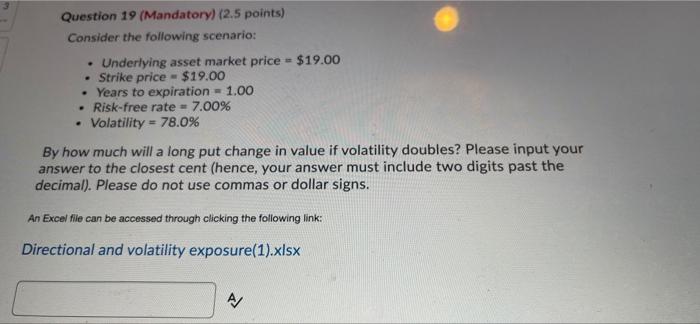

Question: please answer the 2 questions below: . Question 19 (Mandatory) (2.5 points) Consider the following scenario: Underlying asset market price $19.00 Strike price - $19.00

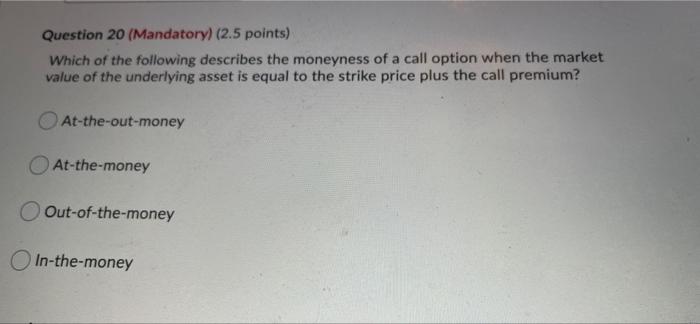

. Question 19 (Mandatory) (2.5 points) Consider the following scenario: Underlying asset market price $19.00 Strike price - $19.00 Years to expiration - 1.00 Risk-free rate - 7.00% Volatility = 78.0% By how much will a long put change in value if volatility doubles? Please input your answer to the closest cent (hence, your answer must include two digits past the decimal). Please do not use commas or dollar signs. An Excel file can be accessed through clicking the following link: Directional and volatility exposure(1).xlsx A/ Question 20 (Mandatory) (2.5 points) Which of the following describes the moneyness of a call option when the market value of the underlying asset is equal to the strike price plus the call premium? At-the-out-money At-the-money Out-of-the-money In-the-money

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts