Question: please answer step by step with words explains Consider a market in which a risk-free bond and a risky stock are traded. The figure below

please answer step by step with words explains

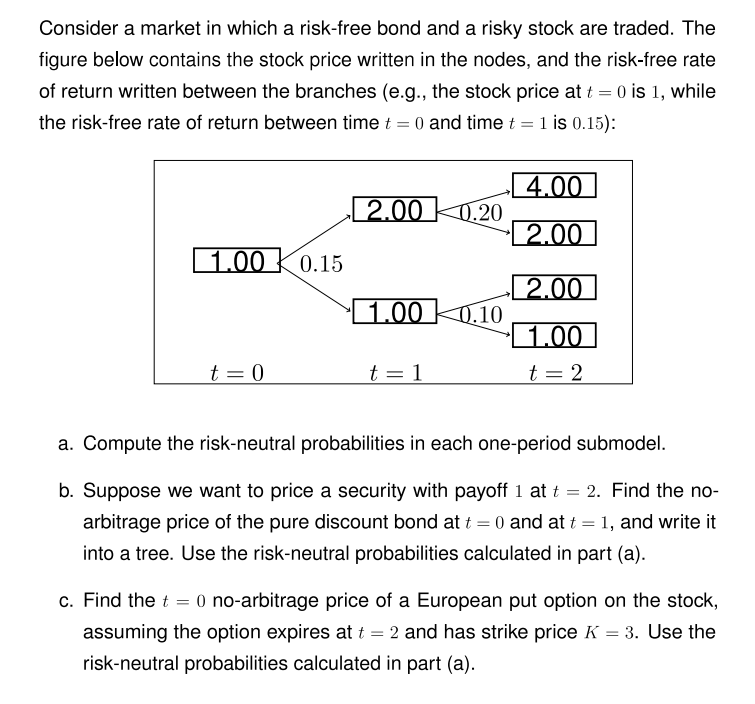

Consider a market in which a risk-free bond and a risky stock are traded. The figure below contains the stock price written in the nodes, and the risk-free rate of return written between the branches (e.g., the stock price at t=0 is 1 , while the risk-free rate of return between time t=0 and time t=1 is 0.15 ): a. Compute the risk-neutral probabilities in each one-period submodel. b. Suppose we want to price a security with payoff 1 at t=2. Find the noarbitrage price of the pure discount bond at t=0 and at t=1, and write it into a tree. Use the risk-neutral probabilities calculated in part (a). c. Find the t=0 no-arbitrage price of a European put option on the stock, assuming the option expires at t=2 and has strike price K=3. Use the risk-neutral probabilities calculated in part (a). Consider a market in which a risk-free bond and a risky stock are traded. The figure below contains the stock price written in the nodes, and the risk-free rate of return written between the branches (e.g., the stock price at t=0 is 1 , while the risk-free rate of return between time t=0 and time t=1 is 0.15 ): a. Compute the risk-neutral probabilities in each one-period submodel. b. Suppose we want to price a security with payoff 1 at t=2. Find the noarbitrage price of the pure discount bond at t=0 and at t=1, and write it into a tree. Use the risk-neutral probabilities calculated in part (a). c. Find the t=0 no-arbitrage price of a European put option on the stock, assuming the option expires at t=2 and has strike price K=3. Use the risk-neutral probabilities calculated in part (a)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts