Question: Please answer the questions contained in the screenshots below 1 Numeric 1 point Compute the Macaulay duration of a 5-year, annually-compounded zero coupon bond with

Please answer the questions contained in the screenshots below

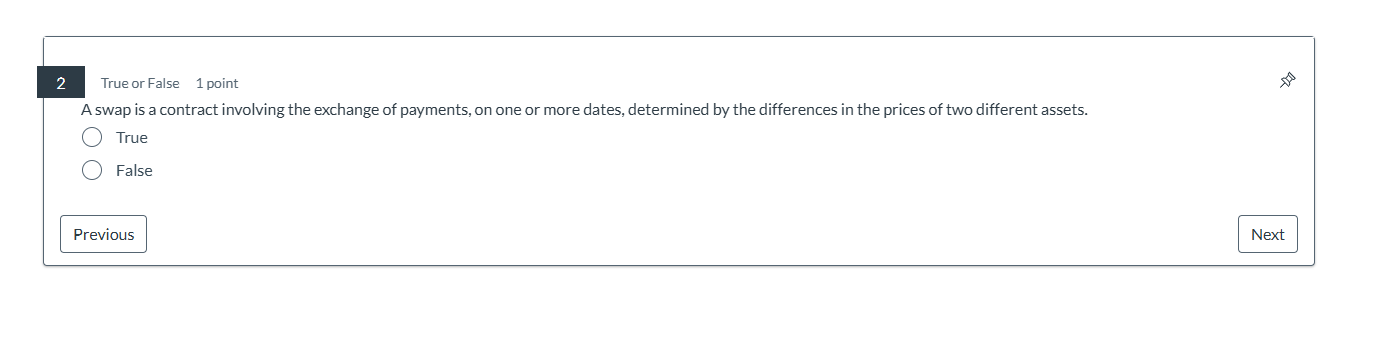

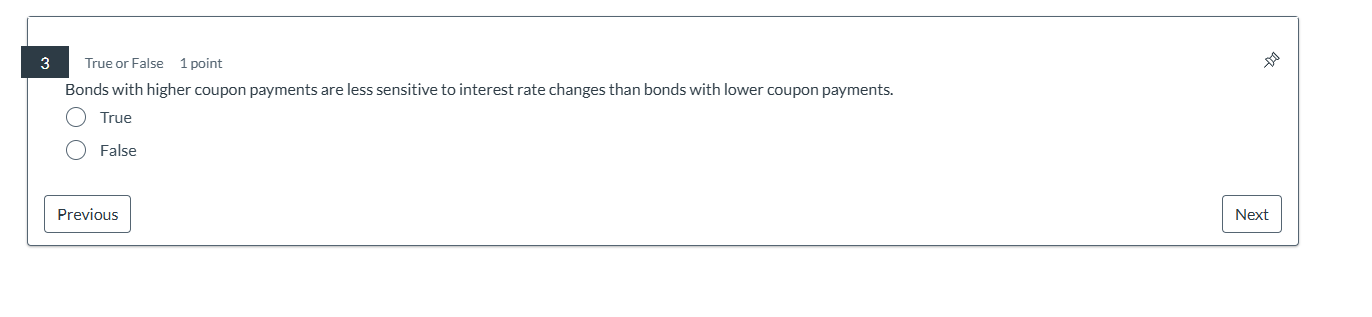

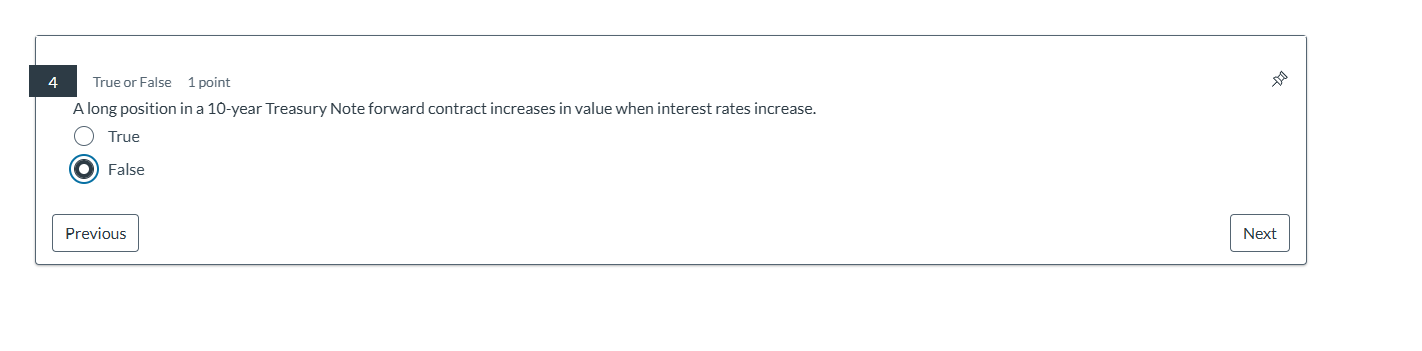

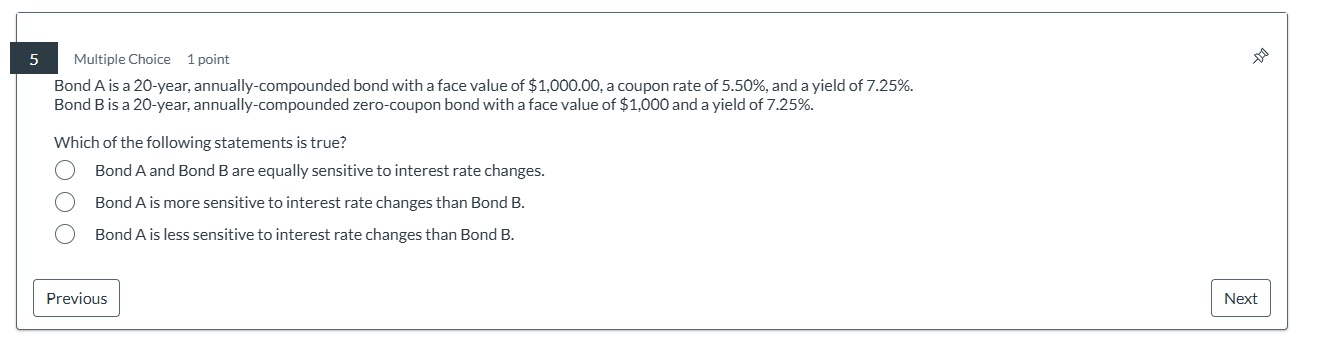

1 Numeric 1 point Compute the Macaulay duration of a 5-year, annually-compounded zero coupon bond with a face value of $1,000 and a yield of 5.75%. Round to the nearest 0.01. 5.02 True or False 1 point A swap is a contract involving the exchange of payments, on one or more dates, determined by the differences in the prices of two different assets. True False Previous Next3 True or False 1 point Bonds with higher coupon payments are less sensitive to interest rate changes than bonds with lower coupon payments. True O False Previous Next4 True or False 1 point A long position in a 10-year Treasury Note forward contract increases in value when interest rates increase. O True O False Previous Next5 Multiple Choice 1 point Bond A is a 20-year, annually-compounded bond with a face value of $1,000.00, a coupon rate of 5.50%, and a yield of 7.25%. Bond B is a 20-year, annually-compounded zero-coupon bond with a face value of $1,000 and a yield of 7.25%. Which of the following statements is true? O Bond A and Bond B are equally sensitive to interest rate changes. O Bond A is more sensitive to interest rate changes than Bond B. O Bond A is less sensitive to interest rate changes than Bond B. Previous NextMultiple Choice 1 point Which one of the following measures the percent change in the bond price when yields change by 1.00%? O Modified duration O Price value of a basis point O Macaulay duration () Modified convexity Previous Next 7 True or False 1 point If a bond's yield increases to 4.78% from 4.76% and its price changes by $0.92, then the bond's price value of a basis point is $0.92. O True O False Previous Next8 True or False 1 point Bonds with less time-to-maturity are more sensitive than bonds with more time-to-maturity. True False Previous Nextn Multiple Choice 1 point 5? Which of the following is the underlying asset in the 10-year Treasury Note futures contract? 6.50% bond between 6.00 to 10.00 years to maturity. Zero coupon bond between 6.00 to 10.00 years to maturity. Zero coupon bond with 10.00 years to maturity. O00O0 6.00% bond between 6.50 to 10.00 years to maturity. Previous 10 True or False 1 point A typical interest rate swap involves the exchange of a fixed-rate payment and a floating-rate payment between two counterparties. True O False Previous Next11 Numeric 1 point Compute the price of a 7-year, annually-compounded with a face value of $1,000.00, a coupon rate of 8.15%, and a yield of 4.35%. Round to the nearest $0.01. 122.52 Previous Next12 True or False 1 point Hedging a bond portfolio against interest rate changes can only be done using a derivative security. True O False Previous Next13 Numeric 1 point Compute the price of a 3-year, annually-compounded zero-coupon bond with a face value of $1,000.00 and a yield of 4.35%. Round to the nearest $0.01. 88.01 Previous Submit

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!