Question: Please answer the question and show your work: Suppose that there are two independent economic factors, F1 and F2. The risk-free rate is 6%, and

Please answer the question and show your work:

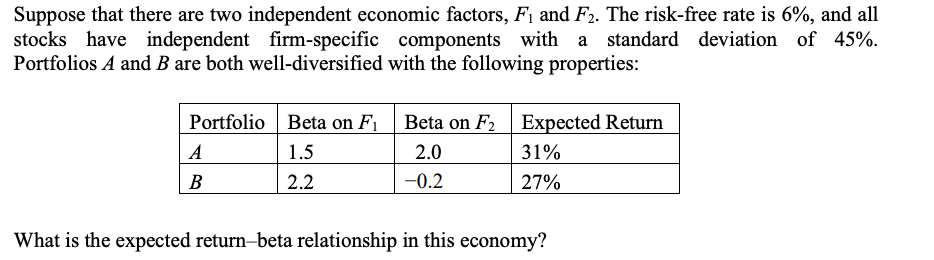

Suppose that there are two independent economic factors, F1 and F2. The risk-free rate is 6%, and all stocks have independent firm-specific components with a standard deviation of 45%. Portfolios A and B are both well-diversified with the following properties: What is the expected return-beta relationship in this economy? Suppose that there are two independent economic factors, F1 and F2. The risk-free rate is 6%, and all stocks have independent firm-specific components with a standard deviation of 45%. Portfolios A and B are both well-diversified with the following properties: What is the expected return-beta relationship in this economy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts