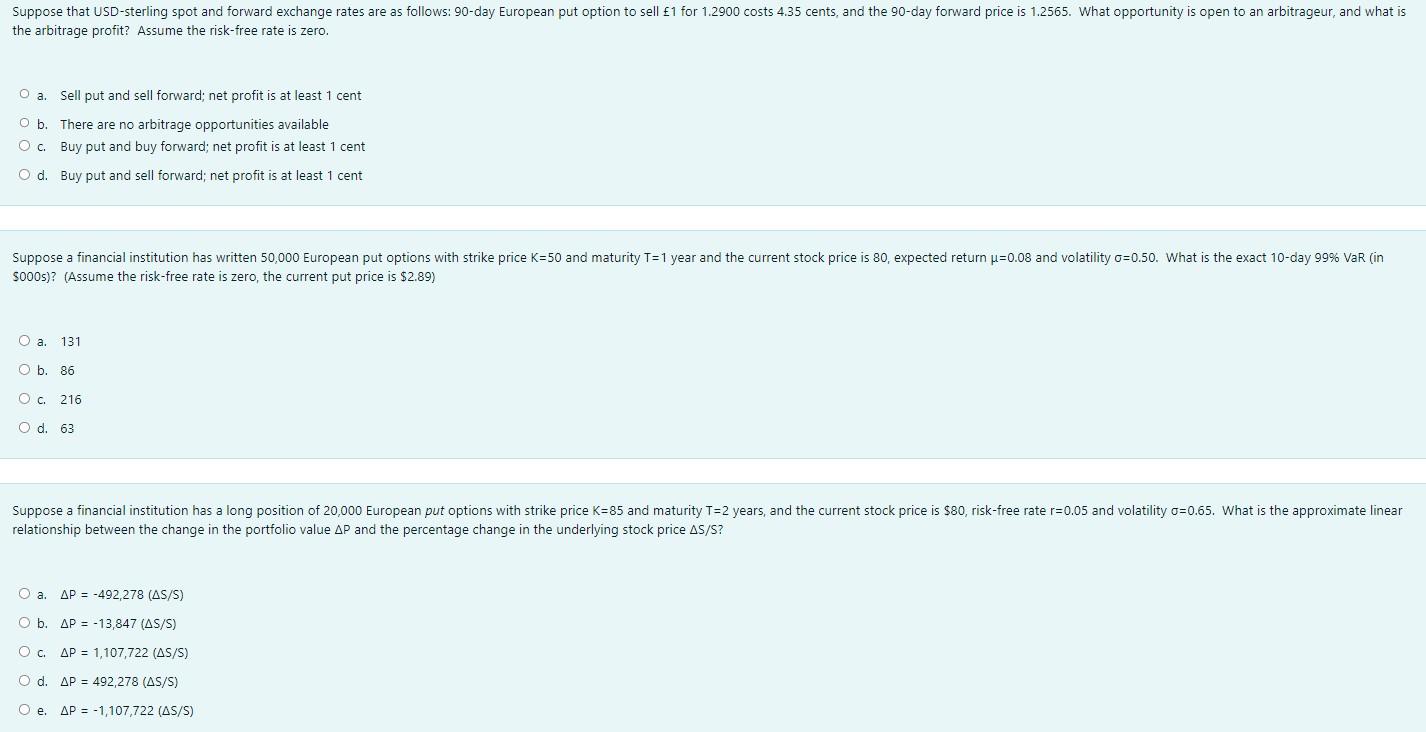

Question: Please answer all just need correct answer the arbitrage profit? Assume the risk-free rate is zero. a. Sell put and sell forward; net profit is

Please answer all just need correct answer

Please answer all just need correct answer

the arbitrage profit? Assume the risk-free rate is zero. a. Sell put and sell forward; net profit is at least 1 cent b. There are no arbitrage opportunities available c. Buy put and buy forward; net profit is at least 1 cent d. Buy put and sell forward; net profit is at least 1 cent \$000s)? (Assume the risk-free rate is zero, the current put price is $2.89 ) a. 131 b. 86 c. 216 d. 63 relationship between the change in the portfolio value P and the percentage change in the underlying stock price S/S ? a. P=492,278(S/S) b. P=13,847(S/S) c. P=1,107,722(S/S) d. P=492,278(S/S) e. P=1,107,722(S/S)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock