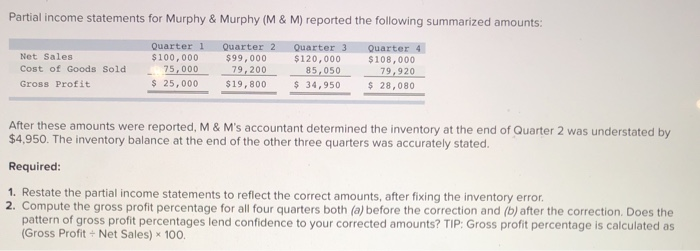

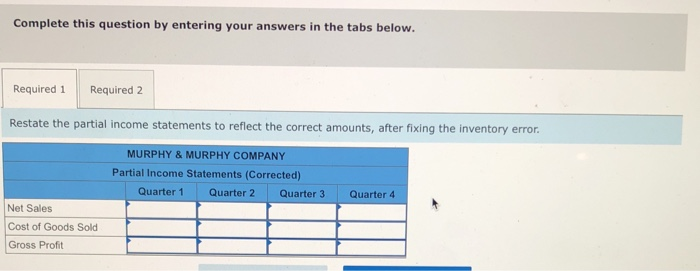

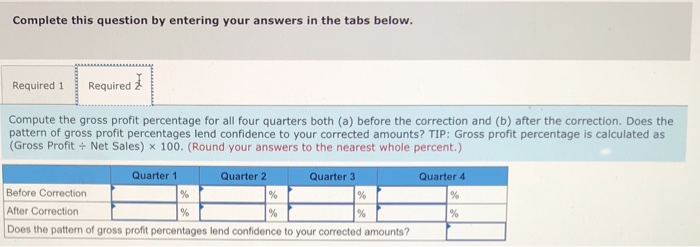

Question: Partial income statements for Murphy & Murphy (M& M) reported the following summarized amounts: Quarter 1 Quarter 2 Quarter 3 Quarter 4 $100,000 99,000 Net

Partial income statements for Murphy & Murphy (M& M) reported the following summarized amounts: Quarter 1 Quarter 2 Quarter 3 Quarter 4 $100,000 99,000 Net Sales Cost of Goods Sold Gross Profit $120,000 $108,000 79,920 $19,800 34,95028,080 $ 25,000 After these amounts were reported, M &M's accountant determined the inventory at the end of Quarter 2 was understated by $4,950. The inventory balance at the end of the other three quarters was accurately stated. Required 1. Restate the partial income statements to reflect the correct amounts, after fixing the inventory error 2. Compute the gross profit percentage for all four quarters both (a) before the correction and (b) after the correction. Does the pattern of gross profit percentages lend confidence to your corrected amounts? TIP: Gross profit percentage is calculated as (Gross Profit + Net Sales) x 100

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts