Question: Please answer in detailed steps. Exercise 5.10. Three assets A,B, and C have market prices and payoffs as given in the table below: (a) Construct

Please answer in detailed steps.

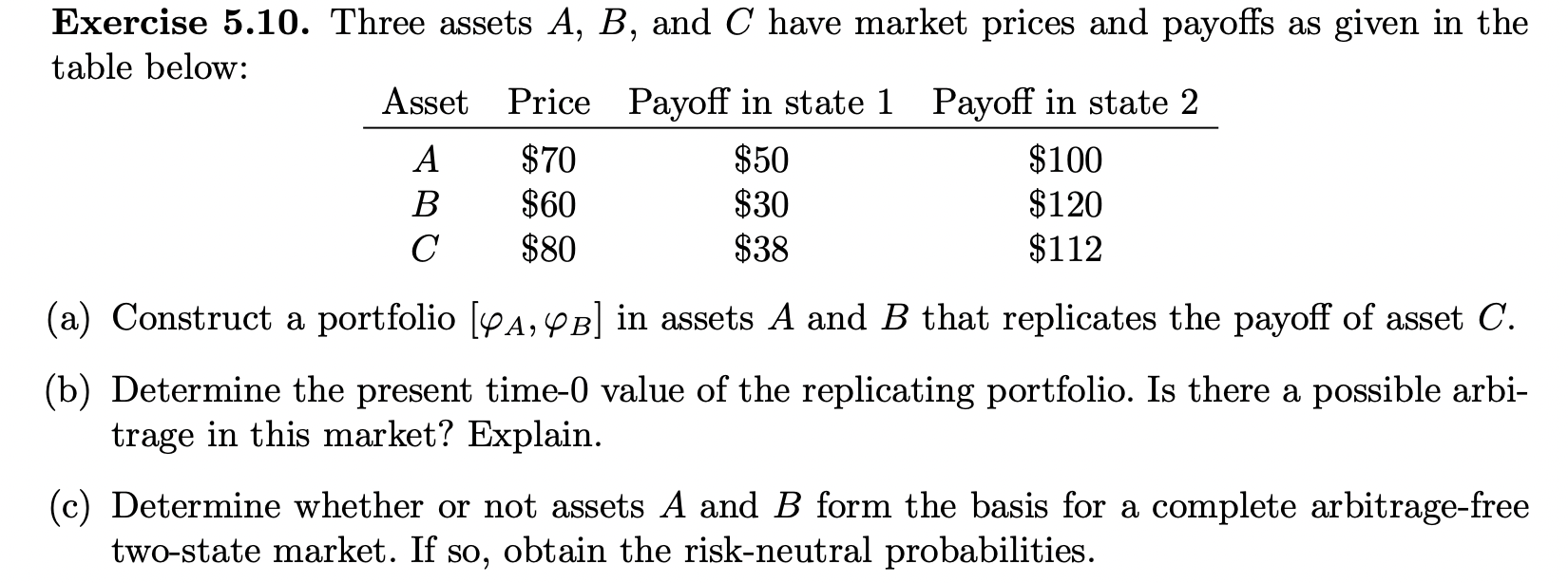

Exercise 5.10. Three assets A,B, and C have market prices and payoffs as given in the table below: (a) Construct a portfolio [A,B] in assets A and B that replicates the payoff of asset C. (b) Determine the present time- 0 value of the replicating portfolio. Is there a possible arbitrage in this market? Explain. (c) Determine whether or not assets A and B form the basis for a complete arbitrage-free two-state market. If so, obtain the risk-neutral probabilities

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock