Question: Part a. When rt > at > btt), then an arbitrage must exist. Part b. When rt > bt(k) > at, then an arbitrage is

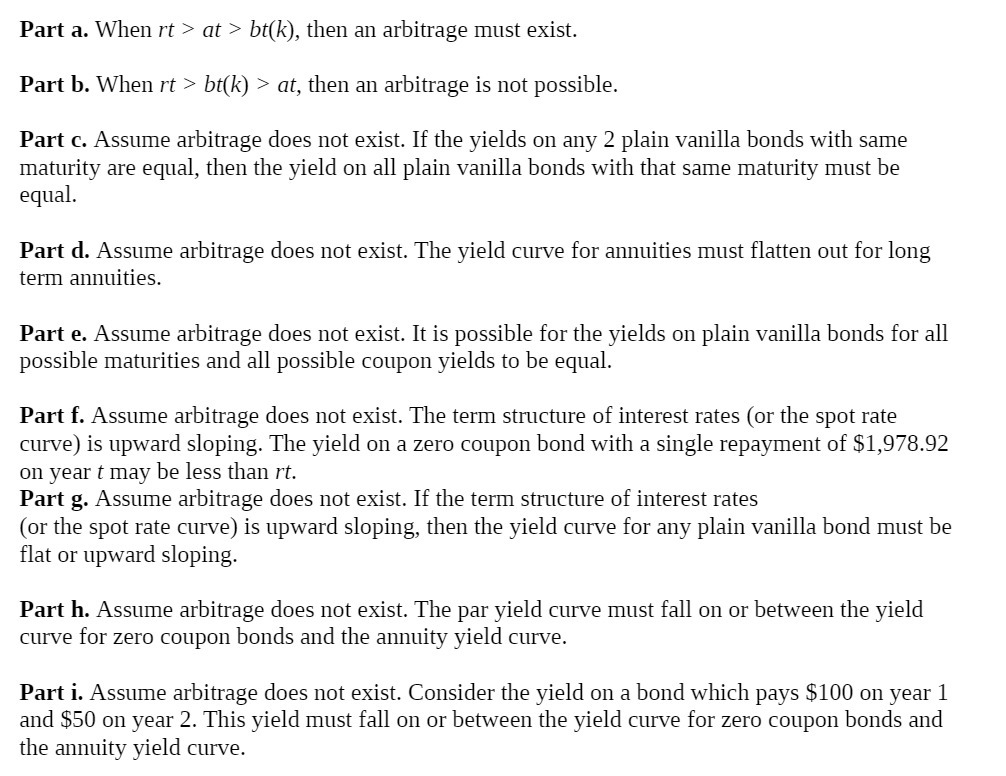

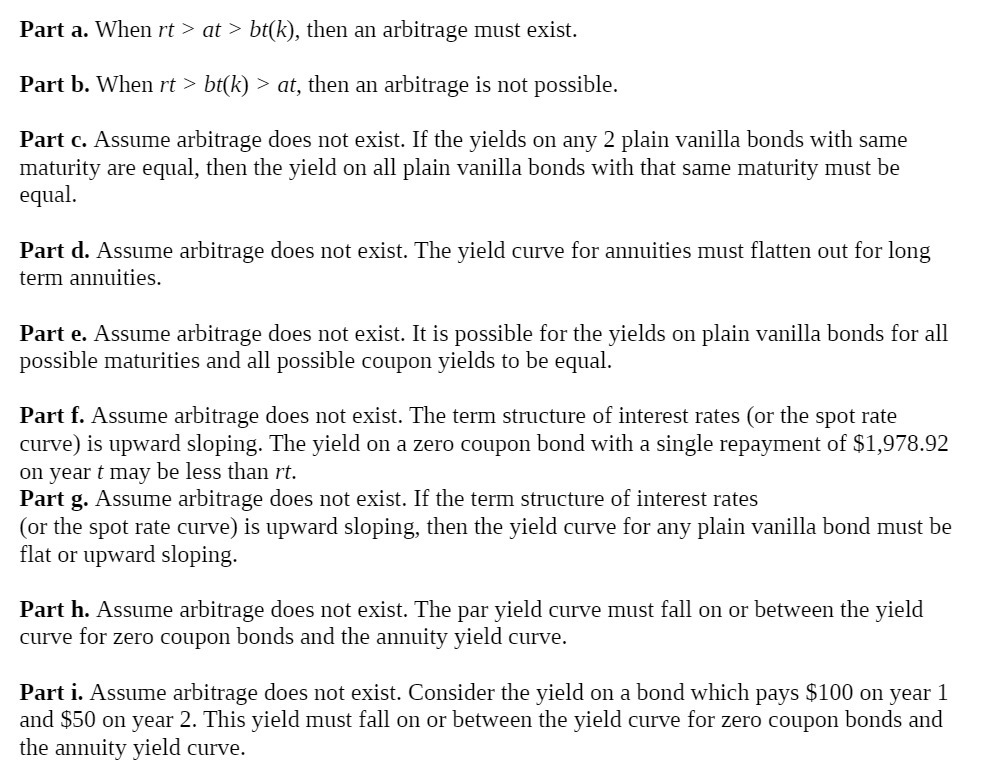

Part a. When rt > at > btt), then an arbitrage must exist. Part b. When rt > bt(k) > at, then an arbitrage is not possible. Part c. Assume arbitrage does not exist. If the yields on any 2 plain vanilla bonds with same maturity are equal, then the yield on all plain vanilla bonds with that same maturity must be equal. Part (1. Assume arbitrage does not exist. The yield curve for annuities must flatten out for long term annuities. Part e. Assume arbitrage does not exist. It is possible for the yields on plain vanilla bonds for all possible maturities and all possible coupon yields to be equal. Part f. Assume arbitrage does not exist. The term structure of interest rates (or the spot rate curve) is upward sloping. The yield on a zero coupon bond with a single repayment of $1,978.92 on year tmay be less than rt. Part g. Assume arbitrage does not exist. If the term structure of interest rates (or the spot rate curve) is upward sloping, then the yield curve for any plain vanilla bond must be at or upward sloping. Part h. Assume arbitrage does not exist. The par yield curve must fall on or between the yield curve for zero coupon bonds and the annuity yield curve. Part i. Assume arbilIage does not exist. Consider the yield on a bond which pays $100 on year 1 and $50 on year 2. This yield must fall on or between the yield curve for zero coupon bonds and the annuity yield curve

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts