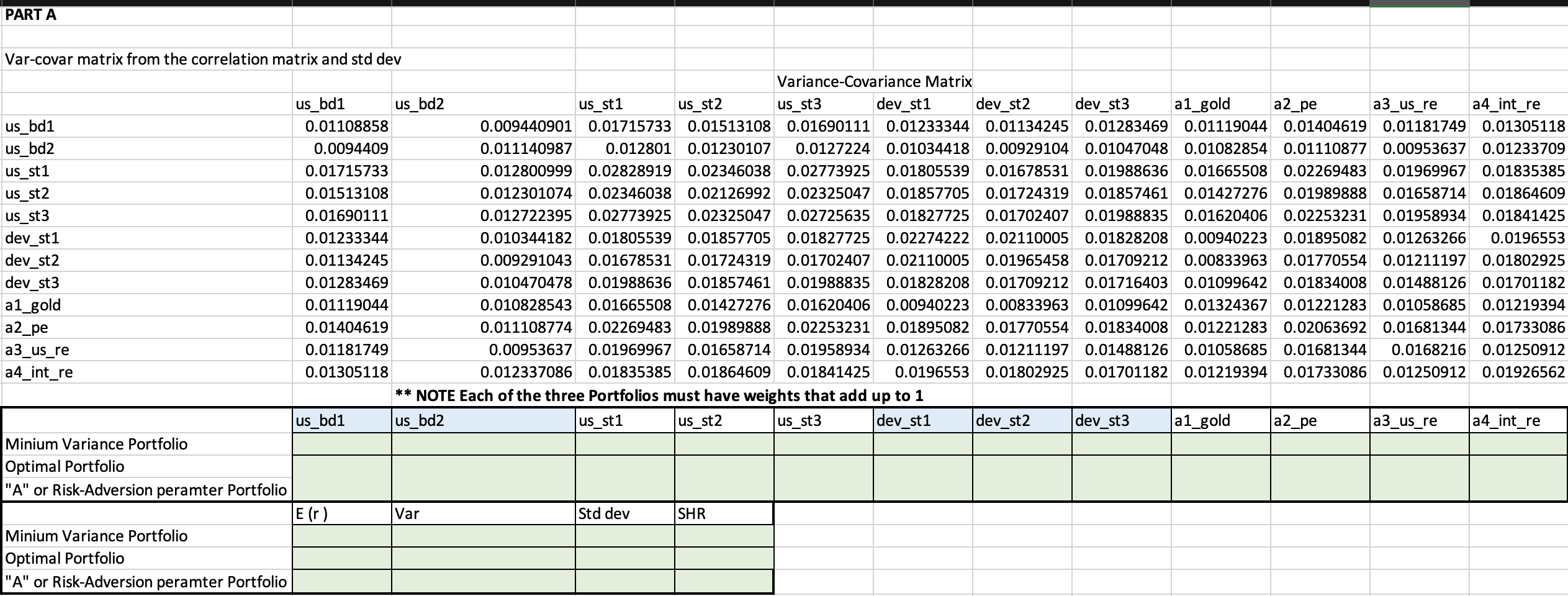

Part A: Create Minimum-Variance Portfolio & Optimal Portfolio for the set of 12 Asset classes detailed below.

Fantastic news! We've Found the answer you've been seeking!

Question:

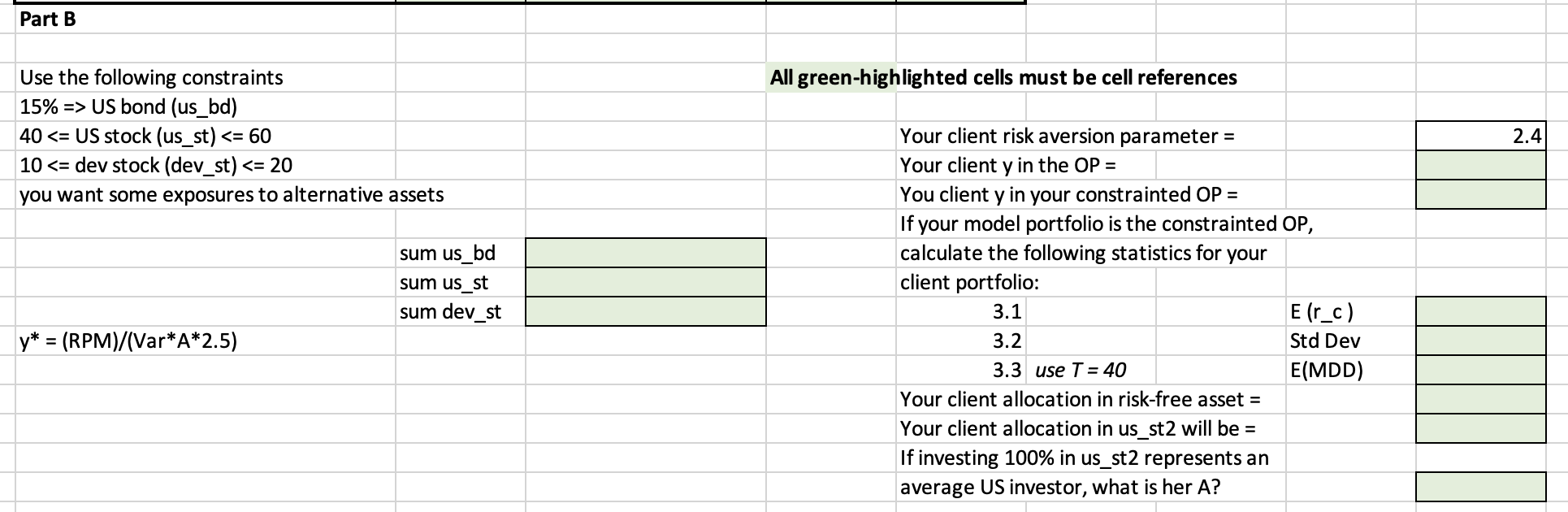

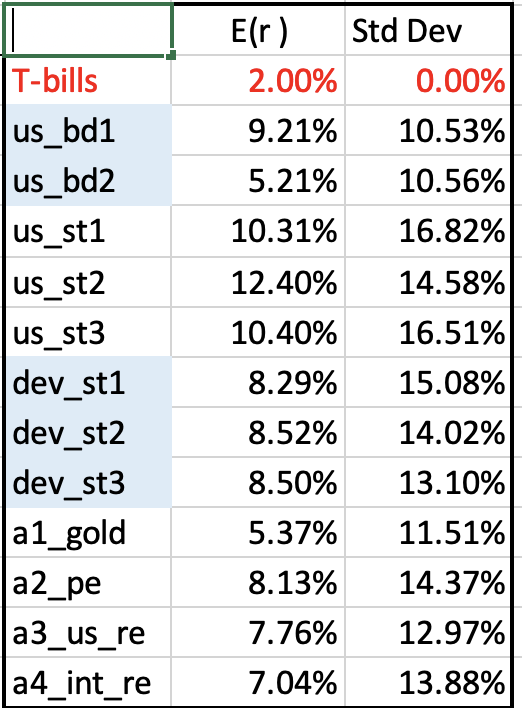

Part A: Create Minimum-Variance Portfolio & Optimal Portfolio for the set of 12 Asset classes detailed below. We are given information related to each class's respective Expected Return-E (r) & Standard Deviation. Following this data; the next table details the Var-CoVar Matrix between asset class pairs. Following finding these two portfolios in Part A, we will use this information to create an adjusted portfolio based on the findings in part A for a client with a specific risk-aversion appetite which is detailed in a table following Part B.

Expert Answer:

Related Book For

Posted Date: