Question: Perform all calculations on the Excel spreadsheet form in the appropriate cells . A ssume the risk-free rate is .44% . Answer each question in

Perform all calculations on the Excel spreadsheet form in the appropriate cells. Assume the risk-free rate is .44%. Answer each question in your simulated role as financial managers -- in strategic, well-thought-out, complete sentences. Watch the Portfolio Theory videos in Blackboard for help with the calculations using Excel.

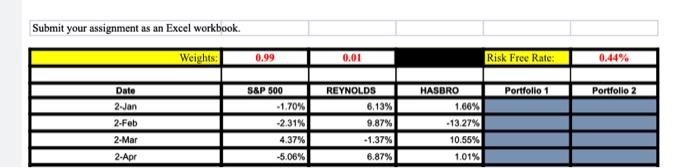

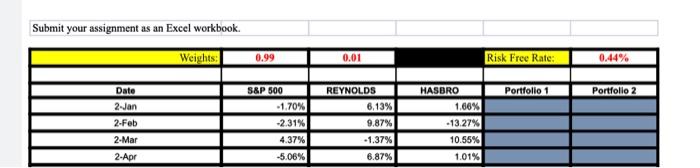

Submit your assignment as an Excel workbook. Weights: Date 2-Jan 2-Feb 2-Mar 2-Apr 0.99 S&P 500 -1.70% -2.31% 4.37% -5.06% 0.01 REYNOLDS 6.13% 9.87% -1.37% 6.87% HASBRO 1.66% -13.27% 10.55% 1.01% Risk Free Rate: Portfolio 1 0.44% Portfolio 2 Submit your assignment as an Excel workbook. Weights: Date 2-Jan 2-Feb 2-Mar 2-Apr 0.99 S&P 500 -1.70% -2.31% 4.37% -5.06% 0.01 REYNOLDS 6.13% 9.87% -1.37% 6.87% HASBRO 1.66% -13.27% 10.55% 1.01% Risk Free Rate: Portfolio 1 0.44% Portfolio 2 Submit your assignment as an Excel workbook. Weights: Date 2-Jan 2-Feb 2-Mar 2-Apr 0.99 S&P 500 -1.70% -2.31% 4.37% -5.06% 0.01 REYNOLDS 6.13% 9.87% -1.37% 6.87% HASBRO 1.66% -13.27% 10.55% 1.01% Risk Free Rate: Portfolio 1 0.44% Portfolio 2 Submit your assignment as an Excel workbook. Weights: Date 2-Jan 2-Feb 2-Mar 2-Apr 0.99 S&P 500 -1.70% -2.31% 4.37% -5.06% 0.01 REYNOLDS 6.13% 9.87% -1.37% 6.87% HASBRO 1.66% -13.27% 10.55% 1.01% Risk Free Rate: Portfolio 1 0.44% Portfolio 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts