Question: Please be clear and do not answer with an excel sheet. I need to see the equations written down. thank you 1. Prices of zero-coupon

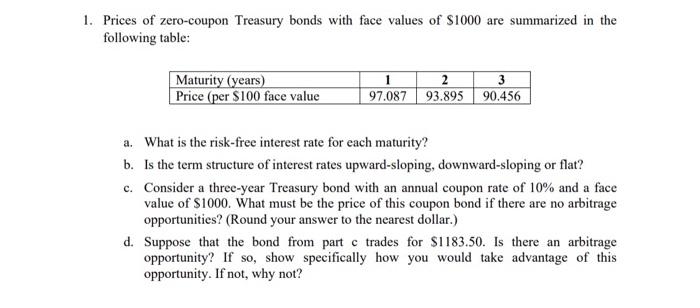

1. Prices of zero-coupon Treasury bonds with face values of S1000 are summarized in the following table: Maturity (years) Price (per $100 face value 1 2 3 97.087 93.895 90.456 a. What is the risk-free interest rate for each maturity? b. Is the term structure of interest rates upward-sloping, downward-sloping or flat? c. Consider a three-year Treasury bond with an annual coupon rate of 10% and a face value of $1000. What must be the price of this coupon bond if there are no arbitrage opportunities? (Round your answer to the nearest dollar.) d. Suppose that the bond from part c trades for $1183.50. Is there an arbitrage opportunity? If so, show specifically how you would take advantage of this opportunity. If not, why not? 1. Prices of zero-coupon Treasury bonds with face values of S1000 are summarized in the following table: Maturity (years) Price (per $100 face value 1 2 3 97.087 93.895 90.456 a. What is the risk-free interest rate for each maturity? b. Is the term structure of interest rates upward-sloping, downward-sloping or flat? c. Consider a three-year Treasury bond with an annual coupon rate of 10% and a face value of $1000. What must be the price of this coupon bond if there are no arbitrage opportunities? (Round your answer to the nearest dollar.) d. Suppose that the bond from part c trades for $1183.50. Is there an arbitrage opportunity? If so, show specifically how you would take advantage of this opportunity. If not, why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts