Question: part C and D only 1(b) Calculate the expected return and standard deviation of a portfolio consisting of an equity security (E), and a debt

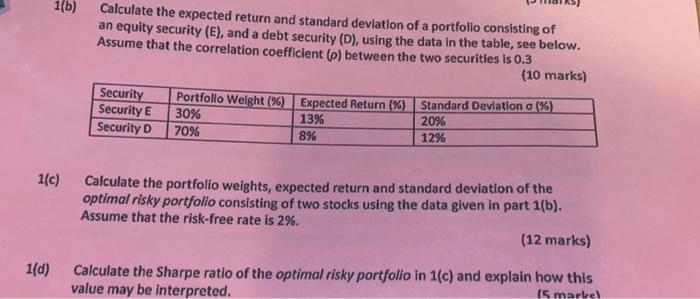

1(b) Calculate the expected return and standard deviation of a portfolio consisting of an equity security (E), and a debt security (D), using the data in the table, see below. Assume that the correlation coefficient (e) between the two securities is 0.3 (10 marks) Security Security E Security D Portfolio Weight %) Expected Return (%) 30% 13% 70% 8% Standard Deviation (%) 20% 1296 1(c) Calculate the portfolio weights, expected return and standard deviation of the optimal risky portfolio consisting of two stocks using the data given in part 1(b). Assume that the risk-free rate is 2%. (12 marks) 1(d) Calculate the Sharpe ratio of the optimal risky portfolio in 1(c) and explain how this value may be interpreted. (5 marvel

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts