Question: please answer part C and show your work, do not use excel. Part III: Risk and Return Analysis. This section of the test addresses the

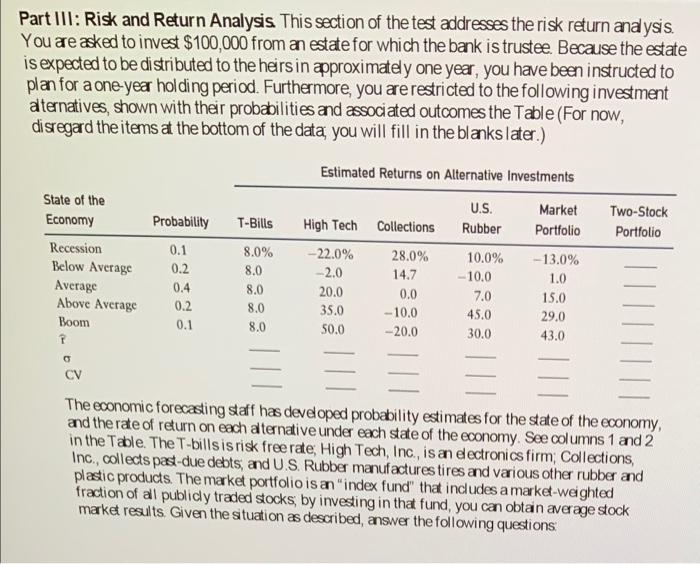

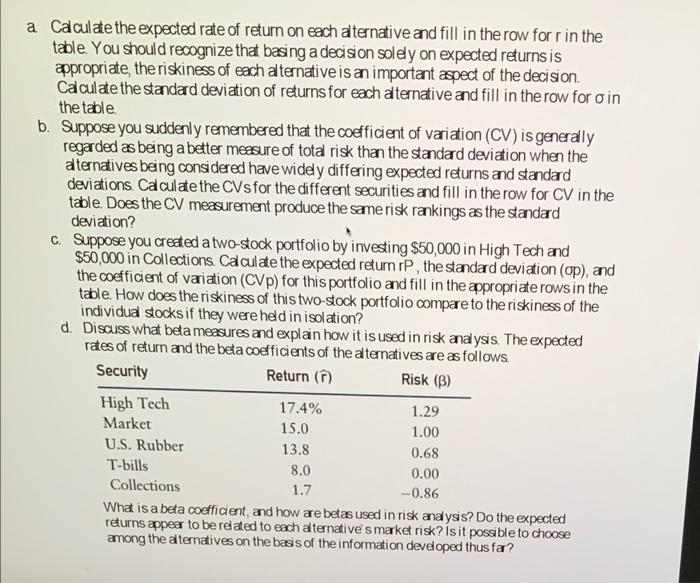

Part III: Risk and Return Analysis. This section of the test addresses the risk return analysis. You are asked to invest $100,000 from an estate for which the bank is trustee. Because the estate is expected to be distributed to the heirs in approximately one year, you have been instructed to plan for a one year holding period. Furthermore, you are restricted to the following investment alternatives , shown with their probabilities and associated outcomes the Table (For now, disregard the items at the bottom of the data, you will fill in the blanks later.) Estimated Returns on Alternative Investments State of the U.S. Market Two-Stock Economy Probability T-Bills High Tech Collections Rubber Portfolio Portfolio Recession 0.1 8.0% --22.0% 28.0% 10.0% -13.0% Below Average 0.2 8.0 -2.0 14.7 -10.0 1.0 Average 0.4 8.0 20.0 0.0 7.0 15.0 Above Average 0.2 8.0 35.0 -10.0 45.0 29.0 Boom 0.1 50.0 - 20.0 30.0 43.0 8.0 1 0 CV The economic forecasting staff has developed probability estimates for the state of the economy, and the rate of return on each alternative under each state of the economy. See columns 1 and 2 in the Table. The T-billsis risk free rate, High Tech, Inc., is an electronics firm, Collections, Inc., collects past-due debts, and U.S. Rubber manufactures tires and various other rubber and plastic products. The market portfolio is an "index fund that includes a market-weighted fraction of all publicly traded stocks, by investing in that fund, you can obtain average stock market results. Given the situation as described, answer the following questions: a Calculate the expected rate of return on each alternative and fill in the row for r in the table. You should recognize that basing a decision solely on expected returns is appropriate, the riskiness of each alternative is an important aspect of the decision. Calculate the standard deviation of returns for each alternative and fill in the row for o in the table b. Suppose you suddenly remembered that the coefficient of variation (CV) is generally regarded as being a better measure of total risk than the standard deviation when the alternatives being considered have widely differing expected returns and standard deviations. Calculate the CVs for the different securities and fill in the row for CV in the table. Does the CV measurement produce the same risk rankings as the standard deviation? c. Suppose you created a two-stock portfolio by investing $50,000 in High Tech and $50,000 in Collections Calculate the expected return rP, the standard deviation (op), and the coefficient of variation (CVP) for this portfolio and fill in the appropriate rows in the table. How does the riskiness of this two-stock portfolio compare to the riskiness of the individual stocks if they were held in isolation? d. Discuss what beta measures and explain how it is used in risk analysis. The expected rates of return and the beta coefficients of the alternatives are as follows. Security Return () Risk (B) High Tech 17.4% 1.29 Market 15.0 1.00 U.S. Rubber 13.8 0.68 T-bills 8.0 0.00 Collections 1.7 -0.86 What is a beta coefficient, and how are betas used in risk analysis? Do the expected returns appear to be related to each alternative's market risk? Is it possible to choose among the alternatives on the basis of the information developed thus fa

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts