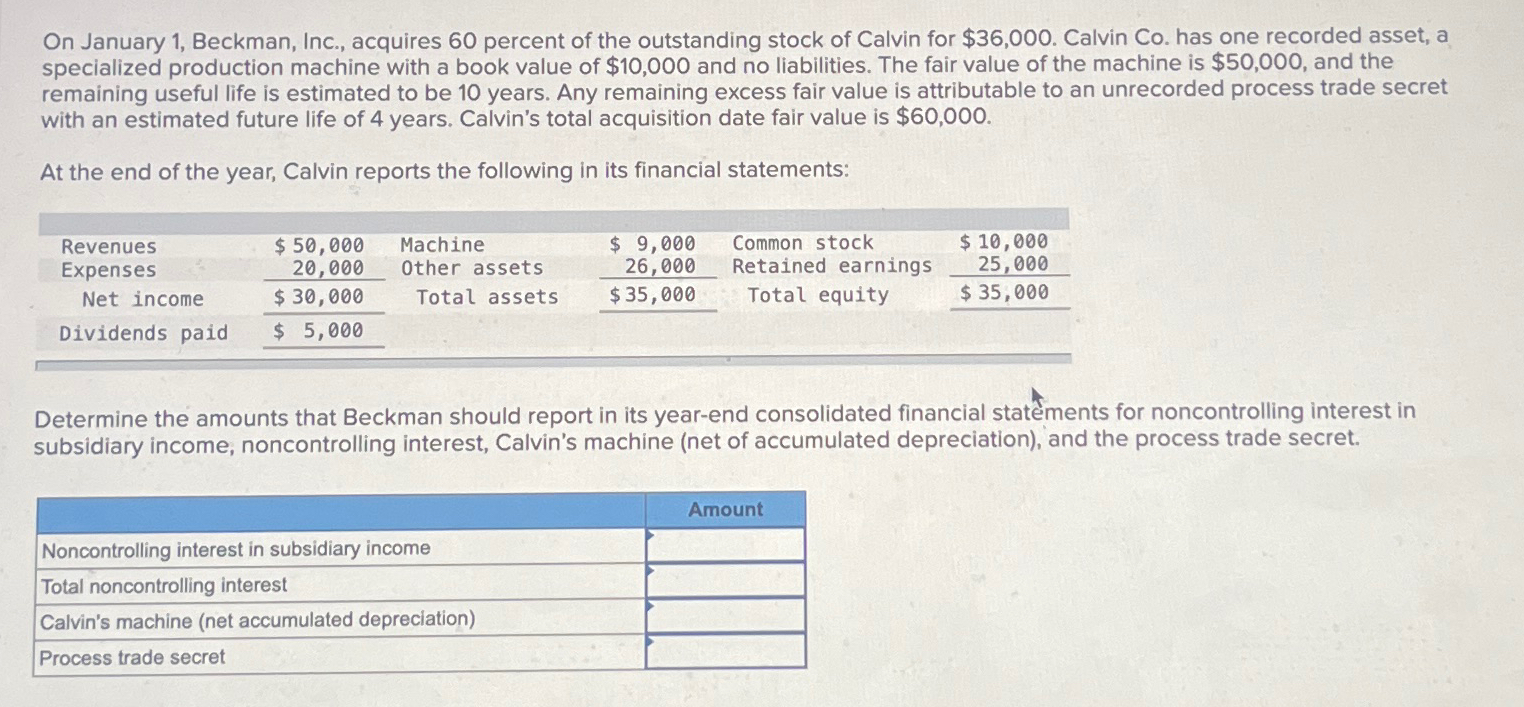

Question: please answer correct, second time posting this because it was wrong.On January 1 , Beckman, Inc., acquires 6 0 percent of the outstanding stock of

please answer correct, second time posting this because it was wrong.On January Beckman, Inc., acquires percent of the outstanding stock of Calvin for $ Calvin Co has one recorded asset, a specialized production machine with a book value of $ and no liabilities. The fair value of the machine is $ and the remaining useful life is estimated to be years. Any remaining excess fair value is attributable to an unrecorded process trade secret with an estimated future life of years. Calvin's total acquisition date fair value is $

At the end of the year, Calvin reports the following in its financial statements:

tabletableRevenuesExpensestable$

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock