Question: Part 4 B and C Managerial Project Part 4 Direct labor or machine hours may not be the appropriate cost driver for overhead in all

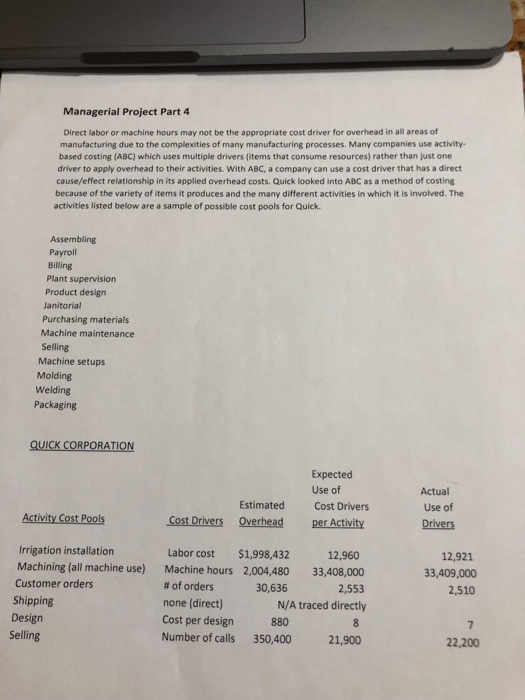

Managerial Project Part 4 Direct labor or machine hours may not be the appropriate cost driver for overhead in all areas of manufacturing due to the complexities of many manufacturing processes. Many companies use activity based costing (ABC) which uses multiple drivers (items that consume resources) rather than just one driver to apply overhead to their activities. With ABC, a company can use a cost driver that has a direct cause/effect relationship in its applied overhead costs. Quick looked into ABC as a method of costing because of the variety of items it produces and the many different activities in which it is involved. The activitles listed below are a sample of possible cost pools for Quick. Assembling Payroll Plant supervision Product design Janitorial Purchasing materials Machine maintenance Selling Machine setups Molding Welding Packaging QUICK CORPORATION Expected Use of Cost Drivers Actual Use of Drivers Estimated Activity Cost Pools Cost Drivers Overhead per Activity Irrigation installation Machining (all machine use) Customer orders Shipping Design Selling Labor cost $1,998,432 2,004,480 12,921 33,409,000 2,510 Machine hours # of orders none (direct) Cost per design Number of calls 33,408,000 2,553 N/A traced directly 30,636 880 350,400 21,900 22,200

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts