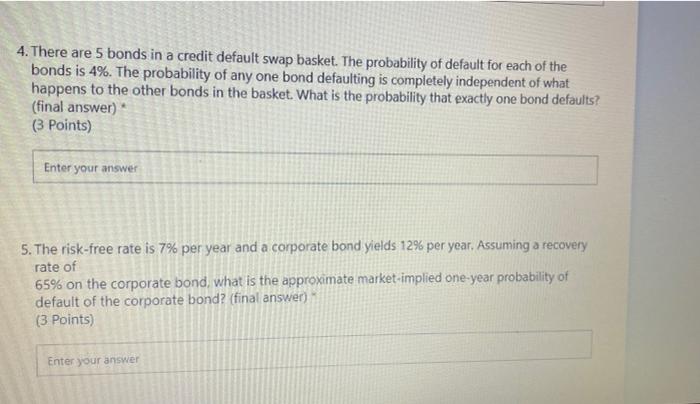

Question: please answer the two 4. There are 5 bonds in a credit default swap basket. The probability of default for each of the bonds is

please answer the two

please answer the two 4. There are 5 bonds in a credit default swap basket. The probability of default for each of the bonds is 4%. The probability of any one bond defaulting is completely independent of what happens to the other bonds in the basket. What is the probability that exactly one bond defaults? (final answer) (3 Points) Enter your answer 5. The risk-free rate is 7% per year and a corporate bond yields 12% per year. Assuming a recovery rate of 65% on the corporate bond, what is the approximate market-implied one-year probability of default of the corporate bond? (final answer) (3 Points) Enter your

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock