Question: Part C: Option Pricing using Replicating Portfolios Approach In this section, you are required to use the replicating portfolio approach to calculate the value of

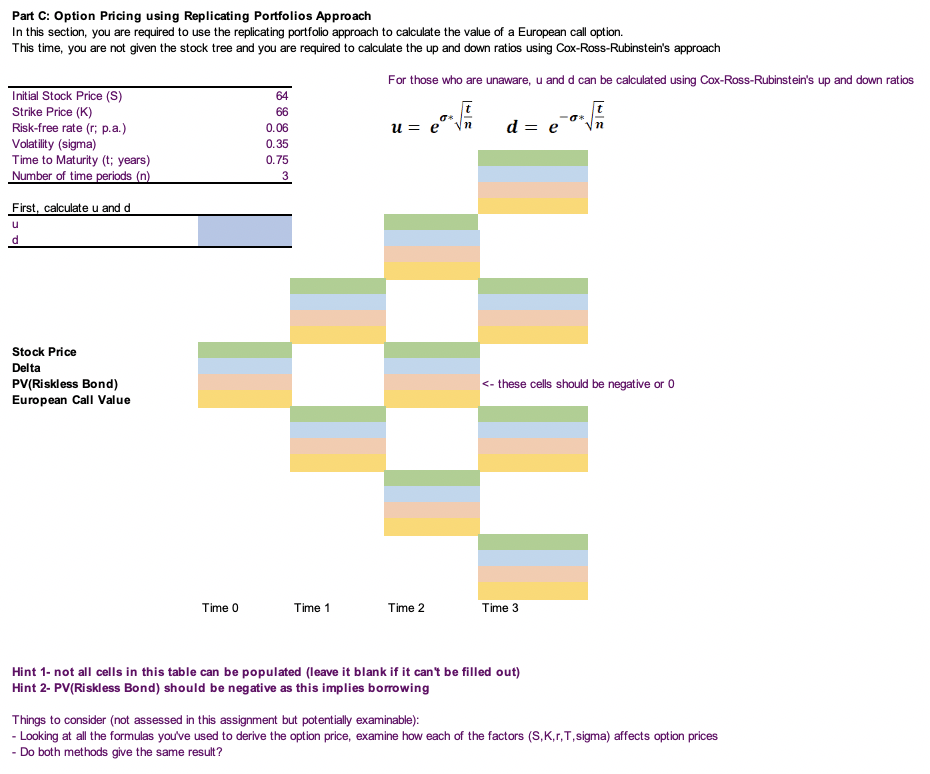

Part C: Option Pricing using Replicating Portfolios Approach In this section, you are required to use the replicating portfolio approach to calculate the value of a European call option. This time, you are not given the stock tree and you are required to calculate the up and down ratios using Cox-Ross-Rubinstein's approach For those who are unaware, u and d can be calculated using Cox-Ross-Rubinstein's up and down ratios earth 64 66 0.06 0.35 0.75 3 u= e n d = e Initial Stock Price (S) Strike Price (K) Risk-free rate (r; p.a.) Volatility (sigma) Time to Maturity (t; years) Number of time periods (n) First, calculate u and d u d Stock Price Delta PV(Riskless Bond) European Call Value

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts