Question: please answer as many as possible 12. United Donees a Restricted for capital addition The All pledges are legaily enforceable and are experience of United

please answer as many as possible

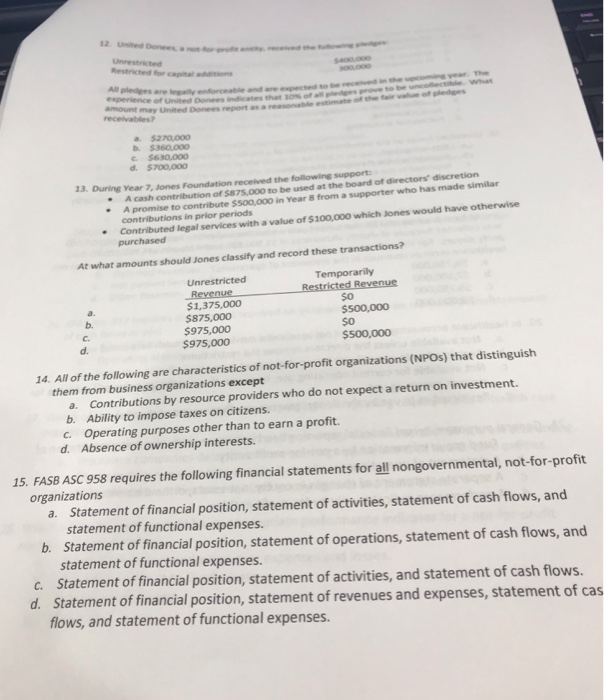

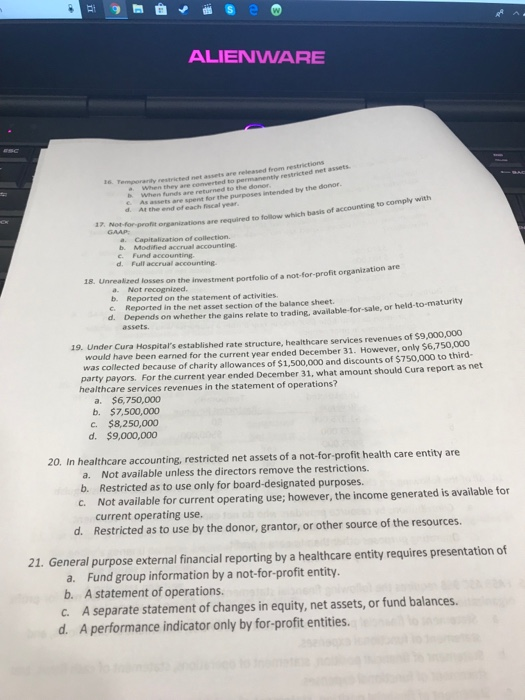

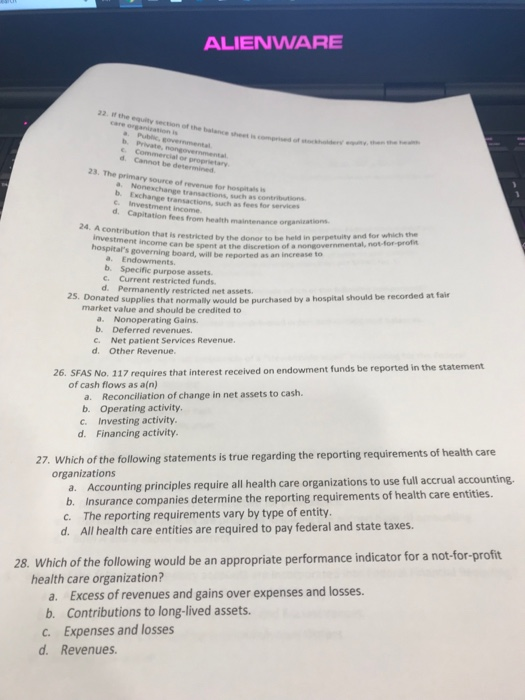

12. United Donees a Restricted for capital addition The All pledges are legaily enforceable and are experience of United Donees indicates amount may United Donees report as a espected to be receved in the coine year a. $270,000 b. $360,000 d. $700,000 contribution of $875,000 to be used at the board of directors' discretion A promise to contribute $500,000 in Year 8 from a supporter who has made similar 13. During Year 7, Jones Foundation received the following support * A cash contributions in prior periods Contributed legal services with a value of $100,000 which Jones would have otherwise At what amounts should Jones classify and record these transactions? Temporanry Unrestricted a. b. c. $1,375,000 $875,000 $975,000 $975,000 so $500,000 so $500,000 d. 14. All of the following are characteristics of not-for-profit organizations (NPOs) that distinguish them from business organizations except a. Contributions by resource providers who do not expect a return on investment. b. Ability to impose taxes on citizens. c. Operating purposes other than to earn a profit. d. Absence of ownership interests. 15. FASB ASc 958 requires the following financial statements for all nongovernmental, not-for-profit organizations a. Statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses. Statement of financial position, statement of operations, statement of cash flows, and statement of functional expenses. b. c. Statement of financial position, statement of activities, and statement of cash flows. Statement of financial position, statement of revenues and expenses, statement of cas flows, and statement of functional expenses. d. ALIENWARE l. Temporarty restricted net assets are released from restrictions permanently restricted net C As assets are spent for the purposes intended by the donor. d. At the end of each fiscal year B When fundls are returned to the organizations are required to follow which basis of accounting to comply with b. Moified accrual accounting d. Full accrual accounting. Unrealized losses on the investment portfolio of a not-for-profit organization are a. Not recognized. b. Reported on the statement of activities c. Reported in the net asset section of the balance sheet. d. Depends on whether the gains relate to trading, available-for-sale, or held-to-maturity assets. 19. Under Cura Hospital's established rate structure, healthcare services revenues of $9,000,000 would have been earned for the current year ended December 31. However, only $6,750,000 was collected because of charity allowances of $1,500,000 and discounts of $750,000 to third- party payors. For the current year ended December 31, what amount should Cura report as net healthcare services revenues in the statement of operations? a. $6,750,000 b. $7,500,000 C. $8,250,000 d. $9,000,000 20. In healthcare accounting, restricted net assets of a not-for-profit health care entity are a. b. c. Not available unless the directors remove the restrictions. Restricted as to use only for board-designated purposes. Not available for current operating use; however, the income generated is available for current operating use. d. Restricted as to use by the donor, grantor, or other source of the resources 21. General purpose external financial reporting by a healthcare entity requires presentation of a. Fund group information by a not-for-profit entity. b. A statement of operations. c. A separate statement of changes in equity, net assets, or fund balances d. A performance indicator only by for-profit entities. ALIENWARE 22. I# the equity section of the balance sheet w is compied of hdr c. Com d. Cannot be 23. The primary source of revenue for hospitalsi b. Exchange transact c. Investment d. Capitation fees from health maintenance e transactions, such as contributions ions, such as fees for servicets 24. A con that is restricted by the donor to be held in perpetulty and for which the can be spent at the discretion of a nongovernmental, not for-profit hospitar's governing board, will e reported as anina to a Endowments c. Current restricted funds d. Permanently restricted net assets 2. Donated supplies that normally would be purchased by a hospital should be recorded at fair market value and should be credited to a. Nonoperating Gains b. Deferred revenues C. Net patient Services Revenue. d. Other Revenue. 26. SFAS No. 117 requires that interest received on endowment funds be reported in the statement of cash flows as a(n) a. Reconciliation of change in net assets to cash. b. Operating activity. c. Investing activity d. Financing activity 27. Which of the following statements is true regarding the reporting requirements of health care a. Accounting principles require all health care organizations to use full accrual accounting. b. Insurance companies determine the reporting requirements of health care entities. c. The reporting requirements vary by type of entity. d. All health care entities are required to pay federal and state taxes organizations 28. Which of the following would be an appropriate performance indicator for a not-for-profit health care organization? a. Excess of revenues and gains over expenses and losses. b. Contributions to long-lived assets. c. Expenses and losses d. Revenues

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts