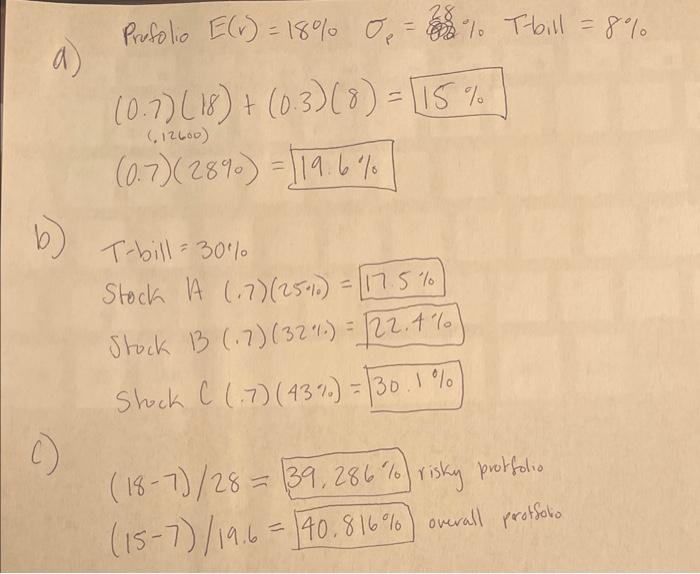

Question: please answer question d 2 (2pts.) Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation

2 (2pts.) Assume that you manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 28%. The T-bill rate is 8%. a. Your client chooses to invest 70% of a portfolio in your fund and 30% in an essentially T-bill (risk-free) money market fund. What are the expected value and standard deviations of the rate of return on his portfolio? b. Suppose that your risky portfolio includes the following investments in the given proportions: What are the investment proportions of your client's overall portfolio, including the position in T-bills? c. What is the reward-to-volatility (Sharpe) ratio (S) of your risky portfolio? Your client's? d. Draw the CAL of your portfolio on an expected return-standard deviation diagram. What is the slope of the CAL? Show the position of your client on your fund'S CAL. a) Prufolio E(r)=18%p=28% T-bill =8% (0.7)(18)+(0.3)(8)=15%(0.7260)(28%)=19.6% b) Tbill=30% StockA(.7)(25%=17.5%StockB(.7)(32%)=22.4%ShockC(.7)(43%)=30.1% C) (187)/28=39.286% risky protfolio (157)/19.6=40.816% overall protfolo

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts