Question: Part Three Instructions In this part of the practice set, the student will prepare a T-Account for each account and calculate the ending balance in

Part Three Instructions In this part of the practice set, the student will prepare a T-Account for each account and calculate the ending balance in each T-Account. In Blackboard the student will write: Dr or Cr (depending on the balance in the account) then the account number, then the dollar amount. Here is an example: Dr 10000 $5,345.00 or Cr 20000 $4,110.00 Only write whether it has a debit or credit balance then the account number then the dollar amount for each account.

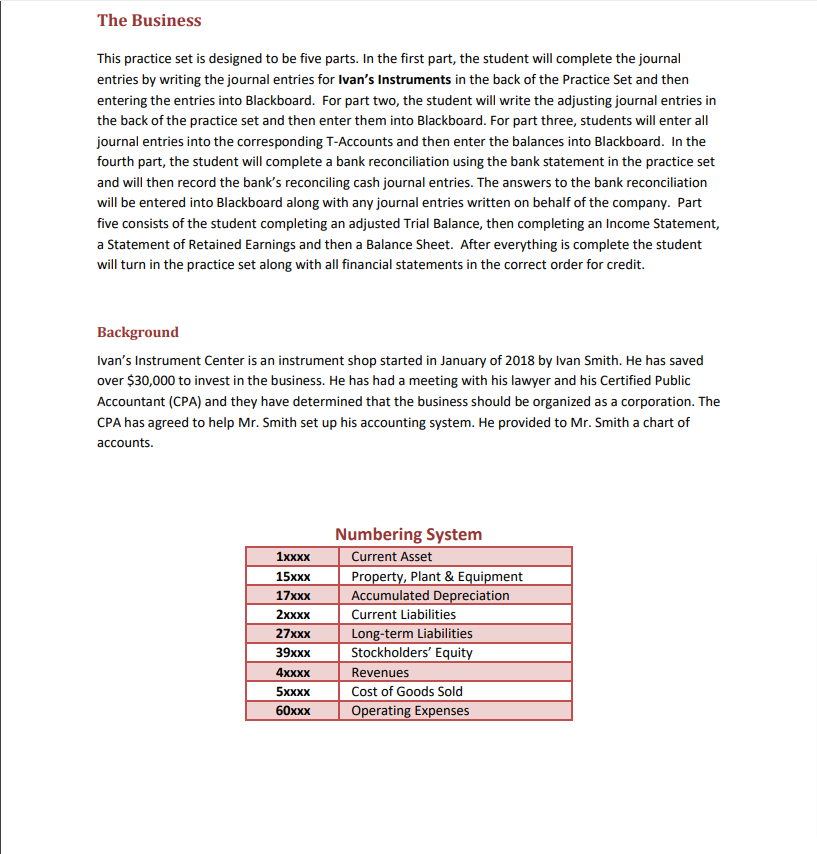

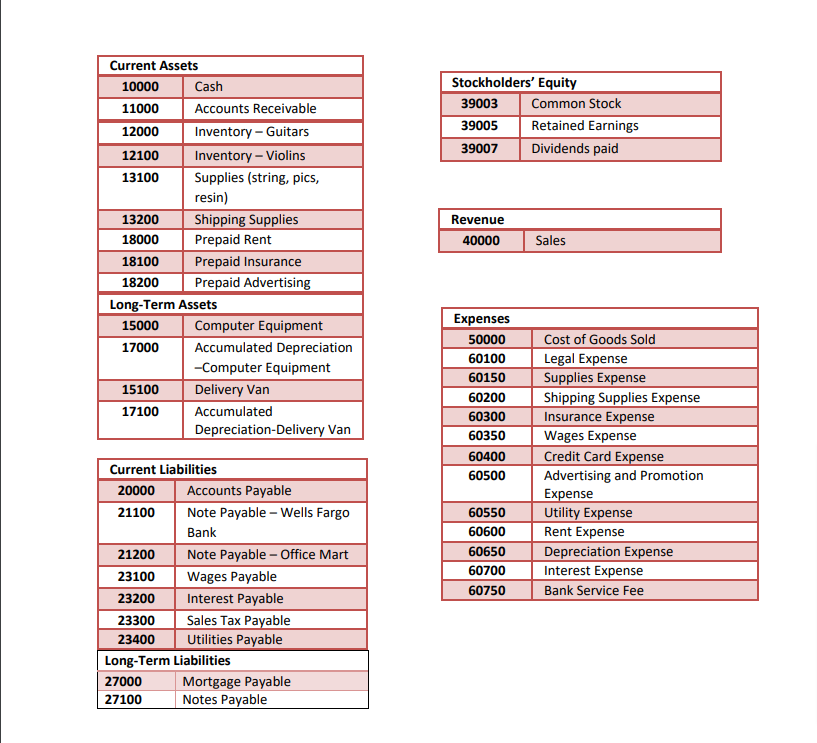

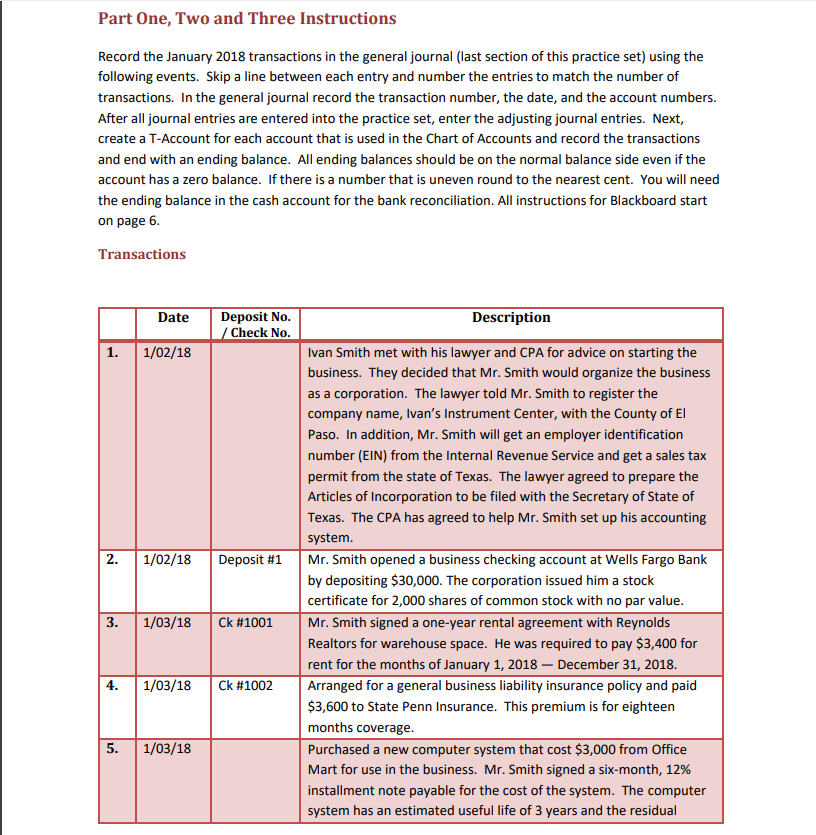

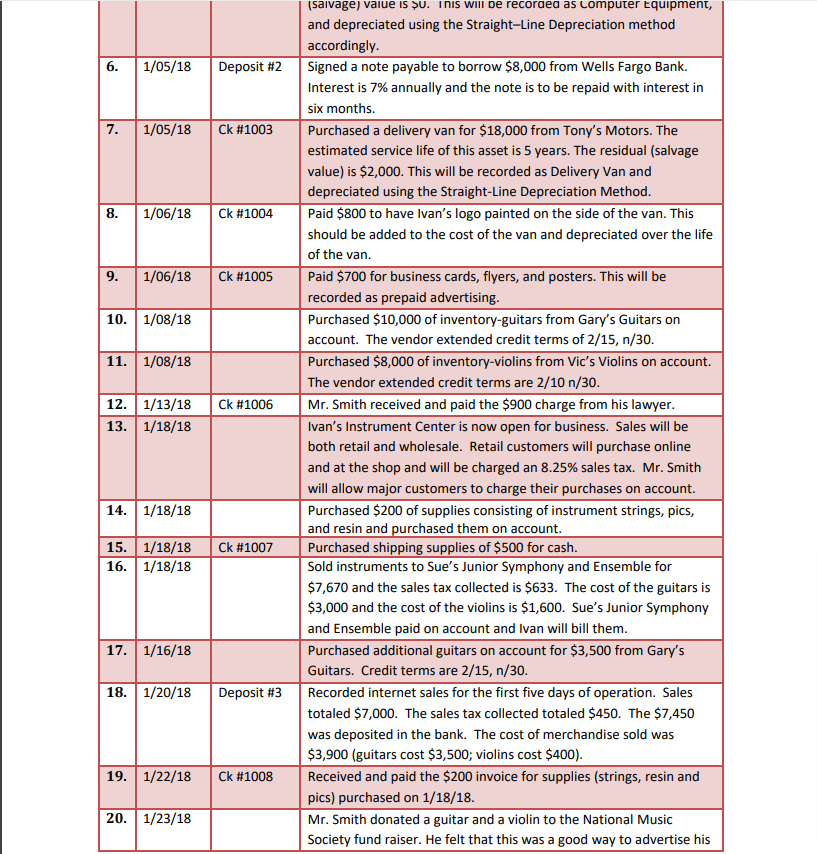

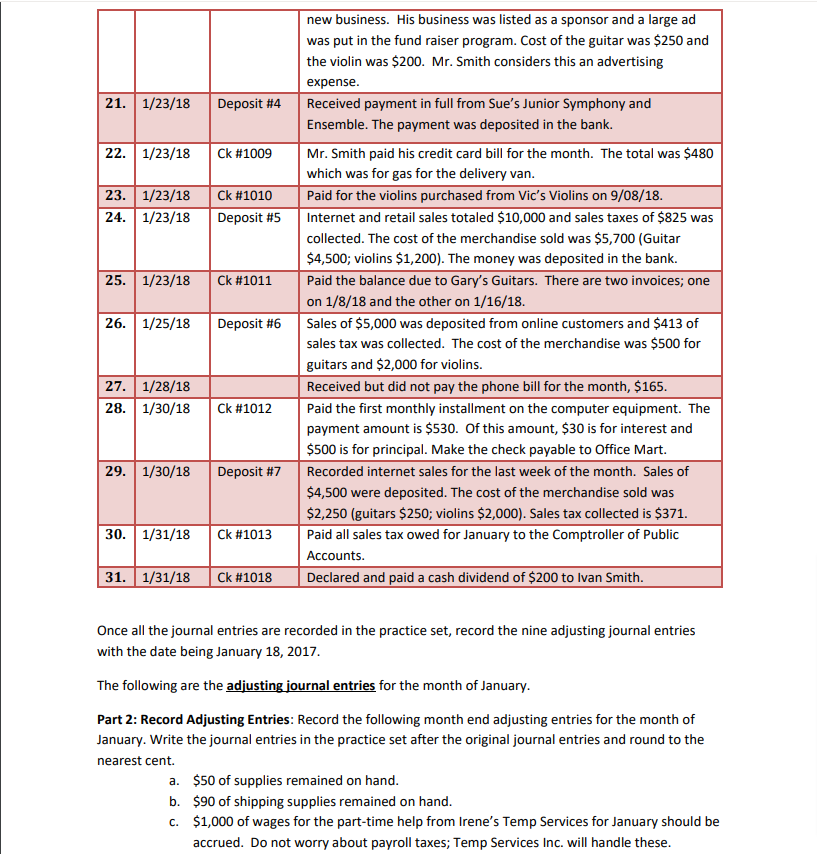

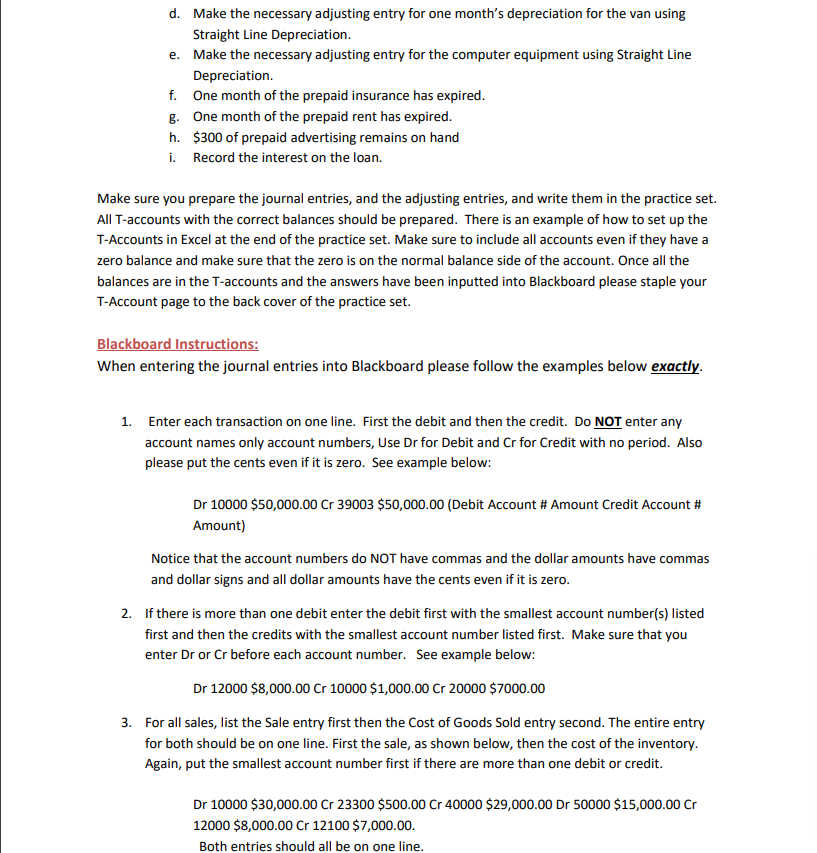

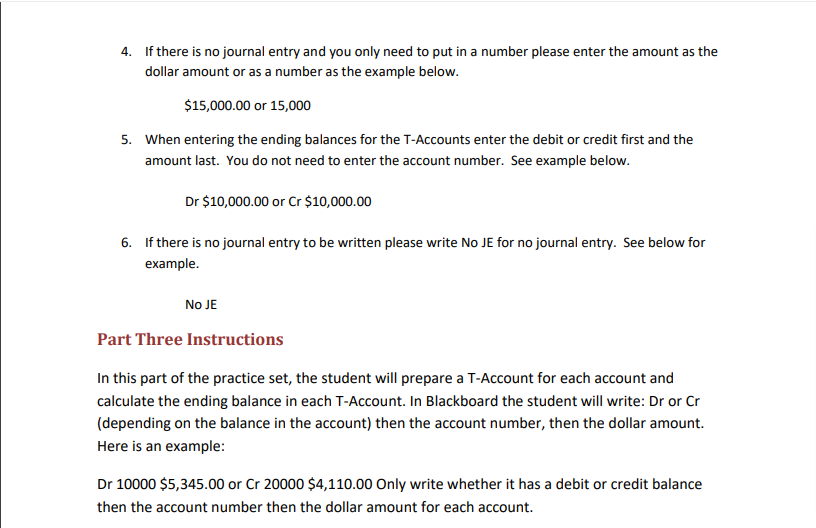

The Business This practice set is designed to be five parts. In the first part, the student will complete the journal entries by writing the journal entries for Ivan's Instruments in the back of the Practice Set and then entering the entries into Blackboard. For part two, the student will write the adjusting journal entries in the back of the practice set and then enter them into Blackboard. For part three, students will enter all journal entries into the corresponding T-Accounts and then enter the balances into Blackboard. In the fourth part, the student will complete a bank reconciliation using the bank statement in the practice set and will then record the bank's reconciling cash journal entries. The answers to the bank reconciliation will be entered into Blackboard along with any journal entries written on behalf of the company. Part five consists of the student completing an adjusted Trial Balance, then completing an Income Statement, a Statement of Retained Earnings and then a Balance Sheet. After everything is complete the student will turn in the practice set along with all financial statements in the correct order for credit. Background Ivan's Instrument Center is an instrument shop started in January of 2018 by Ivan Smith. He has saved over $30,000 to invest in the business. He has had a meeting with his lawyer and his Certified Public Accountant (CPA) and they have determined that the business should be organized as a corporation. The CPA has agreed to help Mr. Smith set up his accounting system. He provided to Mr. Smith a chart of accounts. 1xxxx 15xxx 17xxx 2xxxx 27xxx 39xxx 4xxxx 5xxxx 60xxx Numbering System Current Asset Property, Plant & Equipment Accumulated Depreciation Current Liabilities Long-term Liabilities Stockholders' Equity Revenues Cost of Goods Sold Operating Expenses Current Assets 10000 11000 12000 12100 13100 13200 18000 18100 18200 Long-Term Assets 15000 17000 15100 17100 21200 23100 23200 Cash Accounts Receivable Inventory - Guitars Inventory - Violins Supplies (string, pics, resin) 23300 23400 Shipping Supplies Prepaid Rent Prepaid Insurance Prepaid Advertising Current Liabilities 20000 Accounts Payable 21100 27000 27100 Computer Equipment Accumulated Depreciation -Computer Equipment Delivery Van Accumulated Depreciation-Delivery Van Note Payable - Wells Fargo Bank Note Payable - Office Mart Wages Payable Interest Payable Sales Tax Payable Utilities Payable Long-Term Liabilities Mortgage Payable Notes Payable Stockholders' Equity 39003 39005 39007 Revenue 40000 Expenses 50000 60100 60150 60200 60300 60350 60400 60500 60550 60600 60650 60700 60750 Common Stock Retained Earnings Dividends paid Sales Cost of Goods Sold Legal Expense Supplies Expense Shipping Supplies Expense Insurance Expense Wages Expense Credit Card Expense Advertising and Promotion Expense Utility Expense Rent Expense Depreciation Expense Interest Expense Bank Service Fee Part One, Two and Three Instructions Record the January 2018 transactions in the general journal (last section of this practice set) using the following events. Skip a line between each entry and number the entries to match the number of transactions. In the general journal record the transaction number, the date, and the account numbers. After all journal entries are entered into the practice set, enter the adjusting journal entries. Next, create a T-Account for each account that is used in the Chart of Accounts and record the transactions and end with an ending balance. All ending balances should be on the normal balance side even if the account has a zero balance. If there is a number that is uneven round to the nearest cent. You will need the ending balance in the cash account for the bank reconciliation. All instructions for Blackboard start on page 6. Transactions 1. 2. 3. Date 1/02/18 5. Deposit No. / Check No. 1/02/18 Deposit #1 1/03/18 Ck #1001 4. 1/03/18 Ck #1002 1/03/18 Description Ivan Smith met with his lawyer and CPA for advice on starting the business. They decided that Mr. Smith would organize the business as a corporation. The lawyer told Mr. Smith to register the company name, Ivan's Instrument Center, with the County of El Paso. In addition, Mr. Smith will get an employer identification number (EIN) from the Internal Revenue Service and get a sales tax permit from the state of Texas. The lawyer agreed to prepare the Articles of Incorporation to be filed with the Secretary of State of Texas. The CPA has agreed to help Mr. Smith set up his accounting system. Mr. Smith opened a business checking account at Wells Fargo Bank by depositing $30,000. The corporation issued him a stock certificate for 2,000 shares of common stock with no par value. Mr. Smith signed a one-year rental agreement with Reynolds Realtors for warehouse space. He was required to pay $3,400 for rent for the months of January 1, 2018 December 31, 2018. Arranged for a general business liability insurance policy and paid $3,600 to State Penn Insurance. This premium is for eighteen months coverage. Purchased a new computer system that cost $3,000 from Office Mart for use in the business. Mr. Smith signed a six-month, 12% installment note payable for the cost of the system. The computer system has an estimated useful life of 3 years and the residual 6. 7. 8. 1/05/18 1/05/18 1/06/18 Ck #1004 10. 1/08/18 9. 1/06/18 Ck #1005 11. 1/08/18 12. 1/13/18 13. 1/18/18 14. 1/18/18 Deposit #2 17. 1/16/18 Ck #1003 18. 1/20/18 15. 1/18/18 Ck #1007 16. 1/18/18 20. 1/23/18 Ck #1006 Deposit #3 19. 1/22/18 Ck #1008 (salvage) value is u. This will be recorded as Computer Equipment, and depreciated using the Straight-Line Depreciation method accordingly. Signed a note payable to borrow $8,000 from Wells Fargo Bank. Interest is 7% annually and the note is to be repaid with interest in six months. Purchased a delivery van for $18,000 from Tony's Motors. The estimated service life of this asset is 5 years. The residual (salvage value) is $2,000. This will be recorded as Delivery Van and depreciated using the Straight-Line Depreciation Method. Paid $800 to have Ivan's logo painted on the side of the van. This should be added to the cost of the van and depreciated over the life of the van. Paid $700 for business cards, flyers, and posters. This will be recorded as prepaid advertising. Purchased $10,000 of inventory-guitars from Gary's Guitars on account. The vendor extended credit terms of 2/15, n/30. Purchased $8,000 of inventory-violins from Vic's Violins on account. The vendor extended credit terms are 2/10 n/30. Mr. Smith received and paid the $900 charge from his lawyer. Ivan's Instrument Center is now open for business. Sales will be both retail and wholesale. Retail customers will purchase online and at the shop and will be charged an 8.25% sales tax. Mr. Smith will allow major customers to charge their purchases on account. Purchased $200 of supplies consisting of instrument strings, pics, and resin and purchased them on account. Purchased shipping supplies of $500 for cash. Sold instruments to Sue's Junior Symphony and Ensemble for $7,670 and the sales tax collected is $633. The cost of the guitars is $3,000 and the cost of the violins is $1,600. Sue's Junior Symphony and Ensemble paid on account and Ivan will bill them. Purchased additional guitars on account for $3,500 from Gary's Guitars. Credit terms are 2/15, n/30. Recorded internet sales for the first five days of operation. Sales totaled $7,000. The sales tax collected totaled $450. The $7,450 was deposited in the bank. The cost of merchandise sold was $3,900 (guitars cost $3,500; violins cost $400). Received and paid the $200 invoice for supplies (strings, resin and pics) purchased on 1/18/18. Mr. Smith donated a guitar and a violin to the National Music Society fund raiser. He felt that this was a good way to advertise his 21. 1/23/18 Deposit #4 22. 1/23/18 23. 1/23/18 24. 1/23/18 Ck #1009 Ck #1010 Deposit #5 25. 1/23/18 Ck #1011 26. 1/25/18 Deposit #6 27. 1/28/18 28. 1/30/18 Ck #1012 29. 1/30/18 Deposit #7 30. 1/31/18 Ck #1013 31. 1/31/18 Ck #1018 new business. His business was listed as a sponsor and a large ad was put in the fund raiser program. Cost of the guitar was $250 and the violin was $200. Mr. Smith considers this an advertising expense. Received payment in full from Sue's Junior Symphony and Ensemble. The payment was deposited in the bank. Mr. Smith paid his credit card bill for the month. The total was $480 which was for gas for the delivery van. Paid for the violins purchased from Vic's Violins on 9/08/18. Internet and retail sales totaled $10,000 and sales taxes of $825 was collected. The cost of the merchandise sold was $5,700 (Guitar $4,500; violins $1,200). The money was deposited in the bank. Paid the balance due to Gary's Guitars. There are two invoices; one on 1/8/18 and the other on 1/16/18. Sales of $5,000 was deposited from online customers and $413 of sales tax was collected. The cost of the merchandise was $500 for guitars and $2,000 for violins. Received but did not pay the phone bill for the month, $165. Paid the first monthly installment on the computer equipment. The payment amount is $530. Of this amount, $30 is for interest and $500 is for principal. Make the check payable to Office Mart. Recorded internet sales for the last week of the month. Sales of $4,500 were deposited. The cost of the merchandise sold was $2,250 (guitars $250; violins $2,000). Sales tax collected is $371. Paid all sales tax owed for January to the Comptroller of Public Accounts. Declared and paid a cash dividend of $200 to Ivan Smith. Once all the journal entries are recorded in the practice set, record the nine adjusting journal entries with the date being January 18, 2017. The following are the adjusting journal entries for the month of January. Part 2: Record Adjusting Entries: Record the following month end adjusting entries for the month of January. Write the journal entries in the practice set after the original journal entries and round to the nearest cent. a. $50 of supplies remained on hand. b. $90 of shipping supplies remained on hand. c. $1,000 of wages for the part-time help from Irene's Temp Services for January should be accrued. Do not worry about payroll taxes; Temp Services Inc. will handle these. d. Make the necessary adjusting entry for one month's depreciation for the van using Straight Line Depreciation. e. Make the necessary adjusting entry for the computer equipment using Straight Line Depreciation. f. One month of the prepaid insurance has expired. g. One month of the prepaid rent has expired. h. $300 of prepaid advertising remains on hand i. Record the interest on the loan. Make sure you prepare the journal entries, and the adjusting entries, and write them in the practice set. All T-accounts with the correct balances should be prepared. There is an example of how to set up the T-Accounts in Excel at the end of the practice set. Make sure to include all accounts even if they have a zero balance and make sure that the zero is on the normal balance side of the account. Once all the balances are in the T-accounts and the answers have been inputted into Blackboard please staple your T-Account page to the back cover of the practice set. Blackboard Instructions: When entering the journal entries into Blackboard please follow the examples below exactly. 1. Enter each transaction on one line. First the debit and then the credit. Do NOT enter any account names only account numbers, Use Dr for Debit and Cr for Credit with no period. Also please put the cents even if it is zero. See example below: Dr 10000 $50,000.00 Cr 39003 $50,000.00 (Debit Account # Amount Credit Account # Amount) Notice that the account numbers do NOT have commas and the dollar amounts have commas and dollar signs and all dollar amounts have the cents even if it is zero. 2. If there is more than one debit enter the debit first with the smallest account number(s) listed first and then the credits with the smallest account number listed first. Make sure that you enter Dr or Cr before each account number. See example below: Dr 12000 $8,000.00 Cr 10000 $1,000.00 Cr 20000 $7000.00 3. For all sales, list the Sale entry first then the Cost of Goods Sold entry second. The entire entry for both should be on one line. First the sale, as shown below, then the cost of the inventory. Again, put the smallest account number first if there are more than one debit or credit. Dr 10000 $30,000.00 Cr 23300 $500.00 Cr 40000 $29,000.00 Dr 50000 $15,000.00 Cr 12000 $8,000.00 Cr 12100 $7,000.00. Both entries should all be on one line. 4. If there is no journal entry and you only need to put in a number please enter the amount as the dollar amount or as a number as the example below. $15,000.00 or 15,000 5. When entering the ending balances for the T-Accounts enter the debit or credit first and the amount last. You do not need to enter the account number. See example below. Dr $10,000.00 or Cr $10,000.00 6. If there is no journal entry to be written please write No JE for no journal entry. See below for example. NO JE Part Three Instructions In this part of the practice set, the student will prepare a T-Account for each account and calculate the ending balance in each T-Account. In Blackboard the student will write: Dr or Cr (depending on the balance in the account) then the account number, then the dollar amount. Here is an example: Dr 10000 $5,345.00 or Cr 20000 $4,110.00 Only write whether it has a debit or credit balance then the account number then the dollar amount for each account. The Business This practice set is designed to be five parts. In the first part, the student will complete the journal entries by writing the journal entries for Ivan's Instruments in the back of the Practice Set and then entering the entries into Blackboard. For part two, the student will write the adjusting journal entries in the back of the practice set and then enter them into Blackboard. For part three, students will enter all journal entries into the corresponding T-Accounts and then enter the balances into Blackboard. In the fourth part, the student will complete a bank reconciliation using the bank statement in the practice set and will then record the bank's reconciling cash journal entries. The answers to the bank reconciliation will be entered into Blackboard along with any journal entries written on behalf of the company. Part five consists of the student completing an adjusted Trial Balance, then completing an Income Statement, a Statement of Retained Earnings and then a Balance Sheet. After everything is complete the student will turn in the practice set along with all financial statements in the correct order for credit. Background Ivan's Instrument Center is an instrument shop started in January of 2018 by Ivan Smith. He has saved over $30,000 to invest in the business. He has had a meeting with his lawyer and his Certified Public Accountant (CPA) and they have determined that the business should be organized as a corporation. The CPA has agreed to help Mr. Smith set up his accounting system. He provided to Mr. Smith a chart of accounts. 1xxxx 15xxx 17xxx 2xxxx 27xxx 39xxx 4xxxx 5xxxx 60xxx Numbering System Current Asset Property, Plant & Equipment Accumulated Depreciation Current Liabilities Long-term Liabilities Stockholders' Equity Revenues Cost of Goods Sold Operating Expenses Current Assets 10000 11000 12000 12100 13100 13200 18000 18100 18200 Long-Term Assets 15000 17000 15100 17100 21200 23100 23200 Cash Accounts Receivable Inventory - Guitars Inventory - Violins Supplies (string, pics, resin) 23300 23400 Shipping Supplies Prepaid Rent Prepaid Insurance Prepaid Advertising Current Liabilities 20000 Accounts Payable 21100 27000 27100 Computer Equipment Accumulated Depreciation -Computer Equipment Delivery Van Accumulated Depreciation-Delivery Van Note Payable - Wells Fargo Bank Note Payable - Office Mart Wages Payable Interest Payable Sales Tax Payable Utilities Payable Long-Term Liabilities Mortgage Payable Notes Payable Stockholders' Equity 39003 39005 39007 Revenue 40000 Expenses 50000 60100 60150 60200 60300 60350 60400 60500 60550 60600 60650 60700 60750 Common Stock Retained Earnings Dividends paid Sales Cost of Goods Sold Legal Expense Supplies Expense Shipping Supplies Expense Insurance Expense Wages Expense Credit Card Expense Advertising and Promotion Expense Utility Expense Rent Expense Depreciation Expense Interest Expense Bank Service Fee Part One, Two and Three Instructions Record the January 2018 transactions in the general journal (last section of this practice set) using the following events. Skip a line between each entry and number the entries to match the number of transactions. In the general journal record the transaction number, the date, and the account numbers. After all journal entries are entered into the practice set, enter the adjusting journal entries. Next, create a T-Account for each account that is used in the Chart of Accounts and record the transactions and end with an ending balance. All ending balances should be on the normal balance side even if the account has a zero balance. If there is a number that is uneven round to the nearest cent. You will need the ending balance in the cash account for the bank reconciliation. All instructions for Blackboard start on page 6. Transactions 1. 2. 3. Date 1/02/18 5. Deposit No. / Check No. 1/02/18 Deposit #1 1/03/18 Ck #1001 4. 1/03/18 Ck #1002 1/03/18 Description Ivan Smith met with his lawyer and CPA for advice on starting the business. They decided that Mr. Smith would organize the business as a corporation. The lawyer told Mr. Smith to register the company name, Ivan's Instrument Center, with the County of El Paso. In addition, Mr. Smith will get an employer identification number (EIN) from the Internal Revenue Service and get a sales tax permit from the state of Texas. The lawyer agreed to prepare the Articles of Incorporation to be filed with the Secretary of State of Texas. The CPA has agreed to help Mr. Smith set up his accounting system. Mr. Smith opened a business checking account at Wells Fargo Bank by depositing $30,000. The corporation issued him a stock certificate for 2,000 shares of common stock with no par value. Mr. Smith signed a one-year rental agreement with Reynolds Realtors for warehouse space. He was required to pay $3,400 for rent for the months of January 1, 2018 December 31, 2018. Arranged for a general business liability insurance policy and paid $3,600 to State Penn Insurance. This premium is for eighteen months coverage. Purchased a new computer system that cost $3,000 from Office Mart for use in the business. Mr. Smith signed a six-month, 12% installment note payable for the cost of the system. The computer system has an estimated useful life of 3 years and the residual 6. 7. 8. 1/05/18 1/05/18 1/06/18 Ck #1004 10. 1/08/18 9. 1/06/18 Ck #1005 11. 1/08/18 12. 1/13/18 13. 1/18/18 14. 1/18/18 Deposit #2 17. 1/16/18 Ck #1003 18. 1/20/18 15. 1/18/18 Ck #1007 16. 1/18/18 20. 1/23/18 Ck #1006 Deposit #3 19. 1/22/18 Ck #1008 (salvage) value is u. This will be recorded as Computer Equipment, and depreciated using the Straight-Line Depreciation method accordingly. Signed a note payable to borrow $8,000 from Wells Fargo Bank. Interest is 7% annually and the note is to be repaid with interest in six months. Purchased a delivery van for $18,000 from Tony's Motors. The estimated service life of this asset is 5 years. The residual (salvage value) is $2,000. This will be recorded as Delivery Van and depreciated using the Straight-Line Depreciation Method. Paid $800 to have Ivan's logo painted on the side of the van. This should be added to the cost of the van and depreciated over the life of the van. Paid $700 for business cards, flyers, and posters. This will be recorded as prepaid advertising. Purchased $10,000 of inventory-guitars from Gary's Guitars on account. The vendor extended credit terms of 2/15, n/30. Purchased $8,000 of inventory-violins from Vic's Violins on account. The vendor extended credit terms are 2/10 n/30. Mr. Smith received and paid the $900 charge from his lawyer. Ivan's Instrument Center is now open for business. Sales will be both retail and wholesale. Retail customers will purchase online and at the shop and will be charged an 8.25% sales tax. Mr. Smith will allow major customers to charge their purchases on account. Purchased $200 of supplies consisting of instrument strings, pics, and resin and purchased them on account. Purchased shipping supplies of $500 for cash. Sold instruments to Sue's Junior Symphony and Ensemble for $7,670 and the sales tax collected is $633. The cost of the guitars is $3,000 and the cost of the violins is $1,600. Sue's Junior Symphony and Ensemble paid on account and Ivan will bill them. Purchased additional guitars on account for $3,500 from Gary's Guitars. Credit terms are 2/15, n/30. Recorded internet sales for the first five days of operation. Sales totaled $7,000. The sales tax collected totaled $450. The $7,450 was deposited in the bank. The cost of merchandise sold was $3,900 (guitars cost $3,500; violins cost $400). Received and paid the $200 invoice for supplies (strings, resin and pics) purchased on 1/18/18. Mr. Smith donated a guitar and a violin to the National Music Society fund raiser. He felt that this was a good way to advertise his 21. 1/23/18 Deposit #4 22. 1/23/18 23. 1/23/18 24. 1/23/18 Ck #1009 Ck #1010 Deposit #5 25. 1/23/18 Ck #1011 26. 1/25/18 Deposit #6 27. 1/28/18 28. 1/30/18 Ck #1012 29. 1/30/18 Deposit #7 30. 1/31/18 Ck #1013 31. 1/31/18 Ck #1018 new business. His business was listed as a sponsor and a large ad was put in the fund raiser program. Cost of the guitar was $250 and the violin was $200. Mr. Smith considers this an advertising expense. Received payment in full from Sue's Junior Symphony and Ensemble. The payment was deposited in the bank. Mr. Smith paid his credit card bill for the month. The total was $480 which was for gas for the delivery van. Paid for the violins purchased from Vic's Violins on 9/08/18. Internet and retail sales totaled $10,000 and sales taxes of $825 was collected. The cost of the merchandise sold was $5,700 (Guitar $4,500; violins $1,200). The money was deposited in the bank. Paid the balance due to Gary's Guitars. There are two invoices; one on 1/8/18 and the other on 1/16/18. Sales of $5,000 was deposited from online customers and $413 of sales tax was collected. The cost of the merchandise was $500 for guitars and $2,000 for violins. Received but did not pay the phone bill for the month, $165. Paid the first monthly installment on the computer equipment. The payment amount is $530. Of this amount, $30 is for interest and $500 is for principal. Make the check payable to Office Mart. Recorded internet sales for the last week of the month. Sales of $4,500 were deposited. The cost of the merchandise sold was $2,250 (guitars $250; violins $2,000). Sales tax collected is $371. Paid all sales tax owed for January to the Comptroller of Public Accounts. Declared and paid a cash dividend of $200 to Ivan Smith. Once all the journal entries are recorded in the practice set, record the nine adjusting journal entries with the date being January 18, 2017. The following are the adjusting journal entries for the month of January. Part 2: Record Adjusting Entries: Record the following month end adjusting entries for the month of January. Write the journal entries in the practice set after the original journal entries and round to the nearest cent. a. $50 of supplies remained on hand. b. $90 of shipping supplies remained on hand. c. $1,000 of wages for the part-time help from Irene's Temp Services for January should be accrued. Do not worry about payroll taxes; Temp Services Inc. will handle these. d. Make the necessary adjusting entry for one month's depreciation for the van using Straight Line Depreciation. e. Make the necessary adjusting entry for the computer equipment using Straight Line Depreciation. f. One month of the prepaid insurance has expired. g. One month of the prepaid rent has expired. h. $300 of prepaid advertising remains on hand i. Record the interest on the loan. Make sure you prepare the journal entries, and the adjusting entries, and write them in the practice set. All T-accounts with the correct balances should be prepared. There is an example of how to set up the T-Accounts in Excel at the end of the practice set. Make sure to include all accounts even if they have a zero balance and make sure that the zero is on the normal balance side of the account. Once all the balances are in the T-accounts and the answers have been inputted into Blackboard please staple your T-Account page to the back cover of the practice set. Blackboard Instructions: When entering the journal entries into Blackboard please follow the examples below exactly. 1. Enter each transaction on one line. First the debit and then the credit. Do NOT enter any account names only account numbers, Use Dr for Debit and Cr for Credit with no period. Also please put the cents even if it is zero. See example below: Dr 10000 $50,000.00 Cr 39003 $50,000.00 (Debit Account # Amount Credit Account # Amount) Notice that the account numbers do NOT have commas and the dollar amounts have commas and dollar signs and all dollar amounts have the cents even if it is zero. 2. If there is more than one debit enter the debit first with the smallest account number(s) listed first and then the credits with the smallest account number listed first. Make sure that you enter Dr or Cr before each account number. See example below: Dr 12000 $8,000.00 Cr 10000 $1,000.00 Cr 20000 $7000.00 3. For all sales, list the Sale entry first then the Cost of Goods Sold entry second. The entire entry for both should be on one line. First the sale, as shown below, then the cost of the inventory. Again, put the smallest account number first if there are more than one debit or credit. Dr 10000 $30,000.00 Cr 23300 $500.00 Cr 40000 $29,000.00 Dr 50000 $15,000.00 Cr 12000 $8,000.00 Cr 12100 $7,000.00. Both entries should all be on one line. 4. If there is no journal entry and you only need to put in a number please enter the amount as the dollar amount or as a number as the example below. $15,000.00 or 15,000 5. When entering the ending balances for the T-Accounts enter the debit or credit first and the amount last. You do not need to enter the account number. See example below. Dr $10,000.00 or Cr $10,000.00 6. If there is no journal entry to be written please write No JE for no journal entry. See below for example. NO JE Part Three Instructions In this part of the practice set, the student will prepare a T-Account for each account and calculate the ending balance in each T-Account. In Blackboard the student will write: Dr or Cr (depending on the balance in the account) then the account number, then the dollar amount. Here is an example: Dr 10000 $5,345.00 or Cr 20000 $4,110.00 Only write whether it has a debit or credit balance then the account number then the dollar amount for each account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts