Question: please answer on a paper as fast aa you can #4) (30 Marks) Your client Zebra Inc. has come to you and asked for your

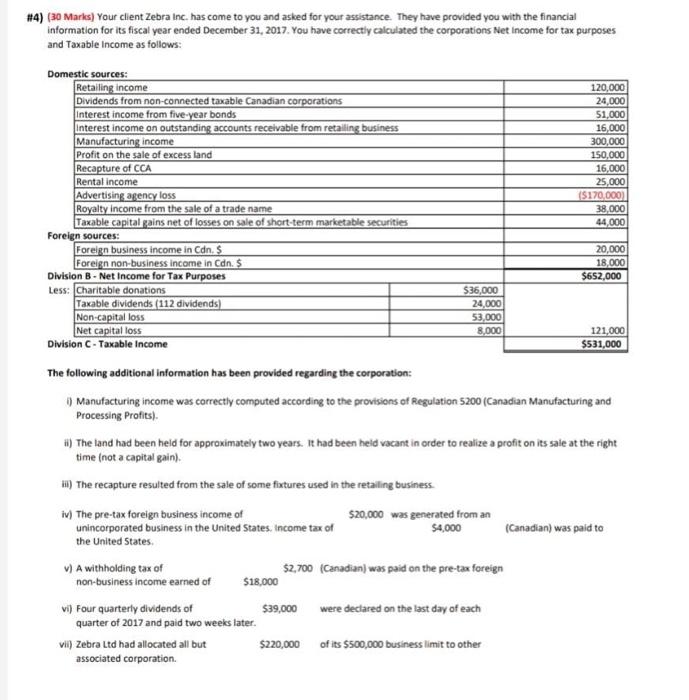

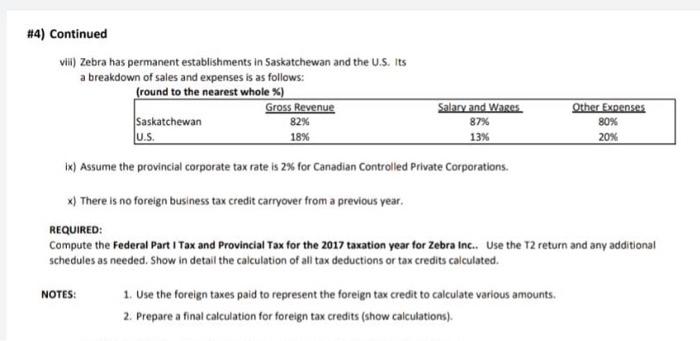

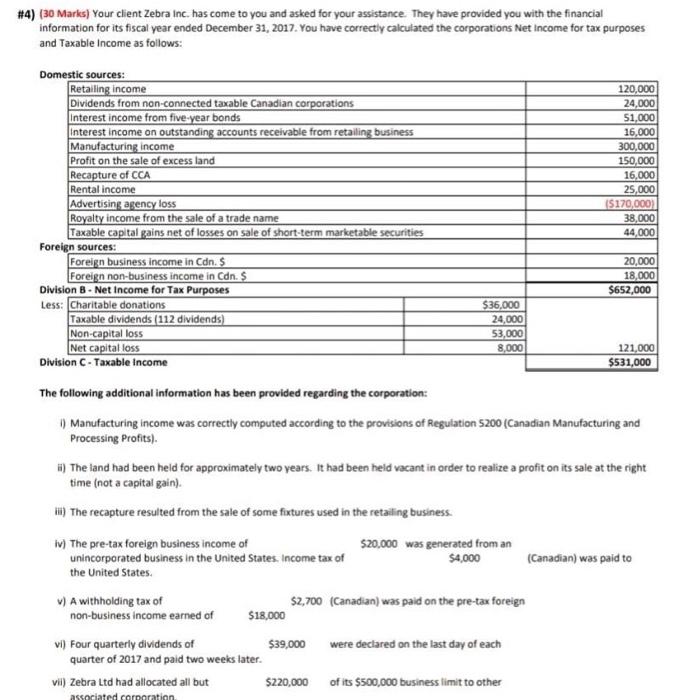

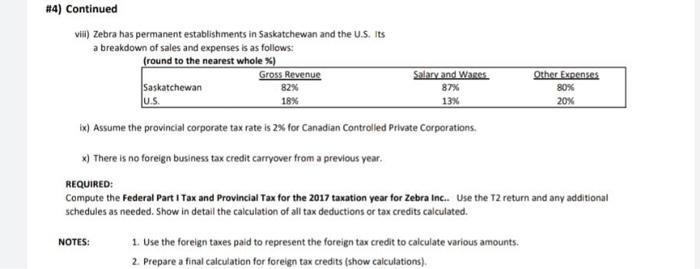

#4) (30 Marks) Your client Zebra Inc. has come to you and asked for your assistance. They have provided you with the financial information for its fiscal year ended December 31, 2017. You have correctly calculated the corporations Net Income for tax purposes and Taxable income as follows: Domestic sources: Retailing income Dividends from non-connected taxable Canadian corporations Interest income from five-year bonds Interest income an outstanding accounts receivable from retailing business Manufacturing income Profit on the sale of excess land Recapture of CCA Rental income Advertising agency loss Royalty income from the sale of a trade name Taxable capital gains net of losses on sale of short-term marketable securities Foreign sources: Foreign business income in Cans Foreign non-business income in Cdn. $ Division B - Net Income for Tax Purposes Less: Charitable donations Taxable dividends (112 dividends) Non-capital loss Net capital loss Division - Taxable income 120,000 24,000 51,000 16,000 300,000 150,000 16,000 25,000 15170,000 38,000 44,000 20,000 18,000 $652,000 $36,000 24,000 53,000 8,000 121,000 $531,000 The following additional information has been provided regarding the corporation: Manufacturing income was correctly computed according to the provisions of Regulation 5200 (Canadian Manufacturing and Processing Profits). ii) The land had been held for approximately two years. It had been held vacant in order to realize a profit on its sale at the right time (not a capital gain) H) The recapture resulted from the sale of some fixtures used in the retailing business iv) The pre-tax foreign business income of $20,000 was generated from an unincorporated business in the United States, Income tax of $4,000 (Canadian) was paid to the United States v) A withholding tax of $2,700 (Canadian) was paid on the pre-tax foreign non-business income earned of $18,000 vi) Four quarterly dividends of $39,000 were declared on the last day of each quarter of 2017 and paid two weeks later. Vill) Zebra Ltd had allocated all but $220,000 of its $500,000 business limit to other associated corporation. #4) Continued vil) Zebra has permanent establishments in Saskatchewan and the U.S. Its a breakdown of sales and expenses is as follows: (round to the nearest whole %) Gross Revenue Saskatchewan 82% U.S. 18% Salary and Wares 87% 13% Other Expenses 80% 20% IK) Assume the provincial corporate tax rate is 2% for Canadian Controlled Private Corporations. x) There is no foreign business tax credit carryover from a previous year. REQUIRED: Compute the Federal Part I Tax and Provincial Tax for the 2017 taxation year for Zebra Inc.. Use the T2 return and any additional schedules as needed. Show in detail the calculation of all tax deductions or tax credits calculated. NOTES: 1. Use the foreign taxes paid to represent the foreign tax credit to calculate various amounts. 2. Prepare a final calculation for foreign tax credits (show calculations). #4) (30 Marks) Your client Zebra Inc. has come to you and asked for your assistance. They have provided you with the financial information for its fiscal year ended December 31, 2017. You have correctly calculated the corporations Net Income for tax purposes and Taxable income as follows: Domestic sources: Retailing income Dividends from non-connected taxable Canadian corporations Interest income from five-year bonds Interest income on outstanding accounts receivable from retailing business Manufacturing income Profit on the sale of excess land Recapture of CCA Rental income Advertising agency loss Royalty income from the sale of a trade name Taxable capital gains net of losses on sale of short-term marketable securities Foreign sources: Foreign business income in Can. $ Foreign non-business income in Can. $ Division 8 - Net Income for Tax Purposes Less: Charitable donations Taxable dividends (112 dividends) Non-capital loss Net capital loss Division - Taxable income 120,000 24,000 $1,000 16,000 300,000 150,000 16,000 25,000 15170,000 38,000 44,000 a 20,000 18,000 $652,000 $36.000 24,000 53,000 8,000 121,000 $531,000 The following additional information has been provided regarding the corporation: ) Manufacturing income was correctly computed according to the provisions of Regulation 5200 Canadian Manufacturing and Processing Profits). 6) The land had been held for approximately two years. It had been held vacant in order to realize a profit on its sale at the right time (not a capital gain). i) The recapture resulted from the sale of some fixtures used in the retailing business iv) The pre-tax foreign business income of $20,000 was generated from an unincorporated business in the United States. Income tax of $4,000 (Canadian) was paid to the United States v) A withholding tax of $2,700 (Canadian) was paid on the pre-tax foreign non-business income earned of $18,000 vi) Four quarterly dividends of $39,000 were declared on the last day of each quarter of 2017 and paid two weeks later. vil) Zebra Ltd had allocated all but $220,000 of its $500,000 business limit to other associated corporation #4) Continued vill) Zebra has permanent establishments in Saskatchewan and the U.S. Its a breakdown of sales and expenses is as follows: (round to the nearest whole ) Gross Revenue Saskatchewan U.S. 1x) Assume the provincial corporate tax rate is 2% for Canadian Controlled Private Corporations 82% 18% Salary and Wares 87% 13% Other Expenses 80% 20% *) There is no foreign business tax credit carryover from a previous year. REQUIRED: Compute the Federal Part I Tax and Provincial Tax for the 2017 taxation year for Zebra Inc. Use the T2 return and any additional schedules as needed. Show in detail the calculation of all tax deductions or tax credits calculated. NOTES: 1. Use the foreign taxes paid to represent the foreign tax credit to calculate various amounts. 2. Prepare a final calculation for foreign tax credits (show calculations), #4) (30 Marks) Your client Zebra Inc. has come to you and asked for your assistance. They have provided you with the financial information for its fiscal year ended December 31, 2017. You have correctly calculated the corporations Net Income for tax purposes and Taxable income as follows: Domestic sources: Retailing income Dividends from non-connected taxable Canadian corporations Interest income from five-year bonds Interest income an outstanding accounts receivable from retailing business Manufacturing income Profit on the sale of excess land Recapture of CCA Rental income Advertising agency loss Royalty income from the sale of a trade name Taxable capital gains net of losses on sale of short-term marketable securities Foreign sources: Foreign business income in Cans Foreign non-business income in Cdn. $ Division B - Net Income for Tax Purposes Less: Charitable donations Taxable dividends (112 dividends) Non-capital loss Net capital loss Division - Taxable income 120,000 24,000 51,000 16,000 300,000 150,000 16,000 25,000 15170,000 38,000 44,000 20,000 18,000 $652,000 $36,000 24,000 53,000 8,000 121,000 $531,000 The following additional information has been provided regarding the corporation: Manufacturing income was correctly computed according to the provisions of Regulation 5200 (Canadian Manufacturing and Processing Profits). ii) The land had been held for approximately two years. It had been held vacant in order to realize a profit on its sale at the right time (not a capital gain) H) The recapture resulted from the sale of some fixtures used in the retailing business iv) The pre-tax foreign business income of $20,000 was generated from an unincorporated business in the United States, Income tax of $4,000 (Canadian) was paid to the United States v) A withholding tax of $2,700 (Canadian) was paid on the pre-tax foreign non-business income earned of $18,000 vi) Four quarterly dividends of $39,000 were declared on the last day of each quarter of 2017 and paid two weeks later. Vill) Zebra Ltd had allocated all but $220,000 of its $500,000 business limit to other associated corporation. #4) Continued vil) Zebra has permanent establishments in Saskatchewan and the U.S. Its a breakdown of sales and expenses is as follows: (round to the nearest whole %) Gross Revenue Saskatchewan 82% U.S. 18% Salary and Wares 87% 13% Other Expenses 80% 20% IK) Assume the provincial corporate tax rate is 2% for Canadian Controlled Private Corporations. x) There is no foreign business tax credit carryover from a previous year. REQUIRED: Compute the Federal Part I Tax and Provincial Tax for the 2017 taxation year for Zebra Inc.. Use the T2 return and any additional schedules as needed. Show in detail the calculation of all tax deductions or tax credits calculated. NOTES: 1. Use the foreign taxes paid to represent the foreign tax credit to calculate various amounts. 2. Prepare a final calculation for foreign tax credits (show calculations). #4) (30 Marks) Your client Zebra Inc. has come to you and asked for your assistance. They have provided you with the financial information for its fiscal year ended December 31, 2017. You have correctly calculated the corporations Net Income for tax purposes and Taxable income as follows: Domestic sources: Retailing income Dividends from non-connected taxable Canadian corporations Interest income from five-year bonds Interest income on outstanding accounts receivable from retailing business Manufacturing income Profit on the sale of excess land Recapture of CCA Rental income Advertising agency loss Royalty income from the sale of a trade name Taxable capital gains net of losses on sale of short-term marketable securities Foreign sources: Foreign business income in Can. $ Foreign non-business income in Can. $ Division 8 - Net Income for Tax Purposes Less: Charitable donations Taxable dividends (112 dividends) Non-capital loss Net capital loss Division - Taxable income 120,000 24,000 $1,000 16,000 300,000 150,000 16,000 25,000 15170,000 38,000 44,000 a 20,000 18,000 $652,000 $36.000 24,000 53,000 8,000 121,000 $531,000 The following additional information has been provided regarding the corporation: ) Manufacturing income was correctly computed according to the provisions of Regulation 5200 Canadian Manufacturing and Processing Profits). 6) The land had been held for approximately two years. It had been held vacant in order to realize a profit on its sale at the right time (not a capital gain). i) The recapture resulted from the sale of some fixtures used in the retailing business iv) The pre-tax foreign business income of $20,000 was generated from an unincorporated business in the United States. Income tax of $4,000 (Canadian) was paid to the United States v) A withholding tax of $2,700 (Canadian) was paid on the pre-tax foreign non-business income earned of $18,000 vi) Four quarterly dividends of $39,000 were declared on the last day of each quarter of 2017 and paid two weeks later. vil) Zebra Ltd had allocated all but $220,000 of its $500,000 business limit to other associated corporation #4) Continued vill) Zebra has permanent establishments in Saskatchewan and the U.S. Its a breakdown of sales and expenses is as follows: (round to the nearest whole ) Gross Revenue Saskatchewan U.S. 1x) Assume the provincial corporate tax rate is 2% for Canadian Controlled Private Corporations 82% 18% Salary and Wares 87% 13% Other Expenses 80% 20% *) There is no foreign business tax credit carryover from a previous year. REQUIRED: Compute the Federal Part I Tax and Provincial Tax for the 2017 taxation year for Zebra Inc. Use the T2 return and any additional schedules as needed. Show in detail the calculation of all tax deductions or tax credits calculated. NOTES: 1. Use the foreign taxes paid to represent the foreign tax credit to calculate various amounts. 2. Prepare a final calculation for foreign tax credits (show calculations)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts