Question: Please Answer Question 3 Bond Pricing, Duration, and Convexity 1. Using the following data from Sept. 14, 2020, plot (graph) the corporate A-rated yield and

Please Answer Question 3

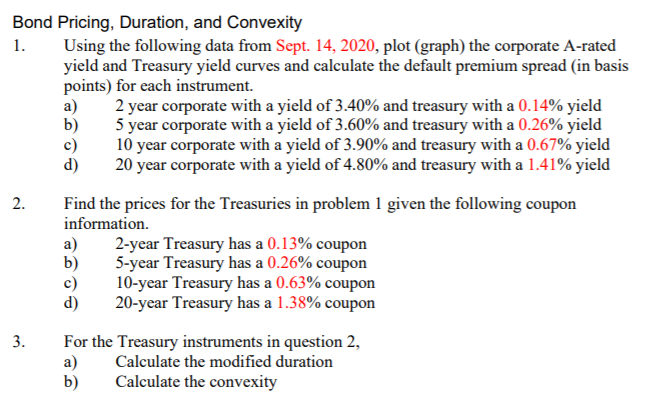

Bond Pricing, Duration, and Convexity 1. Using the following data from Sept. 14, 2020, plot (graph) the corporate A-rated yield and Treasury yield curves and calculate the default premium spread (in basis points) for each instrument. a) 2 year corporate with a yield of 3.40% and treasury with a 0.14% yield b) 5 year corporate with a yield of 3.60% and treasury with a 0.26% yield c) 10 year corporate with a yield of 3.90% and treasury with a 0.67% yield d) 20 year corporate with a yield of 4.80% and treasury with a 1.41% yield 2. Find the prices for the Treasuries in problem 1 given the following coupon information. a) 2-year Treasury has a 0.13% coupon b) 5-year Treasury has a 0.26% coupon 10-year Treasury has a 0.63% coupon d) 20-year Treasury has a 1.38% coupon 3. For the Treasury instruments in question 2, a) Calculate the modified duration b) Calculate the convexity Bond Pricing, Duration, and Convexity 1. Using the following data from Sept. 14, 2020, plot (graph) the corporate A-rated yield and Treasury yield curves and calculate the default premium spread (in basis points) for each instrument. a) 2 year corporate with a yield of 3.40% and treasury with a 0.14% yield b) 5 year corporate with a yield of 3.60% and treasury with a 0.26% yield c) 10 year corporate with a yield of 3.90% and treasury with a 0.67% yield d) 20 year corporate with a yield of 4.80% and treasury with a 1.41% yield 2. Find the prices for the Treasuries in problem 1 given the following coupon information. a) 2-year Treasury has a 0.13% coupon b) 5-year Treasury has a 0.26% coupon 10-year Treasury has a 0.63% coupon d) 20-year Treasury has a 1.38% coupon 3. For the Treasury instruments in question 2, a) Calculate the modified duration b) Calculate the convexity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts