Question: Part A Assume that the variable Wt follows the AR(1) model: yt = 1.7+ 0.65 yt-1 + Et where Et is a Normally distributed i.i.d.

Part A

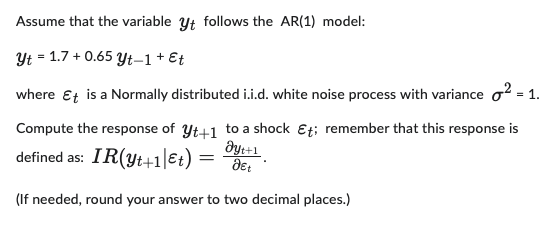

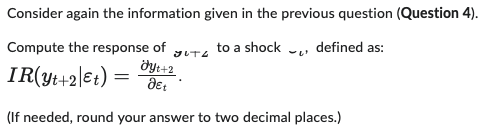

Assume that the variable Wt follows the AR(1) model: yt = 1.7+ 0.65 yt-1 + Et where Et is a Normally distributed i.i.d. white noise process with variance o? = 1. Compute the response of Ut] to a shock &; remember that this response is defined as: IR(yt+1 8t) = dyt+ 1 aEt (If needed, round your answer to two decimal places.)Consider again the information given in the previous question (Question 4). Compute the response of yup to a shock _ , defined as: IR(y+ +2 Et) dyt + 2 det (If needed, round your answer to two decimal places.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock