Question: please can you answer these parts clearly will hit a like Question 3 A retail investor has collected data on different characteristics for three asset

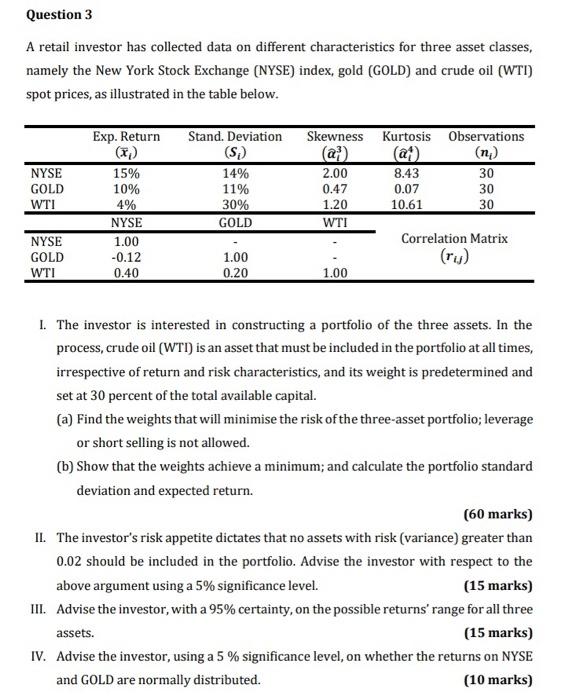

Question 3 A retail investor has collected data on different characteristics for three asset classes, namely the New York Stock Exchange (NYSE) index, gold (GOLD) and crude oil (WTI) spot prices, as illustrated in the table below. Exp. Return Skewness Kurtosis Observations NYSE GOLD WTI Stand. Deviation (S) 14% 11% 30% GOLD 15% 10% 4% NYSE 1.00 -0.12 0.40 2.00 0.47 1.20 WTI 8.43 0.07 10.61 30 30 30 Correlation Matrix NYSE GOLD WTI 1.00 0.20 1.00 1. The investor is interested in constructing a portfolio of the three assets. In the process, crude oil (WTI) is an asset that must be included in the portfolio at all times, irrespective of return and risk characteristics, and its weight is predetermined and set at 30 percent of the total available capital. (a) Find the weights that will minimise the risk of the three-asset portfolio; leverage or short selling is not allowed. (b) Show that the weights achieve a minimum; and calculate the portfolio standard deviation and expected return. (60 marks) II. The investor's risk appetite dictates that no assets with risk (variance) greater than 0.02 should be included in the portfolio. Advise the investor with respect to the above argument using a 5% significance level. (15 marks) III. Advise the investor, with a 95% certainty, on the possible returns' range for all three assets. (15 marks) IV. Advise the investor, using a 5 % significance level, on whether the returns on NYSE and GOLD are normally distributed. (10 marks) Question 3 A retail investor has collected data on different characteristics for three asset classes, namely the New York Stock Exchange (NYSE) index, gold (GOLD) and crude oil (WTI) spot prices, as illustrated in the table below. Exp. Return Skewness Kurtosis Observations NYSE GOLD WTI Stand. Deviation (S) 14% 11% 30% GOLD 15% 10% 4% NYSE 1.00 -0.12 0.40 2.00 0.47 1.20 WTI 8.43 0.07 10.61 30 30 30 Correlation Matrix NYSE GOLD WTI 1.00 0.20 1.00 1. The investor is interested in constructing a portfolio of the three assets. In the process, crude oil (WTI) is an asset that must be included in the portfolio at all times, irrespective of return and risk characteristics, and its weight is predetermined and set at 30 percent of the total available capital. (a) Find the weights that will minimise the risk of the three-asset portfolio; leverage or short selling is not allowed. (b) Show that the weights achieve a minimum; and calculate the portfolio standard deviation and expected return. (60 marks) II. The investor's risk appetite dictates that no assets with risk (variance) greater than 0.02 should be included in the portfolio. Advise the investor with respect to the above argument using a 5% significance level. (15 marks) III. Advise the investor, with a 95% certainty, on the possible returns' range for all three assets. (15 marks) IV. Advise the investor, using a 5 % significance level, on whether the returns on NYSE and GOLD are normally distributed. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts