Question: please answer all parts if possible! there is 5 sections to this problem. these pictures are an example of this problem but I am having

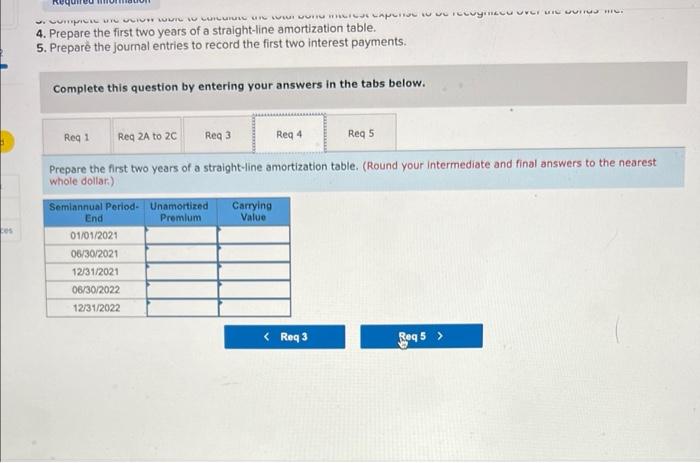

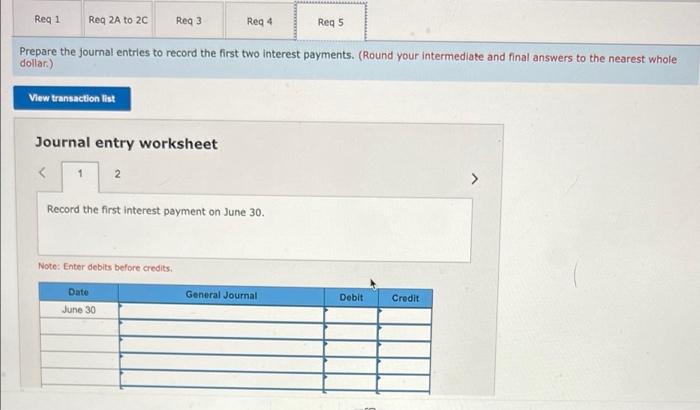

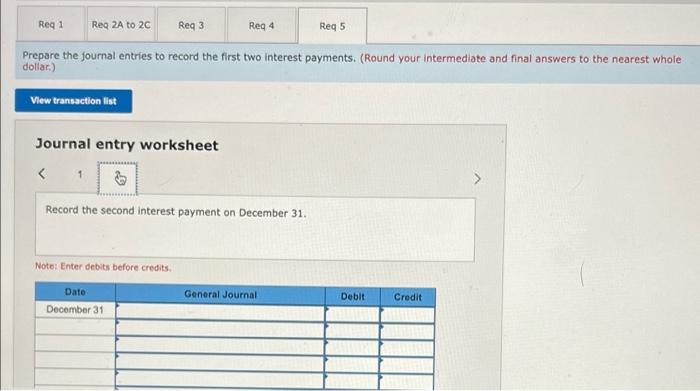

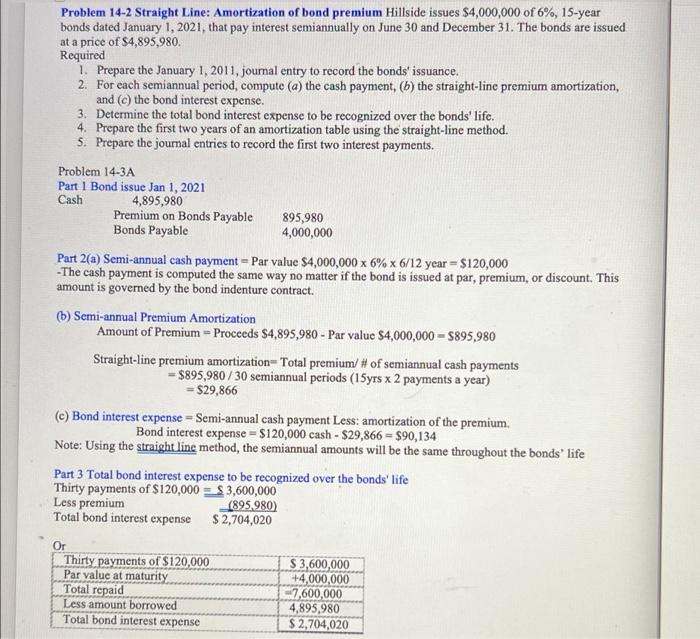

Required information Use the following information for the Problems below. (Algo) [The following information applles to the questions displayed below.) Hillside issues $1,500,000 of 6%, 15-year bonds dated January 1, 2021, that pay interest semiannually on June 30 and December 31 Problem 14-2A (Algo) Straight-Line: Amortization of bond premium LO P3 The bonds are issued at a price of $1,835,994. Required: 1. Prepare the January 1 journal entry to record the bonds' issuance. 2(a) For each semiannual period, complete the table below to calculate the cash payment. 216) For each semiannual period, complete the table below to calculate the straight-line premium amortization. 210 For each semiannual period, complete the table below to calculate the bond interest expense. 3. Complete the below table to calculate the total bond interest expense to be recognized over the bonds' life. 4. Prepare the first two years of a straight-line amortization table. 5. Prepare the journal entries to record the first two interest payments. Complete this question by entering your answers in the tabs below. Req 1 Reg 2A to 20 Reg 3 Reg 4 Req 5 Prepare the January 1 journal entry to record the bonds' Issuance. Req 1 Req 2A to 20 Req3 Req 4 Reg 5 Prepare the January 1 journal entry to record the bonds' Issuance. View transaction list Journal entry worksheet 1 Record the issue of bonds with a par value of $1,500,000 on January 1, 2021 at an issue price of $1,835,994. Note: Enter debits before credits. Date January 01 General Journal Debit Credit + Record entry Clear entry View general Journal Req Reg 2A to 20 Req3 Reg 4 Reg 5 For each semiannual period, compute (a) the cash payment, (b) the straight-line premium amortization, and (c) the bond Interest expense. (Round your final answers to the nearest whole dollar) Par (maturity value Annual Rate Year Semiannual cash Interest payment 2) Bond price Par (maturity value) Premium on Bonds Payable Semiannual periods 2/6) Straight-line premium mortization Semiannual cash payment Premium amortization Bond Interest expenso 2(0) 8 Required information 3. Complete the below table to calculate the total bond interest expense to be recognized over the bonds' life. 4. Prepare the first two years of a straight-line amortization table. 5. Prepare the journal entries to record the first two interest payments. Complete this question by entering your answers in the tabs below. Req1 Req ZA to 20 Req3 Reg 4 Reg 5 Complete the below table to calculate the total bond Interest expense to be recognized over the bonds' life. Total bond interest expense over life of bonds: Amount repaid: payments of Par value at maturity Total repaid 0 Loss amount borrowed Total bond interest expense $ J. LUCTUUR WOHLAPUT Vilevya UVCHI OT hre. 4. Prepare the first two years of a straight-line amortization table. 5. Prepare the journal entries to record the first two interest payments. Complete this question by entering your answers in the tabs below. Reg 1 Reg 2 to 20 Reg 3 Reg 4 Reqs os Prepare the first two years of a straight-line amortization table. (Round your intermediate and final answers to the nearest whole dollar) Semiannual Period- Unamortized Carrying End Premium Value 01/01/2021 06/30/2021 12/31/2021 06/30/2022 12/31/2022 Req3 Req5 > Reg 1 Req ZA to 20 Reg 3 Reg 4 Reg 5 Prepare the journal entries to record the first two interest payments. (Round your intermediate and final answers to the nearest whole dollar) View transaction list Journal entry worksheet Record the first interest payment on June 30. Note: Enter debits before credits General Journal Date June 30 Debit Credit Reg 1 Reg 2A to 2C Reg 3 Reg 4 Reg 5 Prepare the journal entries to record the first two interest payments. (Round your intermediate and final answers to the nearest whole dollar) View transaction list Journal entry worksheet Record the second interest payment on December 31. Note: Enter debits before credits. Date General Journal Debit Credit December 31 Problem 14-2 Straight Line: Amortization of bond premium Hillside issues $4,000,000 of 6%, 15-year bonds dated January 1, 2021, that pay interest semiannually on June 30 and December 31. The bonds are issued at a price of $4,895,980. Required 1. Prepare the January 1, 2011, journal entry to record the bonds' issuance. 2. For each semiannual period, compute (a) the cash payment, (b) the straight-line premium amortization, and (@) the bond interest expense. 3. Determine the total bond interest expense to be recognized over the bonds' life. 4. Prepare the first two years of an amortization table using the straight-line method. 5. Prepare the journal entries to record the first two interest payments. Problem 14-3A Part 1 Bond issue Jan 1, 2021 Cash 4,895,980 Premium on Bonds Payable 895,980 Bonds Payable 4,000,000 Part 2(a) Semi-annual cash payment - Par value $4,000,000 x 6% x 6/12 year = $120,000 - The cash payment is computed the same way no matter if the bond is issued at par, premium, or discount. This amount is governed by the bond indenture contract. (b) Semi-annual Premium Amortization Amount of Premium - Proceeds $4,895,980 - Par value $4,000,000 - $895,980 Straight-line premium amortization-Total premium/ # of semiannual cash payments = $895,980 / 30 semiannual periods (15yrs x 2 payments a year) = $29,866 (c) Bond interest expense = Semi-annual cash payment Less: amortization of the premium. Bond interest expense = $120,000 cash - $29,866 = $90,134 Note: Using the straight line method, the semiannual amounts will be the same throughout the bonds" life Part 3 Total bond interest expense to be recognized over the bonds' life Thirty payments of $120,000 = $ 3,600,000 Less premium (895,980) Total bond interest expense $2,704,020 Or Thirty payments of $120,000 Par value at maturity Total repaid Less amount borrowed Total bond interest expense $ 3,600,000 +4,000,000 -7,600,000 4,895,980 $ 2,704,020 Part 4 Carrying value of Premium Bond - Par value + Unamortized premium. -Original carrying value at issue - Par value $400,000 + Premium 895,980 - $4,895,980 -The premium is amortized (reduced) at each semiannual cash payment period (Semiannual amortization: $895,980/30 - $29,866 -As the premium is slowly amortized (reduced to zero by the time matures), the carrying value of the bond decreases by the same amount each period. (It decreases to par value at maturity.) A B Cash Payment Premium Par Value x i% x 1/2 Amortization $4 mil. X.06 x 1/2 895,980 / 30 Interest Expense A-B C Unamortized Premium Previous - B 895,980 Carrying Value Par Value + c $4,895,980 120,000 29,866 90 134 866, 114 $4,866 114 120,000 29,866 90,134 836,248 $4,836,248 120,000 29,866 90,134 806,382 $4,806,382 120,000 29,866 90,134 76,516 $4,776,516 Part 5 Premium Bond Journal Entries June 30, 2021 Bond Interest Expense 90,134 Premium on Bonds Payable 29,866 Cash 120,000 Premium Bond interest expense = Semi-annual cash payment - amortization of the premium Dec. 31, 2021 Bond Interest Expense 90,134 Premium on Bonds Payable 29,866 Cash 120,000 Discount Bond interest expense - Semi-annual cash payment + amortization of the discount

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts