Question: please answer 2 a,b,c,d as they all correlate to the same question. I will leave excellent review 2. Suppose that the price S(t) of a

please answer 2 a,b,c,d as they all correlate to the same question. I will leave excellent review

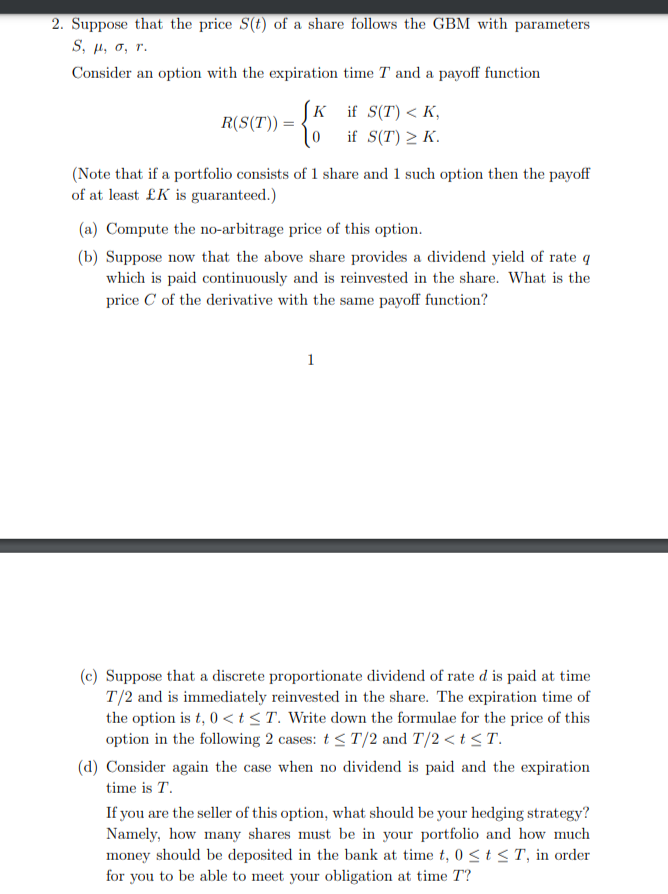

2. Suppose that the price S(t) of a share follows the GBM with parameters S, H, O, T. Consider an option with the expiration time T and a payoff function Kif S(T)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts