Question: please answer both (c) and (d) please provide working. Kenanga Investment Bank is evaluating an equity. Recently, Malaysia government's risk free rate is 3.5%. Calculate

please answer both (c) and (d)

please provide working.

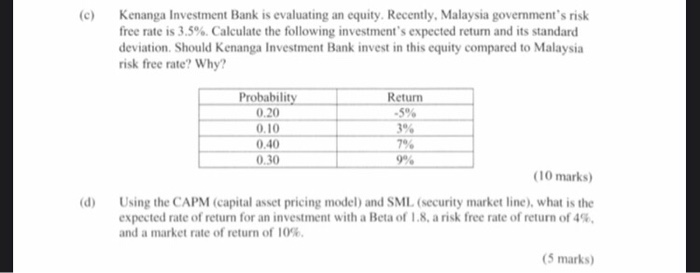

Kenanga Investment Bank is evaluating an equity. Recently, Malaysia government's risk free rate is 3.5%. Calculate the following investment's expected retun and its standard deviation. Should Kenanga Investment Bank invest in this equity compared to Malaysia risk free rate? Why (c) Return -5% 3% 7% 9% Probability 0.20 0.10 0.40 0.30 (10 marks) (d) Using the CAPM (capital asset pricing model) and SML (security market line), what is the expected rate of return for an investment with a Beta of 1.8, a risk free rate of return of 4% and a market rate of return of 10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock