Question: Please also show the workings. Please highlight the correct answer Mathematical Question 3 (7 marks) Calculate the duration of a $1000 face value, 10% coupon

Please also show the workings.

Please highlight the correct answer

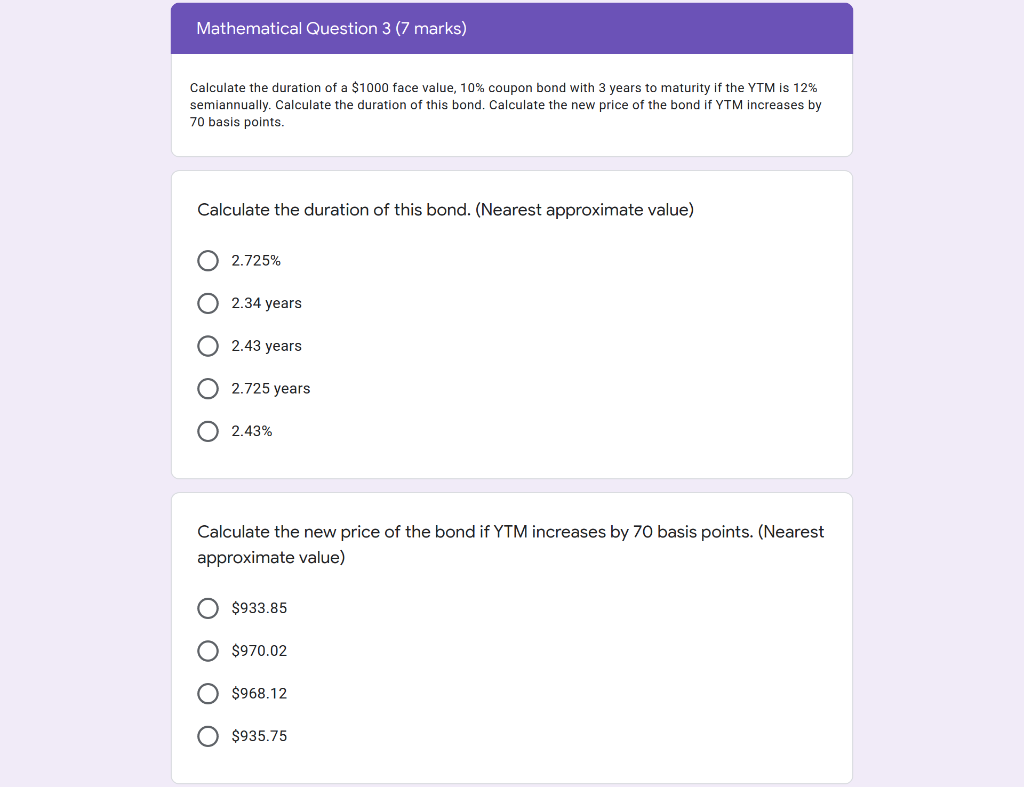

Mathematical Question 3 (7 marks) Calculate the duration of a $1000 face value, 10% coupon bond with 3 years to maturity if the YTM is 12% semiannually. Calculate the duration of this bond. Calculate the new price of the bond if YTM increases by 70 basis points. Calculate the duration of this bond. (Nearest approximate value) 2.725% 2.34 years 2.43 years O 2.725 years 2.43% Calculate the new price of the bond if YTM increases by 70 basis points. (Nearest approximate value) $933.85 $970.02 $968.12 O $935.75

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock