Question: Please answer the all questions. Consider a world in which portfolio returns are generated by a two-factor linear model, where P denotes three portfolios A,

Please answer the all questions.

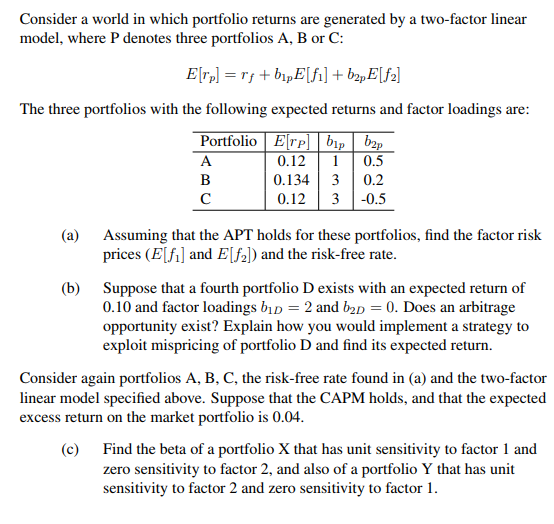

Consider a world in which portfolio returns are generated by a two-factor linear model, where P denotes three portfolios A, B or C: E["p] = rf + bipE[fi] + b2pE[f2] The three portfolios with the following expected returns and factor loadings are: Portfolio Erp] bip bap A 0.12 1 0.5 B 0.134 3 0.2 0.12 3 -0.5 (a) Assuming that the APT holds for these portfolios, find the factor risk prices (E[f] and E[82]) and the risk-free rate. (b) Suppose that a fourth portfolio D exists with an expected return of 0.10 and factor loadings bid = 2 and b2D = 0. Does an arbitrage opportunity exist? Explain how you would implement a strategy to exploit mispricing of portfolio D and find its expected return. Consider again portfolios A, B, C, the risk-free rate found in (a) and the two-factor linear model specified above. Suppose that the CAPM holds, and that the expected excess return on the market portfolio is 0.04. (C) Find the beta of a portfolio X that has unit sensitivity to factor 1 and zero sensitivity to factor 2, and also of a portfolio Y that has unit sensitivity to factor 2 and zero sensitivity to factor 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts