Question: please answer ASAP. Don't worry about the answer. jus follow proper procedure. thank you. please let me know if the question belongs to some other

please answer ASAP.

Don't worry about the answer. jus follow proper procedure. thank you.

please let me know if the question belongs to some other subject. thank you.

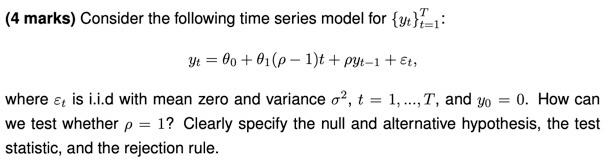

(4 marks) Consider the following time series model for {yt }-1: yt = 00 + 01(p - 1)t + pyt-1 + Et, where & is i.i.d with mean zero and variance of, t = 1, ...,T, and yo = 0. How can we test whether p = 1? Clearly specify the null and alternative hypothesis, the test statistic, and the rejection rule

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock