Question: Part 2: Interest Rate Swaps Use the following term structure of zero-coupon yields to answer the questions below. 0.5 Maturity (years) r (spot rate) 0.02

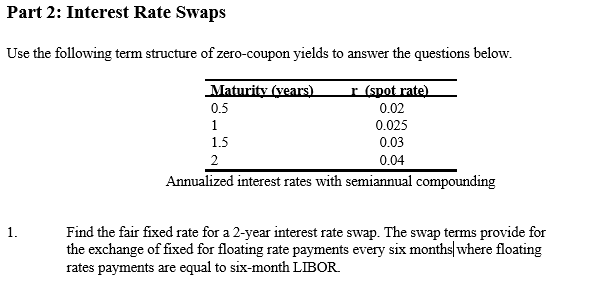

Part 2: Interest Rate Swaps Use the following term structure of zero-coupon yields to answer the questions below. 0.5 Maturity (years) r (spot rate) 0.02 1 0.025 1.5 0.03 2 0.04 Annualized interest rates with semiannual compounding 1. Find the fair fixed rate for a 2-year interest rate swap. The swap terms provide for the exchange of fixed for floating rate payments every six months where floating rates payments are equal to six-month LIBOR Part 2: Interest Rate Swaps Use the following term structure of zero-coupon yields to answer the questions below. 0.5 Maturity (years) r (spot rate) 0.02 1 0.025 1.5 0.03 2 0.04 Annualized interest rates with semiannual compounding 1. Find the fair fixed rate for a 2-year interest rate swap. The swap terms provide for the exchange of fixed for floating rate payments every six months where floating rates payments are equal to six-month LIBOR

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts