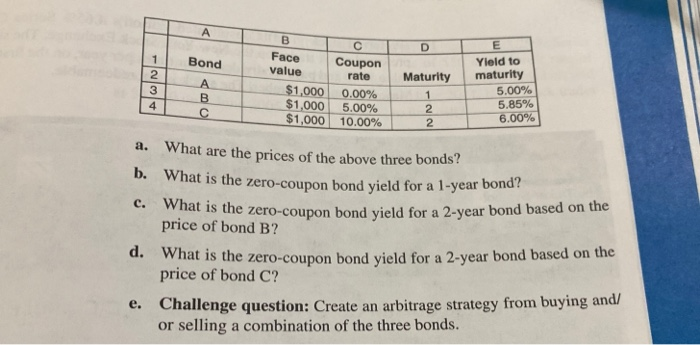

Question: please attach excel formulas recent uuu, W T 9. (Coupon stripping, arbitrage) You are given the following information three traded bonds making annual coupon payments:

recent uuu, W T 9. (Coupon stripping, arbitrage) You are given the following information three traded bonds making annual coupon payments: D Bond Maturity Face value $1.000 $1,000 $1,000 C Coupon rate 0.00% 5.00% 10.00% Yield to maturity 5.00% 5.85% 6.00% 2 a. What are the prices of the above three bonds? b. What is the zero-coupon bond yield for a 1-year bo c. What is the zero-coupon bond yield for price of bond B? zero-coupon bond yield for a 2-year bond based on the d. What is the zero-coupon bond yield for a 2-year bond based on the price of bond C? e. Challenge question: Create an arbitrage strategy from buying and/ or selling a combination of the three bonds

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts