Question: please attach with formulars to tell how these numbers come out. both in manual and in excel. thanks 1. Using the information in the table,

please attach with formulars to tell how these numbers come out. both in manual and in excel. thanks

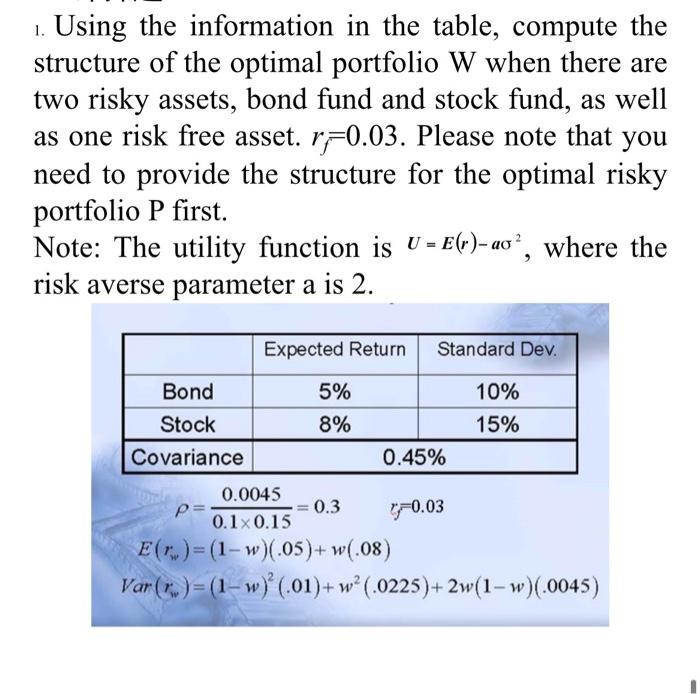

1. Using the information in the table, compute the structure of the optimal portfolio W when there are two risky assets, bond fund and stock fund, as well as one risk free asset. r=0.03. Please note that you need to provide the structure for the optimal risky portfolio P first. Note: The utility function is U = E(r)- ao ?, where the risk averse parameter a is 2. Expected Return Standard Dev. 5% Bond Stock Covariance 10% 15% 8% 0.45% 10.03 0.0045 P= = 0.3 0.10.15 E(C)=(1-w)(.05)+ WC.08) Var()= (1-w) (.01)+w? (.0225)+2w(1-w)(.0045)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock