Question: please answer question 19 and show all work and formulas used. The answer to 17 is 2% All information is on the first photo Use

please answer question 19 and show all work and formulas used. The answer to 17 is 2%

All information is on the first photo

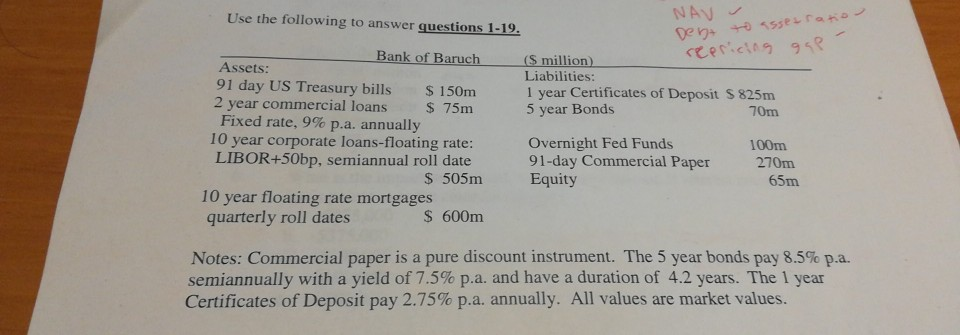

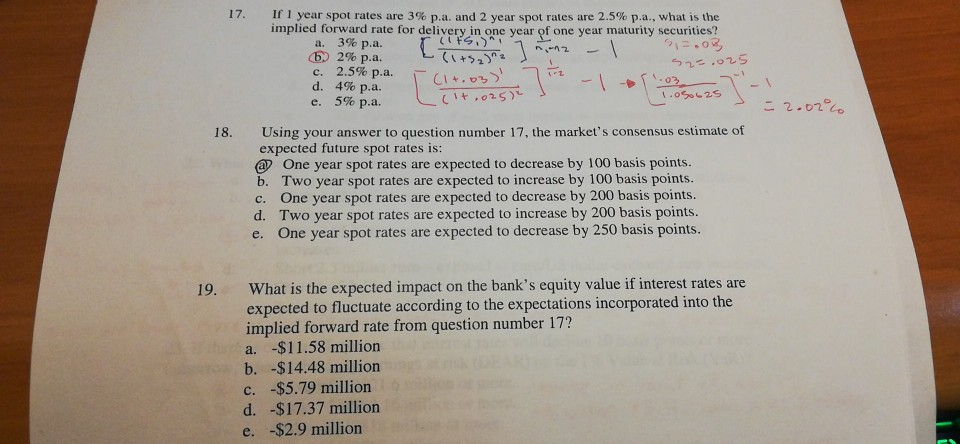

Use the following to answer questions 1-19. NAV I Den to assessation repricing gap ($ million Liabilities: 1 year Certificates of Deposit S 825m 5 year Bonds 70m Bank of Baruch Assets: 91 day US Treasury bills $ 150m 2 year commercial loans $ 75m Fixed rate, 9% p.a. annually 10 year corporate loans-floating rate: LIBOR+50bp, semiannual roll date $ 505m 10 year floating rate mortgages quarterly roll dates $ 600m Overnight Fed Funds 91-day Commercial Paper Equity 100m 270m 65m Notes: Commercial paper is a pure discount instrument. The 5 year bonds pay 8.5% p.a. semiannually with a yield of 7.5% p.a. and have a duration of 4.2 years. The 1 vear Certificates of Deposit pay 2.75% p.a. annually. All values are market values. 17. If year spot rates are 3% pa, and 2 year spot rates are 2.5% p.a., what is the implied forward rate for delivery in one year of one year maturity securities? a. 3% p.a. b) 2% p.a. 52.025 c. 2.5% p.a. (l+.03) T .03 d. - 4% p.a. 1.050625 e. 5% p.a. Clit.0252 = 2.02 18. Using your answer to question number 17, the market's consensus estimate of expected future spot rates is: @ One year spot rates are expected to decrease by 100 basis points. b. Two year spot rates are expected to increase by 100 basis points. c. One year spot rates are expected to decrease by 200 basis points. d. Two year spot rates are expected to increase by 200 basis points. e. One year spot rates are expected to decrease by 250 basis points. 19. What is the expected impact on the bank's equity value if interest rates are expected to fluctuate according to the expectations incorporated into the implied forward rate from question number 17? a. -$11.58 million b. -$14.48 million c. -$5.79 million d. -$17.37 million e. -$2.9 million Use the following to answer questions 1-19. NAV I Den to assessation repricing gap ($ million Liabilities: 1 year Certificates of Deposit S 825m 5 year Bonds 70m Bank of Baruch Assets: 91 day US Treasury bills $ 150m 2 year commercial loans $ 75m Fixed rate, 9% p.a. annually 10 year corporate loans-floating rate: LIBOR+50bp, semiannual roll date $ 505m 10 year floating rate mortgages quarterly roll dates $ 600m Overnight Fed Funds 91-day Commercial Paper Equity 100m 270m 65m Notes: Commercial paper is a pure discount instrument. The 5 year bonds pay 8.5% p.a. semiannually with a yield of 7.5% p.a. and have a duration of 4.2 years. The 1 vear Certificates of Deposit pay 2.75% p.a. annually. All values are market values. 17. If year spot rates are 3% pa, and 2 year spot rates are 2.5% p.a., what is the implied forward rate for delivery in one year of one year maturity securities? a. 3% p.a. b) 2% p.a. 52.025 c. 2.5% p.a. (l+.03) T .03 d. - 4% p.a. 1.050625 e. 5% p.a. Clit.0252 = 2.02 18. Using your answer to question number 17, the market's consensus estimate of expected future spot rates is: @ One year spot rates are expected to decrease by 100 basis points. b. Two year spot rates are expected to increase by 100 basis points. c. One year spot rates are expected to decrease by 200 basis points. d. Two year spot rates are expected to increase by 200 basis points. e. One year spot rates are expected to decrease by 250 basis points. 19. What is the expected impact on the bank's equity value if interest rates are expected to fluctuate according to the expectations incorporated into the implied forward rate from question number 17? a. -$11.58 million b. -$14.48 million c. -$5.79 million d. -$17.37 million e. -$2.9 million

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts