Question: please answer and show work Intro Assume that the single index model is valid. You've collected the following information about excess returns for two stocks,

please answer and show work

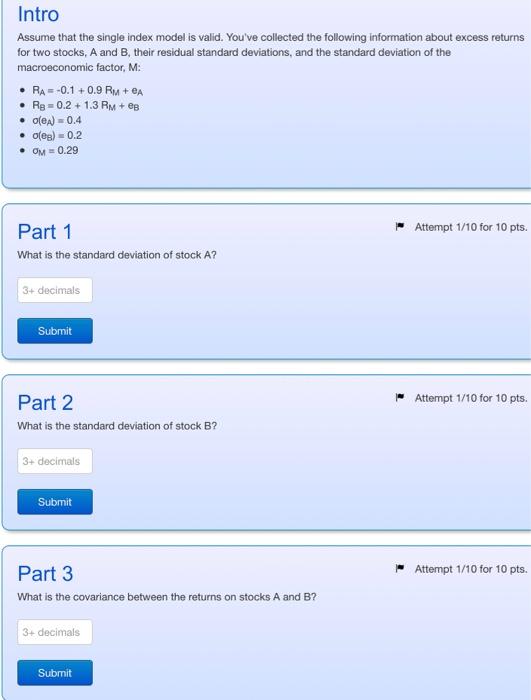

Intro Assume that the single index model is valid. You've collected the following information about excess returns for two stocks, A and B, their residual standard deviations, and the standard deviation of the macroeconomic factor, M : RA=0.1+0.9RM+eA - RB=0.2+1.3RM+eB o(eA)=0.4 - o(eB)=0.2 - M=0.29 Part 1 Attempt 1/10 for 10 pts. What is the standard deviation of stock A? Part 2 Attempt 1/10 for 10 pts. What is the standard deviation of stock B? Part 3 Attempt 1/10 for 10 pts. What is the covariance between the returns on stocks A and B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock