Question: Please answer all questions and provide step by step solution for each question, provide explanation of the formulas used to obtain your spread-sheet outputs, plots,

Please answer all questions and provide step by step solution for each question, provide explanation of the formulas used to obtain your spread-sheet outputs, plots, tables and spreadsheet data which are clearly la-belled (e.g., where appropriate include the question num-ber, title, parameter names, axis labels, clearly identified final solutions (e.g., if asked to calculate a premium, then do not just present a binomial tree which calculates the premium; instead clearly identify the answer with "The premium is $..."); all numerical results correct to at least four significant figures (unless otherwise specified). Use excel to answer some questions and show the PDF outputs of Excel. Thanks

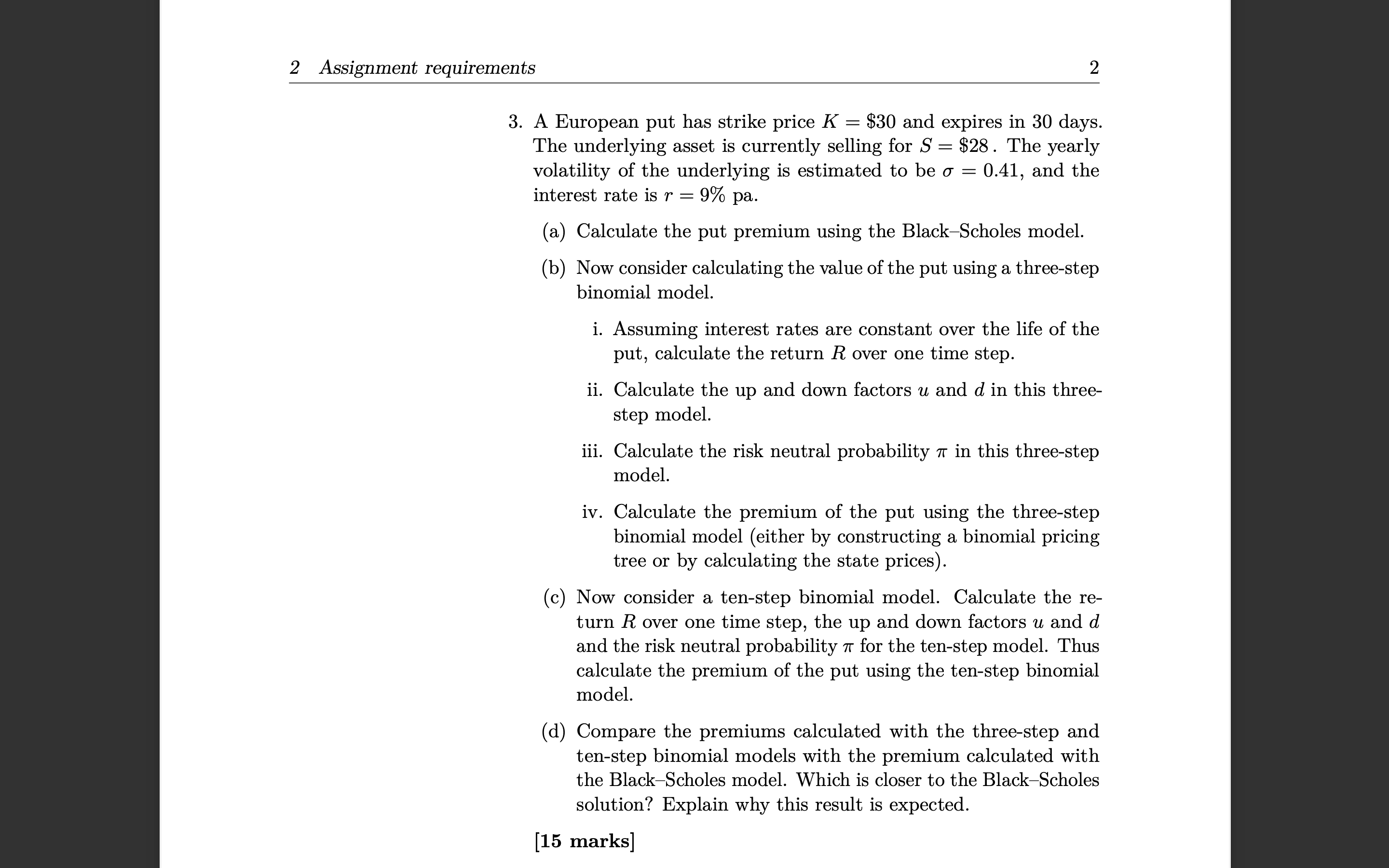

2 Assignment requirements 2 3. A European put has strike price K = $30 and expires in 30 days. The underlying asset is currently selling for S = $28. The yearly volatility of the underlying is estimated to be o = 0.41, and the interest rate is r = 9% pa. (a) Calculate the put premium using the Black-Scholes model. (b) Now consider calculating the value of the put using a three-step binomial model. i. Assuming interest rates are constant over the life of the put, calculate the return R over one time step. ii. Calculate the up and down factors u and d in this three- step model. iii. Calculate the risk neutral probability 7 in this three-step model. iv. Calculate the premium of the put using the three-step binomial model (either by constructing a binomial pricing tree or by calculating the state prices). (c) Now consider a ten-step binomial model. Calculate the re- turn R over one time step, the up and down factors u and d and the risk neutral probability 7 for the ten-step model. Thus calculate the premium of the put using the ten-step binomial model. (d) Compare the premiums calculated with the three-step and ten-step binomial models with the premium calculated with the Black-Scholes model. Which is closer to the Black-Scholes solution? Explain why this result is expected. [15 marks]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!