Question: Part Two: Revenue Sources, Structure, and Administration The township value data are for the area outside of any city or town that resides in

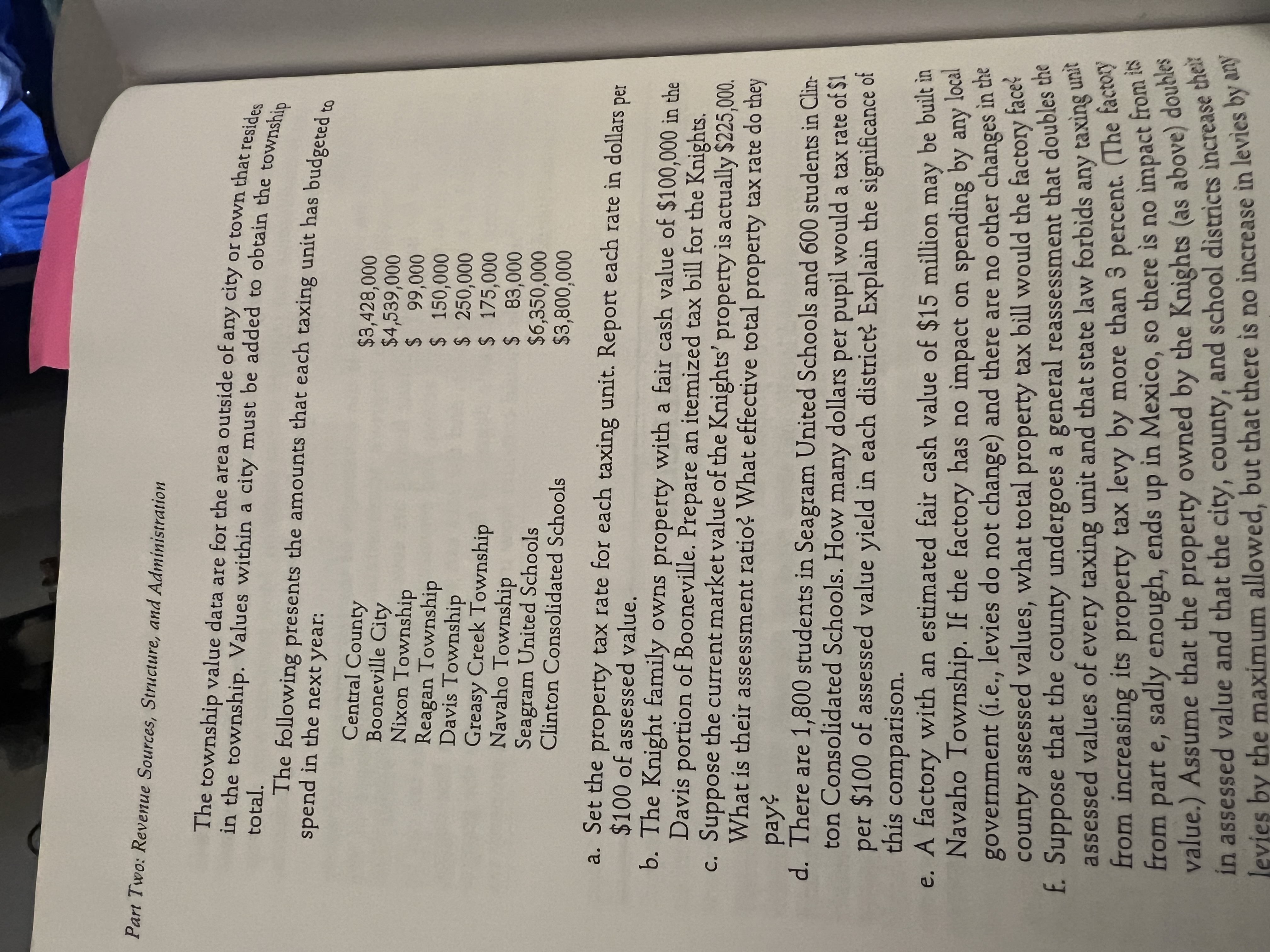

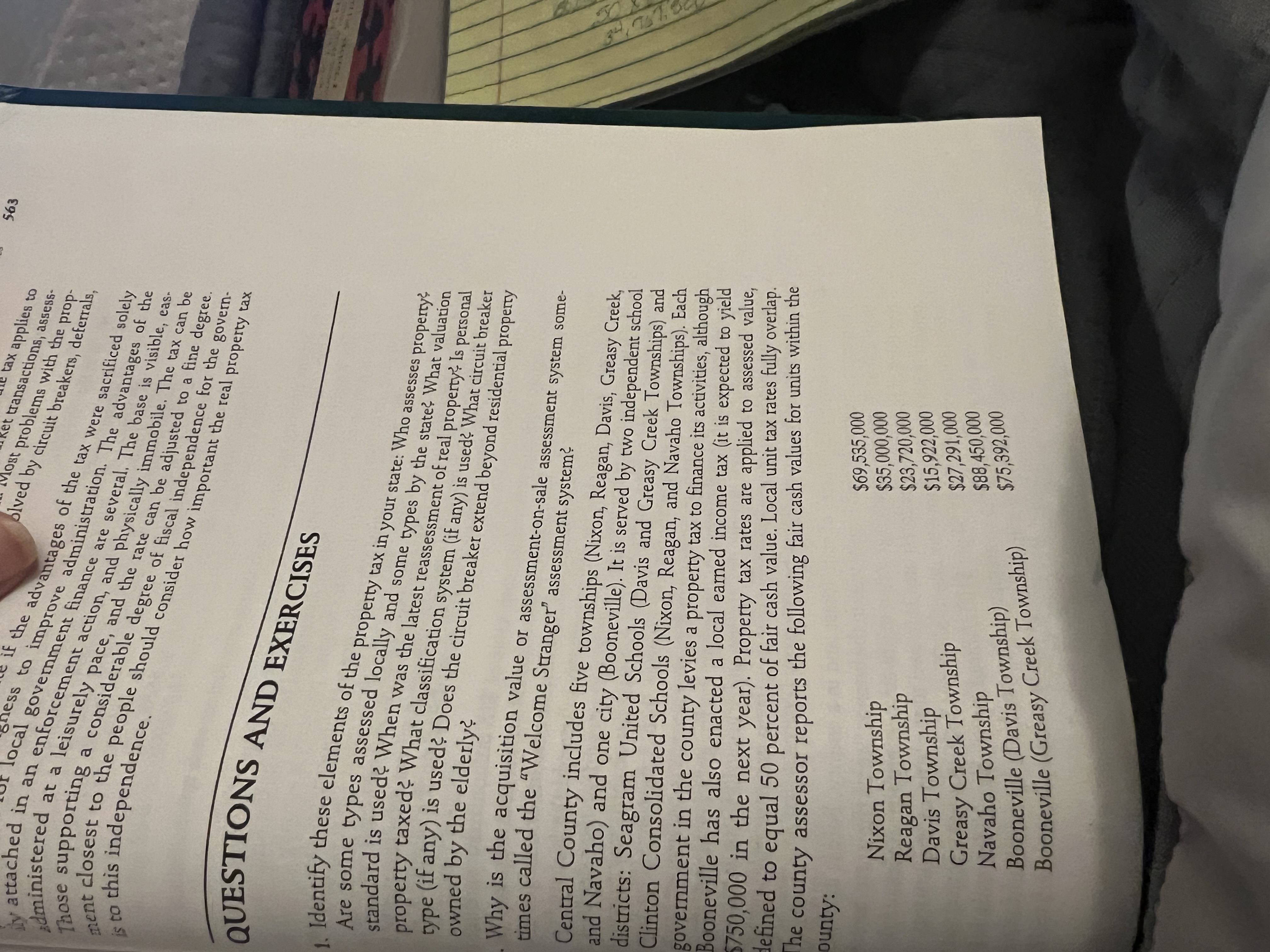

Part Two: Revenue Sources, Structure, and Administration The township value data are for the area outside of any city or town that resides in the township. Values within a city must be added to obtain the township total. spend in the next year: The following presents the amounts that each taxing unit has budgeted to Central County Booneville City Nixon Township Reagan Township Davis Township Greasy Creek Township Navaho Township Seagram United Schools Clinton Consolidated Schools $3,428,000 $4,539,000 $ 99,000 $ 150,000 $ 250,000 $ 175,000 $ 83,000 $6,350,000 $3,800,000 a. Set the property tax rate for each taxing unit. Report each rate in dollars $100 of assessed value. per b. The Knight family owns property with a fair cash value of $100,000 in the Davis portion of Booneville. Prepare an itemized tax bill for the Knights. c. Suppose the current market value of the Knights' property is actually $225,000. What is their assessment ratio? What effective total property tax rate do they pay? d. There are 1,800 students in Seagram United Schools and 600 students in Clin- ton Consolidated Schools. How many dollars per pupil would a tax rate of $1 per $100 of assessed value yield in each district? Explain the significance of this comparison. e. A factory with an estimated fair cash value of $15 million may be built in Navaho Township. If the factory has no impact on spending by any local government (i.e., levies do not change) and there are no other changes in the county assessed values, what total property tax bill would the factory face f. Suppose that the county undergoes a general reassessment that doubles the assessed values of every taxing unit and that state law forbids any taxing unit from increasing its property tax levy by more than 3 percent. (The factory from part e, sadly enough, ends up in Mexico, so there is no impact from its value.) Assume that the property owned by the Knights (as above) doubles in assessed value and that the city, county, and school districts increase levies by the maximum allowed, but that there is no increase in levies by any their 34, TT administered tax applies to Ret transactions, assess- Most problems with the prop- olved by circuit breakers, deferrals, if the advantages of the tax were sacrificed solely ghess to improve administration. The advantages of the TUF local government finance are several. The base is visible, eas- at a y attached in an enforcement action, and physically immobile. The tax can be leisurely pace, and the rate can be adjusted to a fine degree. Those supporting a considerable degree of fiscal independence for the govern- closest to the people should consider how important the real property tax is to this independence. QUESTIONS AND EXERCISES 1. 563 Are some types assessed locally and some types by the state? What valuation standard is used? When was the latest reassessment of real property? Is personal property taxed? What classification system (if any) is used? What circuit breaker type (if any) is used? Does the circuit breaker extend beyond residential property owned by the elderly? times called the "Welcome Stranger" assessment system? Why is the acquisition value or assessment-on-sale assessment system some- Central County includes five townships (Nixon, Reagan, Davis, Greasy Creek, and Navaho) and one city (Booneville). It is served by two independent school districts: Seagram United Schools (Davis and Greasy Creek Townships) and Clinton Consolidated Schools (Nixon, Reagan, and Navaho Townships). Each government in the county levies a property tax to finance its activities, although Booneville has also enacted a local earned income tax (it is expected to yield $750,000 in the next year). Property tax rates are applied to assessed value, defined to equal 50 percent of fair cash value. Local unit tax rates fully overlap. The county assessor reports the following fair cash values for units within the County: Nixon Township Reagan Township Davis Township $69,535,000 $35,000,000 $23,720,000 Greasy Creek Township $15,922,000 Navaho Township $27,291,000 Booneville (Davis Township) $88,450,000 Booneville (Greasy Creek Township) $75,392,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts