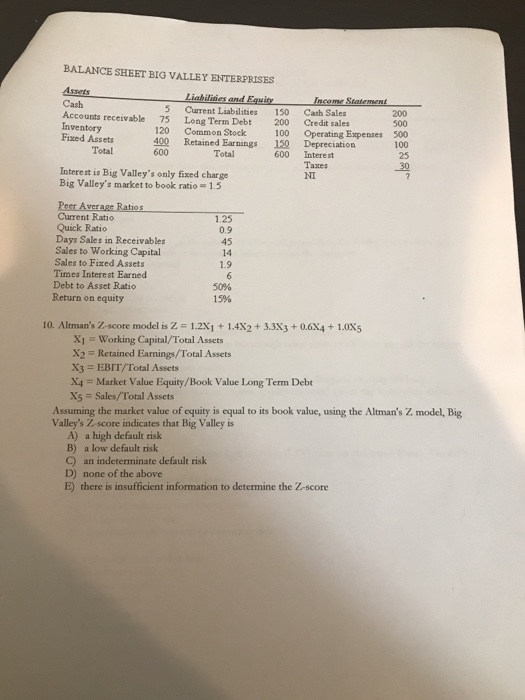

Question: Please answer the question in the following image showing all work BALANCE SHEET BIG VALLEY ENTERPRISES Cash 5 Current Liabilities 150 Cash Sales 120 Common

BALANCE SHEET BIG VALLEY ENTERPRISES Cash 5 Current Liabilities 150 Cash Sales 120 Common Stock 400 Retained Earnings 150 Depreciation ccounts receivable 75 Long Term Debt 200 Credit sales Inventory Fixed Assets 100 Operating Espenses 500 Total Total 600 Interest Interest is Big Valley's only fisxed charge Big Valley's market to book ratio 1.5 NI Pecr Average Ratios Current Ratio Quick Ratio Days Sales in Receivables Sales to Working Capital Sales to Fixed Assets Times Intere st Earned Debt to Asset Ratio Return on equity 0.9 45 1.9 15% 10. Altman's Z-score model is Z1.2x1+1.4x2+3.3x3+0.6x4+1.0x5 X1 = Working Capital/Total Assets X2 Retained Earnings/Total Assets X3-:/Total Assets X4 = Market Value Equity/Book Value long Term Debt X5 Sales/Total Assets Assuming the market value of equity is equal to its book value, using the Altman's Z model, Big Valley's Z-score indicates that Big Valley is A) a high default risk B) a low default risk C) an indeterminate default risk D) none of the above E) there is insufficient information to determine the Z-score

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts