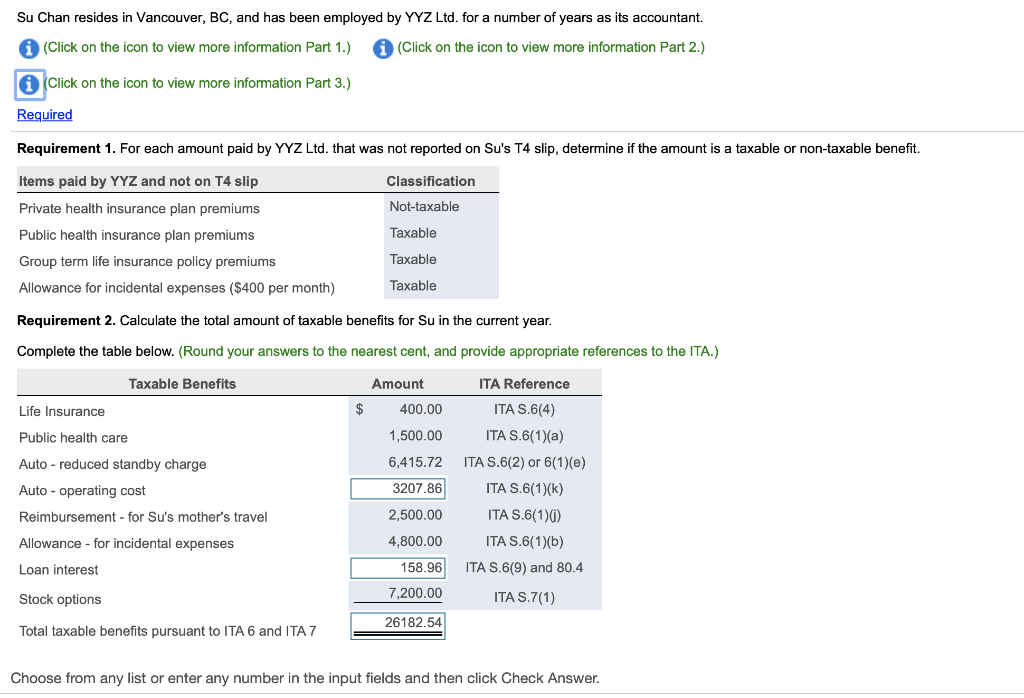

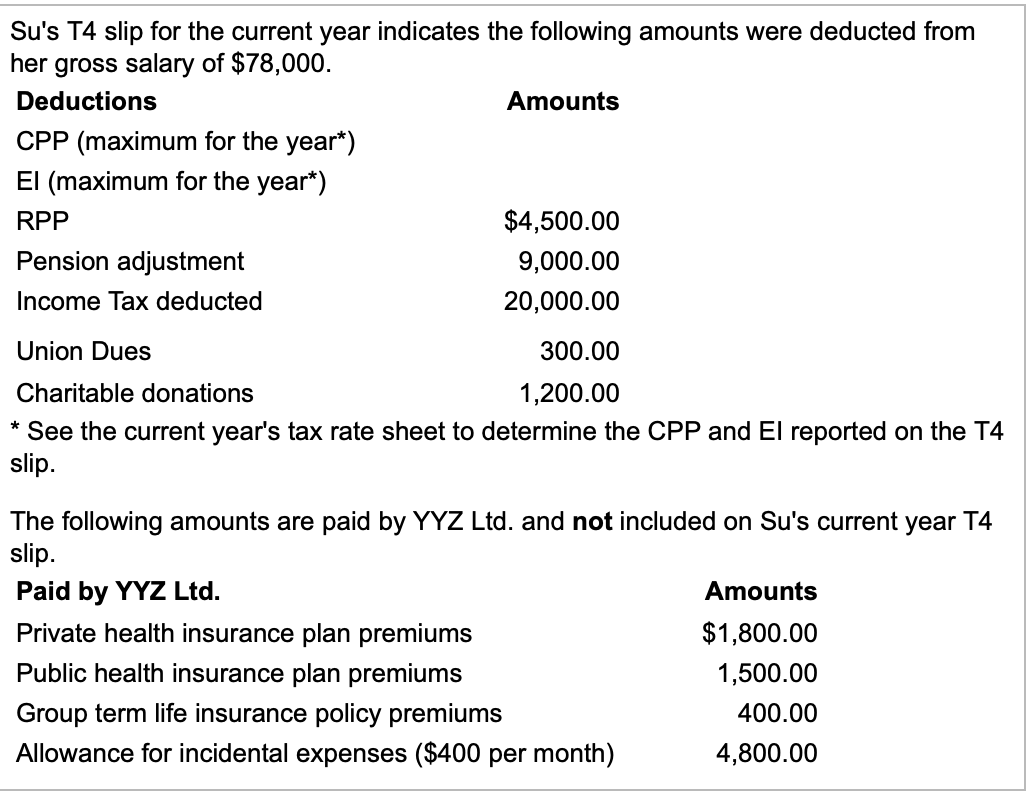

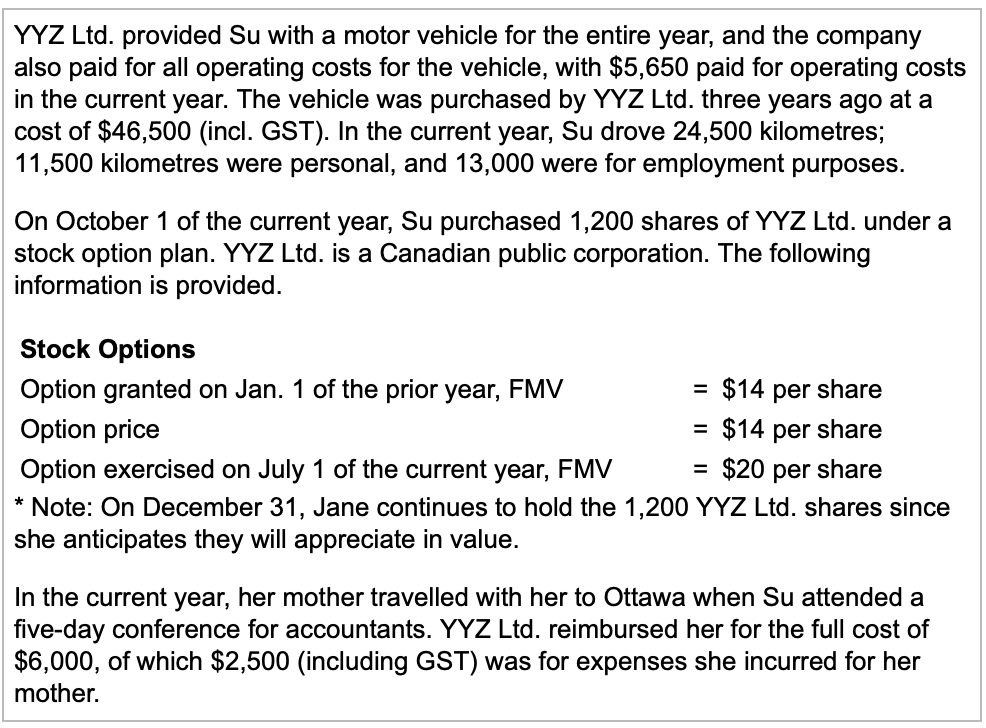

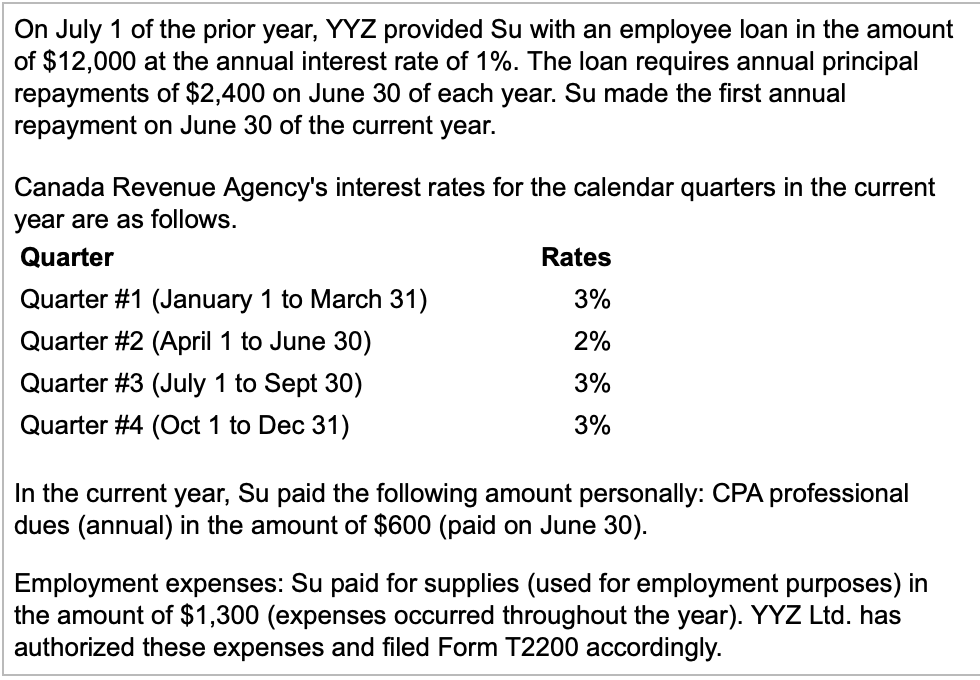

Su Chan resides in Vancouver, BC, and has been employed by YYZ Ltd. for a number of years as its accountant. (Click on the icon to view more information Part 1.) (Click on the icon to view more information Part 2.) Click on the icon to view more information Part 3.) Required Requirement 1. For each amount paid by YYZ Ltd. that was not reported on Su's T4 slip, determine if the amount is a taxable or non-taxable benefit. Classification Not-taxable Items paid by YYZ and not on T4 slip Private health insurance plan premiums Public health insurance plan premiums Group term life insurance policy premiums Allowance for incidental expenses ($400 per month) Taxable Taxable Taxable Requirement 2. Calculate the total amount of taxable benefits for Su in the current year. Complete the table below. (Round your answers to the nearest cent, and provide appropriate references to the ITA.) Taxable Benefits Amount ITA Reference ITA S.6(4) Life Insurance $ 400.00 Public health care 1,500.00 Auto - reduced standby charge Auto-operating cost Reimbursement - for Su's mother's travel Allowance - for incidental expenses 6,415.72 3207.86 2,500.00 4,800.00 ITA S.6(1)(a) ITA S.6(2) or 6(1)(e ITA S.6(1)(k) ITA S.6(1)0) ITA S.6(1)(b) ITA S.6(9) and 80.4 ITA S.7(1) Loan interest 158.96 Stock options 7,200.00 26182.54 Total taxable benefits pursuant to ITA 6 and ITA 7 Choose from any list or enter any number in the input fields and then click Check Answer. Su's T4 slip for the current year indicates the following amounts were deducted from her gross salary of $78,000. Deductions Amounts CPP (maximum for the year*) El (maximum for the year*) RPP $4,500.00 Pension adjustment 9,000.00 Income Tax deducted 20,000.00 Union Dues 300.00 Charitable donations 1,200.00 * See the current year's tax rate sheet to determine the CPP and El reported on the T4 slip. The following amounts are paid by YYZ Ltd. and not included on Su's current year T4 slip. Paid by YYZ Ltd. Amounts Private health insurance plan premiums $1,800.00 Public health insurance plan premiums 1,500.00 Group term life insurance policy premiums 400.00 Allowance for incidental expenses ($400 per month) 4,800.00 YYZ Ltd. provided Su with a motor vehicle for the entire year, and the company also paid for all operating costs for the vehicle, with $5,650 paid for operating costs in the current year. The vehicle was purchased by YYZ Ltd. three years ago at a cost of $46,500 (incl. GST). In the current year, Su drove 24,500 kilometres; 11,500 kilometres were personal, and 13,000 were for employment purposes. On October 1 of the current year, Su purchased 1,200 shares of YYZ Ltd. under a stock option plan. YYZ Ltd. is a Canadian public corporation. The following information is provided. Stock Options Option granted on Jan. 1 of the prior year, FMV = $14 per share Option price = $14 per share Option exercised on July 1 of the current year, FMV $20 per share * Note: On December 31, Jane continues to hold the 1,200 YYZ Ltd. shares since she anticipates they will appreciate in value. In the current year, her mother travelled with her to Ottawa when Su attended a five-day conference for accountants. YYZ Ltd. reimbursed her for the full cost of $6,000, of which $2,500 (including GST) was for expenses she incurred for her mother. On July 1 of the prior year, YYZ provided Su with an employee loan in the amount of $12,000 at the annual interest rate of 1%. The loan requires annual principal repayments of $2,400 on June 30 of each year. Su made the first annual repayment on June 30 of the current year. Canada Revenue Agency's interest rates for the calendar quarters in the current year are as follows. Quarter Rates Quarter #1 (January 1 to March 31) 3% Quarter #2 (April 1 to June 30) 2% Quarter #3 (July 1 to Sept 30) 3% Quarter #4 (Oct 1 to Dec 31) 3% In the current year, Su paid the following amount personally: CPA professional dues (annual) in the amount of $600 (paid on June 30). Employment expenses: Su paid for supplies (used for employment purposes) in the amount of $1,300 (expenses occurred throughout the year). YYZ Ltd. has authorized these expenses and filed Form T2200 accordingly. X Required 1. For each amount paid by YYZ Ltd. that was not reported on Su's T4 slip, determine if the amount is a taxable or non-taxable benefit. 2. Calculate the total amount of taxable benefits for Su in the current year and provide appropriate references to the ITA. 3. Calculate Su's net employment income for the current year in accordance with sections 5 to 8 of the Income Tax Act. Round your calculations to the nearest dollar, and provide appropriate references to the ITA. Print Done Su Chan resides in Vancouver, BC, and has been employed by YYZ Ltd. for a number of years as its accountant. (Click on the icon to view more information Part 1.) (Click on the icon to view more information Part 2.) Click on the icon to view more information Part 3.) Required Requirement 1. For each amount paid by YYZ Ltd. that was not reported on Su's T4 slip, determine if the amount is a taxable or non-taxable benefit. Classification Not-taxable Items paid by YYZ and not on T4 slip Private health insurance plan premiums Public health insurance plan premiums Group term life insurance policy premiums Allowance for incidental expenses ($400 per month) Taxable Taxable Taxable Requirement 2. Calculate the total amount of taxable benefits for Su in the current year. Complete the table below. (Round your answers to the nearest cent, and provide appropriate references to the ITA.) Taxable Benefits Amount ITA Reference ITA S.6(4) Life Insurance $ 400.00 Public health care 1,500.00 Auto - reduced standby charge Auto-operating cost Reimbursement - for Su's mother's travel Allowance - for incidental expenses 6,415.72 3207.86 2,500.00 4,800.00 ITA S.6(1)(a) ITA S.6(2) or 6(1)(e ITA S.6(1)(k) ITA S.6(1)0) ITA S.6(1)(b) ITA S.6(9) and 80.4 ITA S.7(1) Loan interest 158.96 Stock options 7,200.00 26182.54 Total taxable benefits pursuant to ITA 6 and ITA 7 Choose from any list or enter any number in the input fields and then click Check Answer. Su's T4 slip for the current year indicates the following amounts were deducted from her gross salary of $78,000. Deductions Amounts CPP (maximum for the year*) El (maximum for the year*) RPP $4,500.00 Pension adjustment 9,000.00 Income Tax deducted 20,000.00 Union Dues 300.00 Charitable donations 1,200.00 * See the current year's tax rate sheet to determine the CPP and El reported on the T4 slip. The following amounts are paid by YYZ Ltd. and not included on Su's current year T4 slip. Paid by YYZ Ltd. Amounts Private health insurance plan premiums $1,800.00 Public health insurance plan premiums 1,500.00 Group term life insurance policy premiums 400.00 Allowance for incidental expenses ($400 per month) 4,800.00 YYZ Ltd. provided Su with a motor vehicle for the entire year, and the company also paid for all operating costs for the vehicle, with $5,650 paid for operating costs in the current year. The vehicle was purchased by YYZ Ltd. three years ago at a cost of $46,500 (incl. GST). In the current year, Su drove 24,500 kilometres; 11,500 kilometres were personal, and 13,000 were for employment purposes. On October 1 of the current year, Su purchased 1,200 shares of YYZ Ltd. under a stock option plan. YYZ Ltd. is a Canadian public corporation. The following information is provided. Stock Options Option granted on Jan. 1 of the prior year, FMV = $14 per share Option price = $14 per share Option exercised on July 1 of the current year, FMV $20 per share * Note: On December 31, Jane continues to hold the 1,200 YYZ Ltd. shares since she anticipates they will appreciate in value. In the current year, her mother travelled with her to Ottawa when Su attended a five-day conference for accountants. YYZ Ltd. reimbursed her for the full cost of $6,000, of which $2,500 (including GST) was for expenses she incurred for her mother. On July 1 of the prior year, YYZ provided Su with an employee loan in the amount of $12,000 at the annual interest rate of 1%. The loan requires annual principal repayments of $2,400 on June 30 of each year. Su made the first annual repayment on June 30 of the current year. Canada Revenue Agency's interest rates for the calendar quarters in the current year are as follows. Quarter Rates Quarter #1 (January 1 to March 31) 3% Quarter #2 (April 1 to June 30) 2% Quarter #3 (July 1 to Sept 30) 3% Quarter #4 (Oct 1 to Dec 31) 3% In the current year, Su paid the following amount personally: CPA professional dues (annual) in the amount of $600 (paid on June 30). Employment expenses: Su paid for supplies (used for employment purposes) in the amount of $1,300 (expenses occurred throughout the year). YYZ Ltd. has authorized these expenses and filed Form T2200 accordingly. X Required 1. For each amount paid by YYZ Ltd. that was not reported on Su's T4 slip, determine if the amount is a taxable or non-taxable benefit. 2. Calculate the total amount of taxable benefits for Su in the current year and provide appropriate references to the ITA. 3. Calculate Su's net employment income for the current year in accordance with sections 5 to 8 of the Income Tax Act. Round your calculations to the nearest dollar, and provide appropriate references to the ITA. Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts