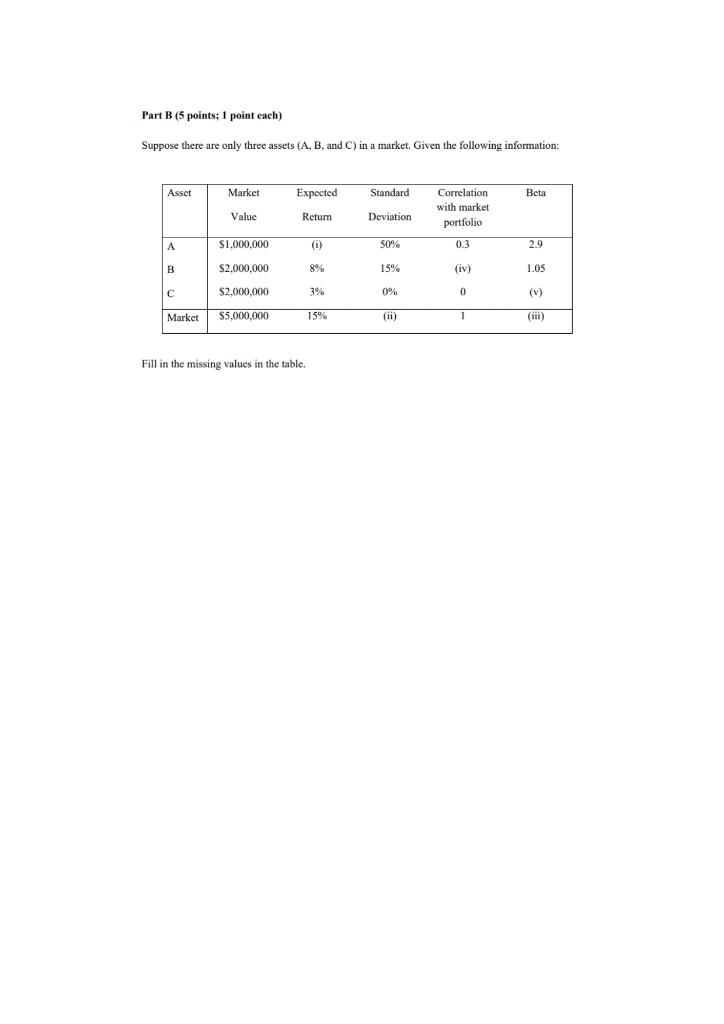

Question: Part B (5 points: 1 point each) Suppose there are only three assets (A, B. and C) in a market. Given the following information: Asset

Part B (5 points: 1 point each) Suppose there are only three assets (A, B. and C) in a market. Given the following information: Asset Market Expected Standard Beta Correlation with market portfolio Value Retum Deviation $1,000,000 (0) 50% 0. 2.9 B S2.000.000 8% 15% (iv) 1.05 $2.000.000 3% 0% (v) Market $5,000,000 15% (ii) 1 (ili) Fill in the missing values in the table

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock