Question: please answer all things in yellow, I will give a big thumbs up. PART 1: BRAD BROOXS-A Continuing Case Your childhood friend, Brad Brooks, has

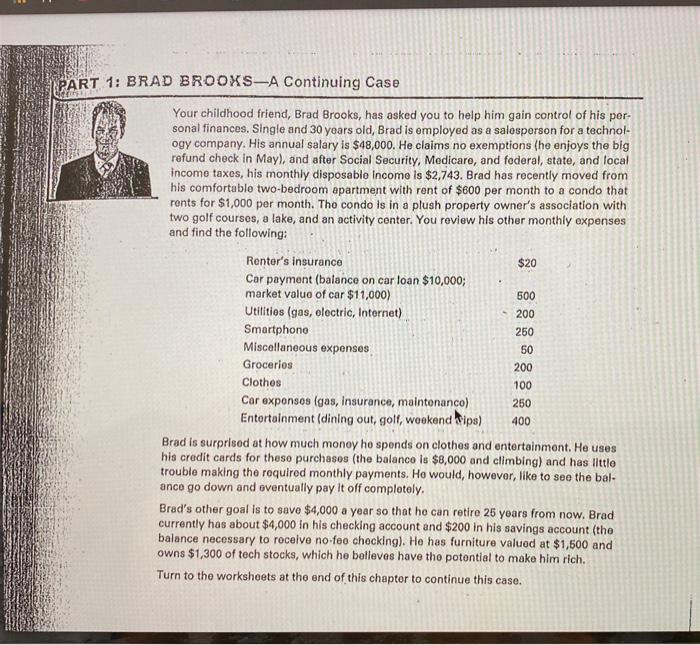

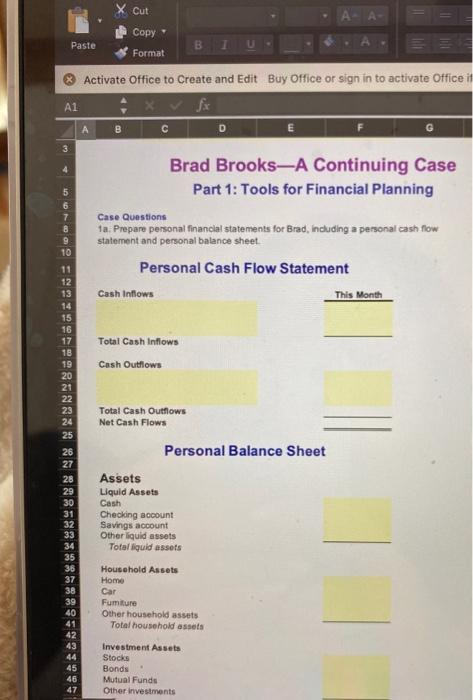

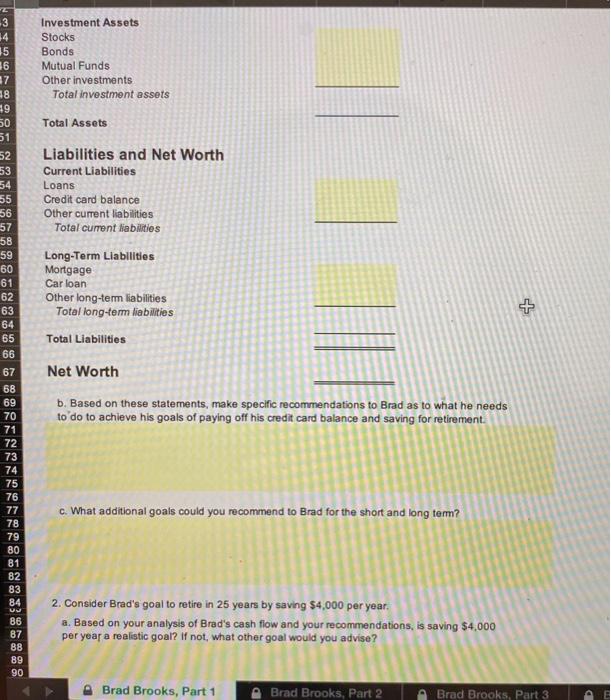

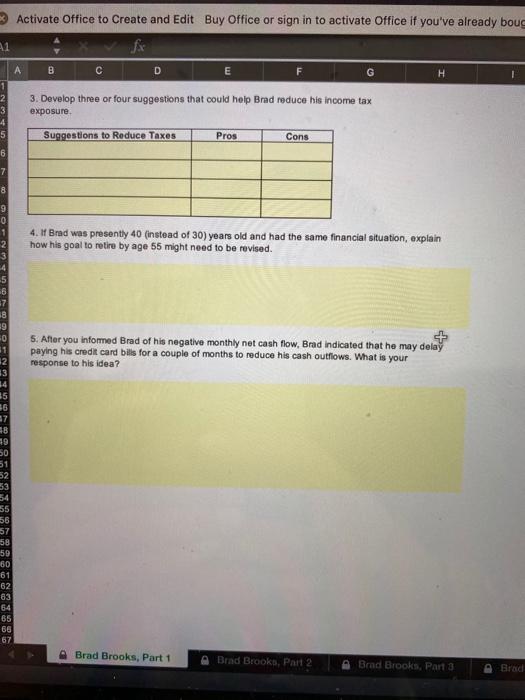

PART 1: BRAD BROOXS-A Continuing Case Your childhood friend, Brad Brooks, has asked you to help him gain control of his per- sonal financos. Single and 30 years old, Brad is employed as a salosporson for a technol- ogy company. His annual salary is $48,000. He claims no exemptions (he enjoys the big refund check in May), and after Social Security, Medicare, and federal, state, and local Income taxes, his monthly disposable Income is $2,743. Brad has recently moved from his comfortablo two-bedroom apartment with rent of $600 per month to a condo that ronts for $1,000 per month. The condo is in a plush property owner's association with two golf coursos, a lake, and an activity center. You review his other monthly expenses and find the following: Rentor's Insurance $20 Car payment (balance on car loan $10,000; market value of car $11,000) 500 Utilities (gas, electric, Internet) 200 Smartphono 250 Miscellaneous expenses 50 Grocerios 200 Clothes 100 Cor exponsos (gas, insurance, maintenanco) 250 Entertainment (dining out, golf, wookend ips) 400 Brad is surprised at how much monoy ho spends on clothes and entertainment. He uses his credit cards for those purchases (the balance is $8,000 and climbing) and has little trouble making the required monthly payments. Ho would, however, like to see the bal- anco go down and eventually pay it off complotely, Brad's other goal is to save $4,000 a year so that he can retire 25 years from now. Brad currently has about $4,000 in his checking account and $200 in his savings account (tho balance necessary to rocelve no foo chocking). He has furniture valuod at $1,500 and owns $1,300 of tech stocks, which he believes have tho potontial to make him rich. Turn to the workshoets at the end of this chapter to continue this case. X cut A- A Paste Copy Format X Activate Office to Create and Edit Buy Office or sign in to activate Office it Al B D E G 3 4 6 Brad BrooksA Continuing Case Part 1: Tools for Financial Planning Case Questions ta: Prepare personal financial statements for Brad, including a personal cash flow statement and personal balance sheet Personal Cash Flow Statement Cash Inflows This Month 10 11 12 14 15 16 17 18 19 20 21 22 23 24 25 Total Cash Inflows Cash Outflows Total Cash Outflows Net Cash Flows Personal Balance Sheet 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 Assets Liquid Assets Cash Checking account Savings account Other liquid assets Totalliquid assets Household Assets Home Car Fumiture Other household assets Total household assets Investment Assets Stocks Bonds Mutual Funds Other investments 3 14 Investment Assets Stocks Bonds Mutual Funds Other investments Total investment assets Total Assets 16 17 18 29 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 Liabilities and Net Worth Current Liabilities Loans Credit card balance Other current liabilities Total current liabilities + Long-Term Liabilities Mortgage Car loan Other long-term liabilities Total long-term liabilities Total Liabilities Net Worth b. Based on these statements, make specific recommendations to Brad as to what he needs to do to achieve his goals of paying off his credit card balance and saving for retirement. 67 68 69 70 71 c. What additional goals could you recommend to Brad for the short and long term? 72 73 74 75 76 77 78 79 80 81 82 83 84 U 86 87 88 B9 90 2. Consider Brad's goal to retire in 25 years by saving $4,000 per year. a. Based on your analysis of Brad's cash flow and your recommendations, is saving $4,000 per year a realistic goal? If not, what other goal would you advise? Brad Brooks, Part 1 Brad Brooks, Part 2 Brad Brooks, Part 3 > Activate Office to Create and Edit Buy Office or sign in to activate Office if you've already boue 41 A B D E H 1 2 3 -4 5 3. Develop three or four suggestions that could help Brad reduce his income tax exposure Suggestions to Reduce Taxes Pros Cons 6 7 8 9 0 1 2 3 4. Brad was presently 40 (instead of 30) years old and had the same financial situation, explain how his goal to retire by age 55 might need to be revised. 5. After you infomed Brad of his negative monthly net cash flow, Brad indicated that he may delay paying his credit card bills for a couple of months to reduce his cash outflows. What is your response to his idea? -5 -6 37 38 19 -0 11 12 13 14 35 36 27 8 9 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 D Brad Brooks, Part 1 A Brad Brooks, Part 2 Brad Brooks, Part 3 Brad PART 1: BRAD BROOXS-A Continuing Case Your childhood friend, Brad Brooks, has asked you to help him gain control of his per- sonal financos. Single and 30 years old, Brad is employed as a salosporson for a technol- ogy company. His annual salary is $48,000. He claims no exemptions (he enjoys the big refund check in May), and after Social Security, Medicare, and federal, state, and local Income taxes, his monthly disposable Income is $2,743. Brad has recently moved from his comfortablo two-bedroom apartment with rent of $600 per month to a condo that ronts for $1,000 per month. The condo is in a plush property owner's association with two golf coursos, a lake, and an activity center. You review his other monthly expenses and find the following: Rentor's Insurance $20 Car payment (balance on car loan $10,000; market value of car $11,000) 500 Utilities (gas, electric, Internet) 200 Smartphono 250 Miscellaneous expenses 50 Grocerios 200 Clothes 100 Cor exponsos (gas, insurance, maintenanco) 250 Entertainment (dining out, golf, wookend ips) 400 Brad is surprised at how much monoy ho spends on clothes and entertainment. He uses his credit cards for those purchases (the balance is $8,000 and climbing) and has little trouble making the required monthly payments. Ho would, however, like to see the bal- anco go down and eventually pay it off complotely, Brad's other goal is to save $4,000 a year so that he can retire 25 years from now. Brad currently has about $4,000 in his checking account and $200 in his savings account (tho balance necessary to rocelve no foo chocking). He has furniture valuod at $1,500 and owns $1,300 of tech stocks, which he believes have tho potontial to make him rich. Turn to the workshoets at the end of this chapter to continue this case. X cut A- A Paste Copy Format X Activate Office to Create and Edit Buy Office or sign in to activate Office it Al B D E G 3 4 6 Brad BrooksA Continuing Case Part 1: Tools for Financial Planning Case Questions ta: Prepare personal financial statements for Brad, including a personal cash flow statement and personal balance sheet Personal Cash Flow Statement Cash Inflows This Month 10 11 12 14 15 16 17 18 19 20 21 22 23 24 25 Total Cash Inflows Cash Outflows Total Cash Outflows Net Cash Flows Personal Balance Sheet 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 Assets Liquid Assets Cash Checking account Savings account Other liquid assets Totalliquid assets Household Assets Home Car Fumiture Other household assets Total household assets Investment Assets Stocks Bonds Mutual Funds Other investments 3 14 Investment Assets Stocks Bonds Mutual Funds Other investments Total investment assets Total Assets 16 17 18 29 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 Liabilities and Net Worth Current Liabilities Loans Credit card balance Other current liabilities Total current liabilities + Long-Term Liabilities Mortgage Car loan Other long-term liabilities Total long-term liabilities Total Liabilities Net Worth b. Based on these statements, make specific recommendations to Brad as to what he needs to do to achieve his goals of paying off his credit card balance and saving for retirement. 67 68 69 70 71 c. What additional goals could you recommend to Brad for the short and long term? 72 73 74 75 76 77 78 79 80 81 82 83 84 U 86 87 88 B9 90 2. Consider Brad's goal to retire in 25 years by saving $4,000 per year. a. Based on your analysis of Brad's cash flow and your recommendations, is saving $4,000 per year a realistic goal? If not, what other goal would you advise? Brad Brooks, Part 1 Brad Brooks, Part 2 Brad Brooks, Part 3 > Activate Office to Create and Edit Buy Office or sign in to activate Office if you've already boue 41 A B D E H 1 2 3 -4 5 3. Develop three or four suggestions that could help Brad reduce his income tax exposure Suggestions to Reduce Taxes Pros Cons 6 7 8 9 0 1 2 3 4. Brad was presently 40 (instead of 30) years old and had the same financial situation, explain how his goal to retire by age 55 might need to be revised. 5. After you infomed Brad of his negative monthly net cash flow, Brad indicated that he may delay paying his credit card bills for a couple of months to reduce his cash outflows. What is your response to his idea? -5 -6 37 38 19 -0 11 12 13 14 35 36 27 8 9 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 D Brad Brooks, Part 1 A Brad Brooks, Part 2 Brad Brooks, Part 3 Brad

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts