Question: PLEASE ANSWER QUSTION 5. QUESTION 5 IS BASED ON QUESTION 4. 4. Write the model (1) using a vector form in a sample version as

PLEASE ANSWER QUSTION 5. QUESTION 5 IS BASED ON QUESTION 4.

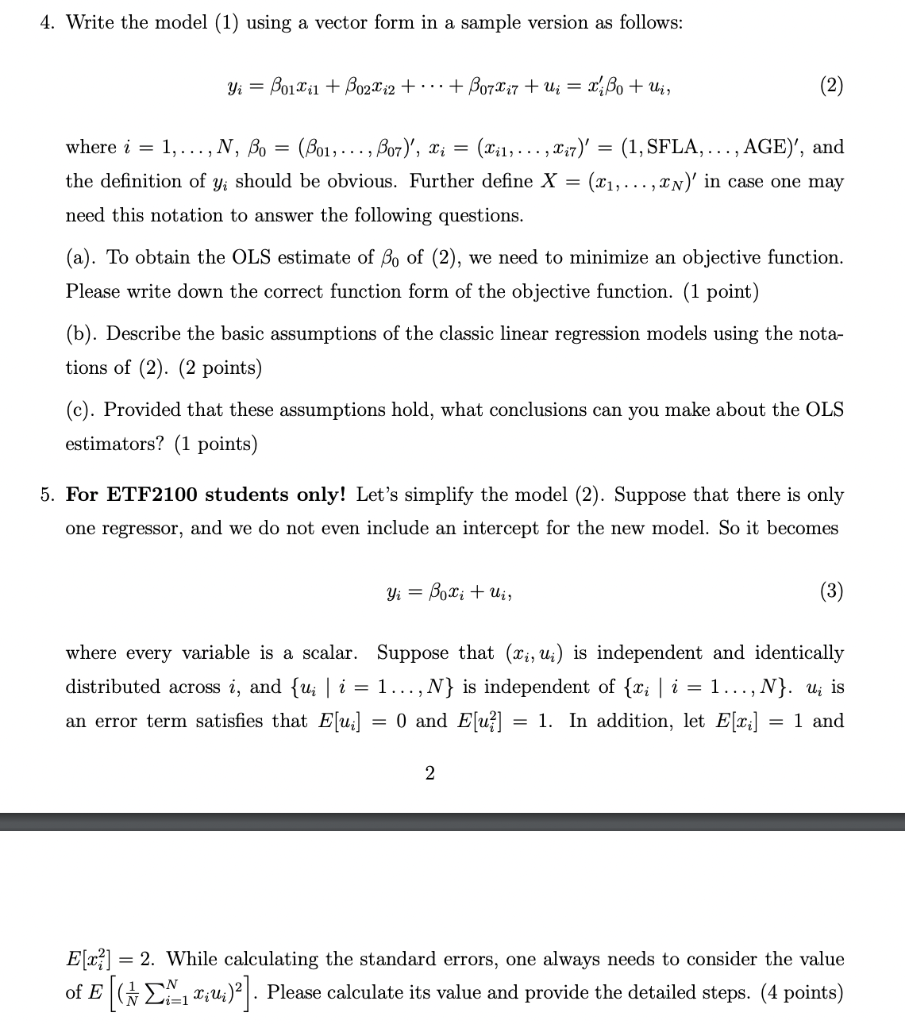

4. Write the model (1) using a vector form in a sample version as follows: Yi = Boili1 + Bo22:2 + ... + B072;7 + Wi = ' B + Wi, (2) where i = 1,...,N, Bo = (B01, ..., Bor)', Xi = (Lil, ... , 227) = (1, SFLA, ..., AGE)', and the definition of yi should be obvious. Further define X = (11,...,xn)' in case one may need this notation to answer the following questions. (a). To obtain the OLS estimate of Bo of (2), we need to minimize an objective function. Please write down the correct function form of the objective function. (1 point) (b). Describe the basic assumptions of the classic linear regression models using the nota- tions of (2). (2 points) (c). Provided that these assumptions hold, what conclusions can you make about the OLS estimators? (1 points) 5. For ETF2100 students only! Let's simplify the model (2). Suppose that there is only one regressor, and we do not even include an intercept for the new model. So it becomes Yi = Boxi + ui, (3) where every variable is a scalar. Suppose that (xi, Ui) is independent and identically distributed across i, and {u; | i = 1...,N} is independent of {xi | i = 1...,N}. wi is an error term satisfies that E[ui] = 0 and E[u] = 1. In addition, let E[w:] = 1 and 2 E[x?] = 2. While calculating the standard errors, one always needs to consider the value of E[G 24. 1;4;)*]. Please calculate its value and provide the detailed steps. (4 points) 4. Write the model (1) using a vector form in a sample version as follows: Yi = Boili1 + Bo22:2 + ... + B072;7 + Wi = ' B + Wi, (2) where i = 1,...,N, Bo = (B01, ..., Bor)', Xi = (Lil, ... , 227) = (1, SFLA, ..., AGE)', and the definition of yi should be obvious. Further define X = (11,...,xn)' in case one may need this notation to answer the following questions. (a). To obtain the OLS estimate of Bo of (2), we need to minimize an objective function. Please write down the correct function form of the objective function. (1 point) (b). Describe the basic assumptions of the classic linear regression models using the nota- tions of (2). (2 points) (c). Provided that these assumptions hold, what conclusions can you make about the OLS estimators? (1 points) 5. For ETF2100 students only! Let's simplify the model (2). Suppose that there is only one regressor, and we do not even include an intercept for the new model. So it becomes Yi = Boxi + ui, (3) where every variable is a scalar. Suppose that (xi, Ui) is independent and identically distributed across i, and {u; | i = 1...,N} is independent of {xi | i = 1...,N}. wi is an error term satisfies that E[ui] = 0 and E[u] = 1. In addition, let E[w:] = 1 and 2 E[x?] = 2. While calculating the standard errors, one always needs to consider the value of E[G 24. 1;4;)*]. Please calculate its value and provide the detailed steps. (4 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts