Question: please answer the questions below: with calculation and formula 2. For the December 2018 futures contract on the S&P500 Index (SPX) compute 'Fair' Value and

please answer the questions below: with calculation and formula

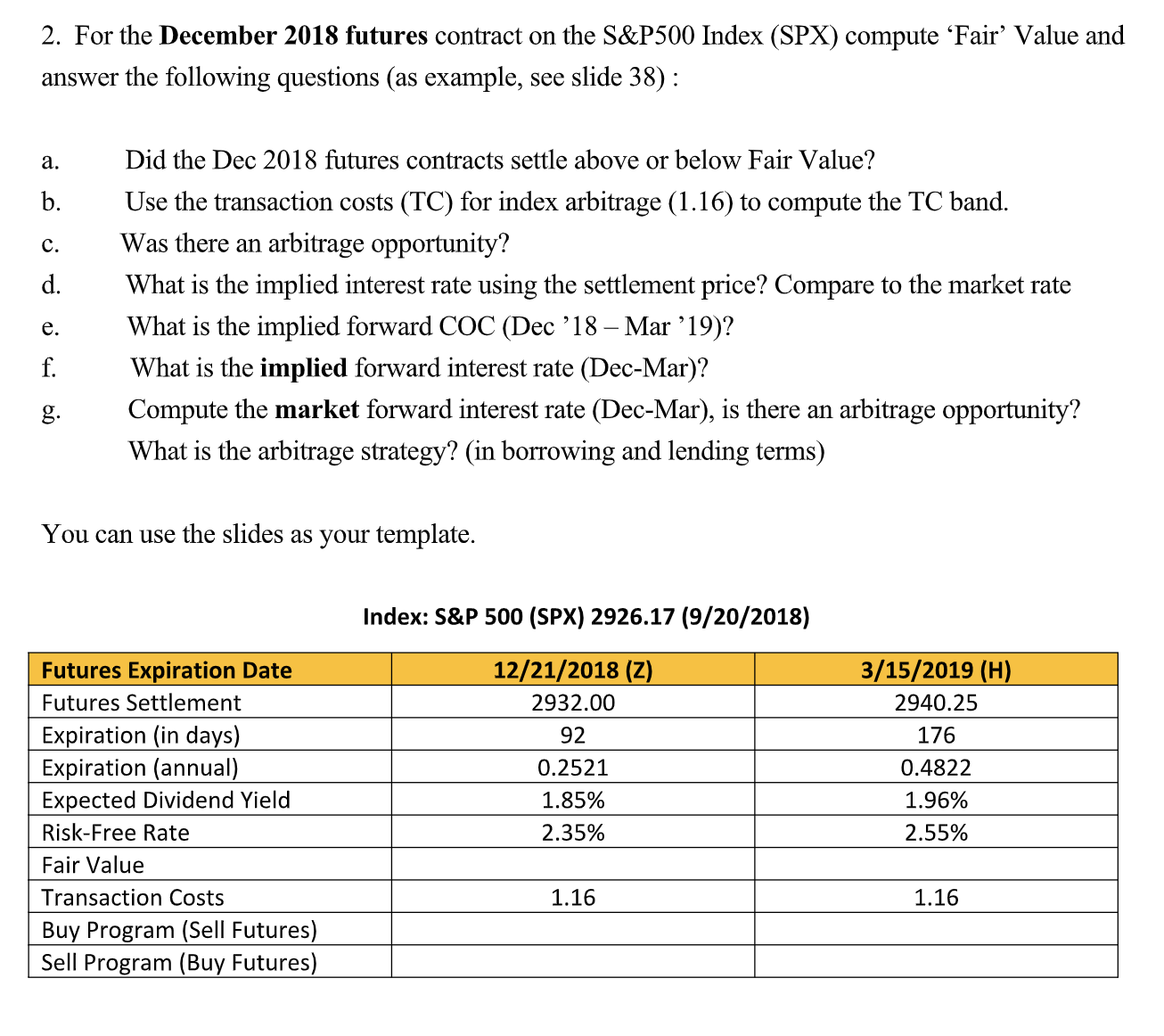

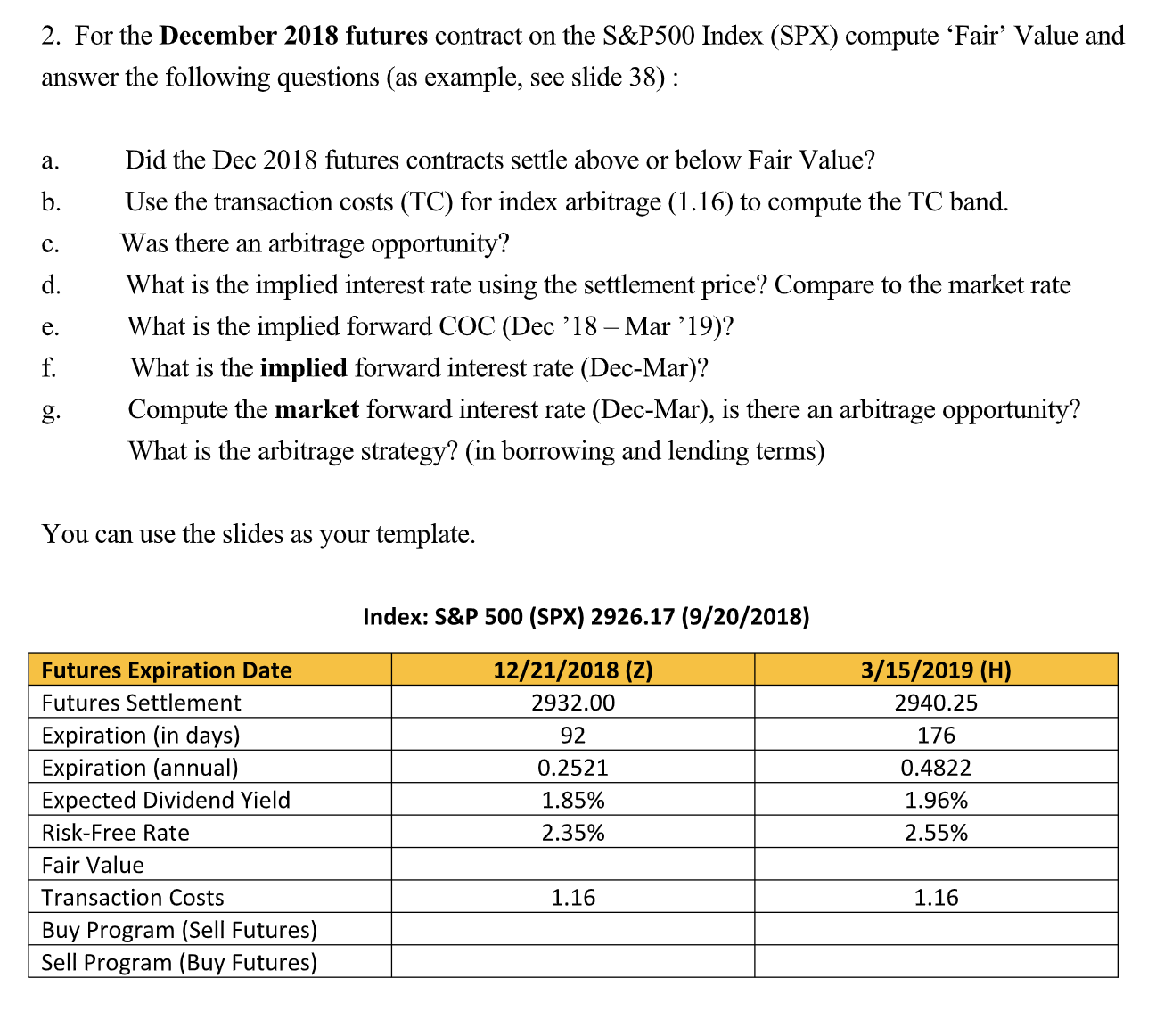

2. For the December 2018 futures contract on the S&P500 Index (SPX) compute 'Fair' Value and answer the following questions (as example, see slide 38) : Did the Dec 2018 itures contracts settle above or below Fair Value? Use the transaction costs (TC) for index arbitrage (1.16) to compute the TC band. Was there an arbitrage opportunity? What is the implied interest rate using the settlement price? Compare to the market rate What is the implied forward COC (Dec '18 Mar ' 19)? What is the implied forward interest rate (Dec-Mar)? Compute the market forward interest rate (Dec-Mar), is there an arbitrage opportunity? What is the arbitrage strategy? (in borrowing and lending terms) mwcepp'e You can use the slides as your template. Index: sap 500 (SPX) 2926.17 (9/20/2018) Futures Expiration Date 12/21/2018 (2) 3/15/2019 (H) Futures Settlement 29322. 00 29:10. 25 Expiration (in days) Expiration (annual) 0 2521 0.1178622 Expected Dividend Yield 1. 85% 1. 96% Risk-Free Rate 2. 35% 2.55% Fair Value Transaction Costs Buy Program (Sell Futures) Sell Program (Buy Futures) =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts