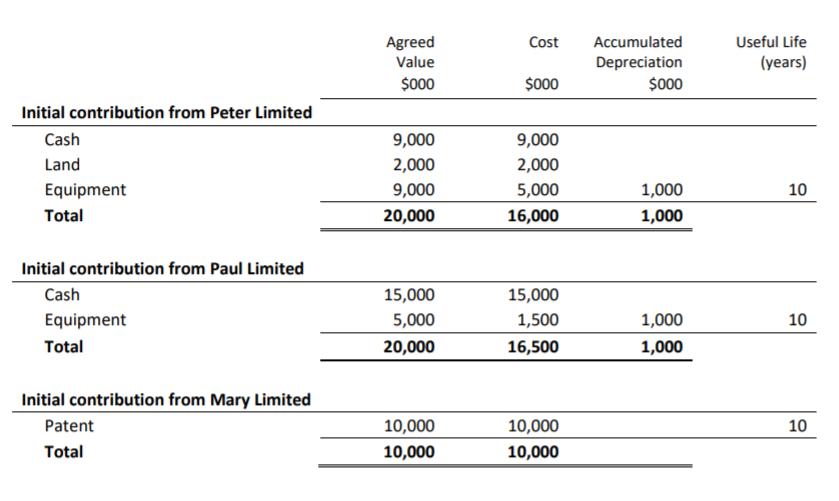

Peter Limited, Paul Limited and Mary Limited entered into a joint operation on 1 July 2019 to

Question:

The joint operators chose not to revalue their remaining interests in the contributed assets in their separate records. All joint operators agree to record any depreciation or amortisation of the joint operation in their own books. There are no residual values for the assets of the joint operation.

During the year ended 30 June 2020, Peter Limited, Paul Limited and Mary Limited contributed a further total of $10,000,000 cash to the joint operation in the same ratio as their initial interests.

Peter Limited was appointed Joint Operation Manager, receiving a sum of $500,000 for this service during the first year of operation. This service fee is included in the Administration costs reported in the Statement of Cash Receipts and Payments shown below.

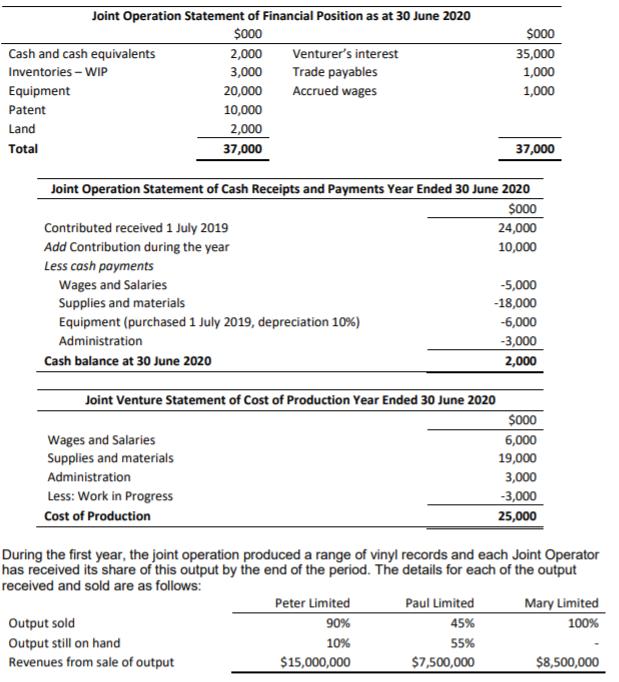

The financial statements for the joint operation for the year are as follows:

Required

1. Prepare the general journal entries for the year 1 July 2019 to 30 June 2020 for Peter Limited only in respect of the joint operation and related inventory transactions, assuming no entries have yet been made for the year ended 30 June 2020. Peter Limited uses the line-by-line method to account for its interest in the joint operation.

2. Based on the facts provided in Question 1, immediately after the initial contribution, what is the value of total Cash represented in the Interest in the Joint Operation held by Mary Limited?

3. Briefly discuss the principles you used in calculating your answer in Question 2.

Expert Answer:

1 General Journal Entries for Peter Limited a Initial Contribution on 1 July 2019 Debit Cash 20000000 Debit Land 2000000 Debit Equipment 9000000 Credi... View the full answer

Fundamentals of Cost Accounting

ISBN: 978-0077398194

3rd Edition

Authors: William Lanen, Shannon Anderson, Michael Maher